What Is a Dividend and How Does It Actually Work?

A dividend is a portion of a company’s profits paid directly to shareholders — declared by the board of directors, tied to specific dates, and never guaranteed. Understanding how dividends work, from the ex-dividend date to the payout ratio, is essential before building income around them.

The first time a dividend hit my account, I remember doing a double-take. The market had been flat, I hadn’t done anything — and there was just… cash. That’s the appeal. But I’ve also watched investors get burned chasing high yields without understanding the mechanics. Miss the ex-dividend date by one day? No payout. Buy a “high-yield” stock that turns out to be high-yield because the price has collapsed? That’s a different story entirely. Let’s walk through exactly how dividends work, from the boardroom decision to the dollars in your account.

What a Dividend Actually Is

A dividend is a portion of a company’s profits distributed to its shareholders. Since shareholders own a piece of the company, they’re entitled to share in the profits — that’s the logic.

The decision to pay a dividend rests with the board of directors. They declare a dividend, specifying the amount per share, the key dates, and when payment will occur. This is a formal board resolution, not a casual management call.

Dividends come in three main forms:

| Form | What it means |

|---|---|

| Cash dividend | Most common — cash paid directly per share |

| Stock dividend | Additional shares issued instead of cash |

| Special dividend | A one-time, extra payout on top of regular dividends |

Cash dividends are by far the norm. Special dividends tend to appear when a company has a windfall — an asset sale, an unusually strong year — and wants to pass that along to shareholders.

The Four Dates That Determine Who Gets Paid

This is where a lot of new investors get tripped up. There are four dates in the dividend timeline, and one in particular can make or break whether you receive payment.

| Date | What happens |

|---|---|

| Declaration Date | Board formally announces the dividend: amount, record date, payment date |

| Ex-Dividend Date | Buy on or after this date and you will NOT receive the dividend |

| Record Date | Company confirms its list of shareholders eligible for payment |

| Payment Date | Dividend cash lands in shareholder accounts |

The ex-dividend date is the one to tattoo on your brain. To receive a dividend, you must own shares before the ex-dividend date. The reason it sits a day or two before the record date comes down to settlement mechanics — stock trades typically take one to two business days to settle, so the cutoff is pushed back accordingly.

Payment frequency varies by company. Some pay quarterly, others semi-annually or annually. There’s no universal rule — check the company’s own disclosures for their schedule.

Reading Dividend Yield and Payout Ratio

Two numbers matter most when evaluating a dividend.

Dividend Yield

Dividend Yield = Annual Dividend per Share ÷ Current Share Price × 100If a stock trades at $50 and pays $2 annually, the yield is 4%. Here’s the catch: yield and price move in opposite directions. A yield that suddenly looks very attractive might be signaling that the stock price has dropped significantly — which isn’t necessarily good news.

Payout Ratio

Payout Ratio = Dividends per Share ÷ Earnings per Share × 100This tells you what share of profits the company is paying out as dividends. A payout ratio above 80% means the company is sending most of its earnings to shareholders, leaving little room for reinvestment or cushion if profits dip. Too low, and the company might be hoarding cash unnecessarily. What counts as “healthy” varies by sector, so compare within industries, not across them.

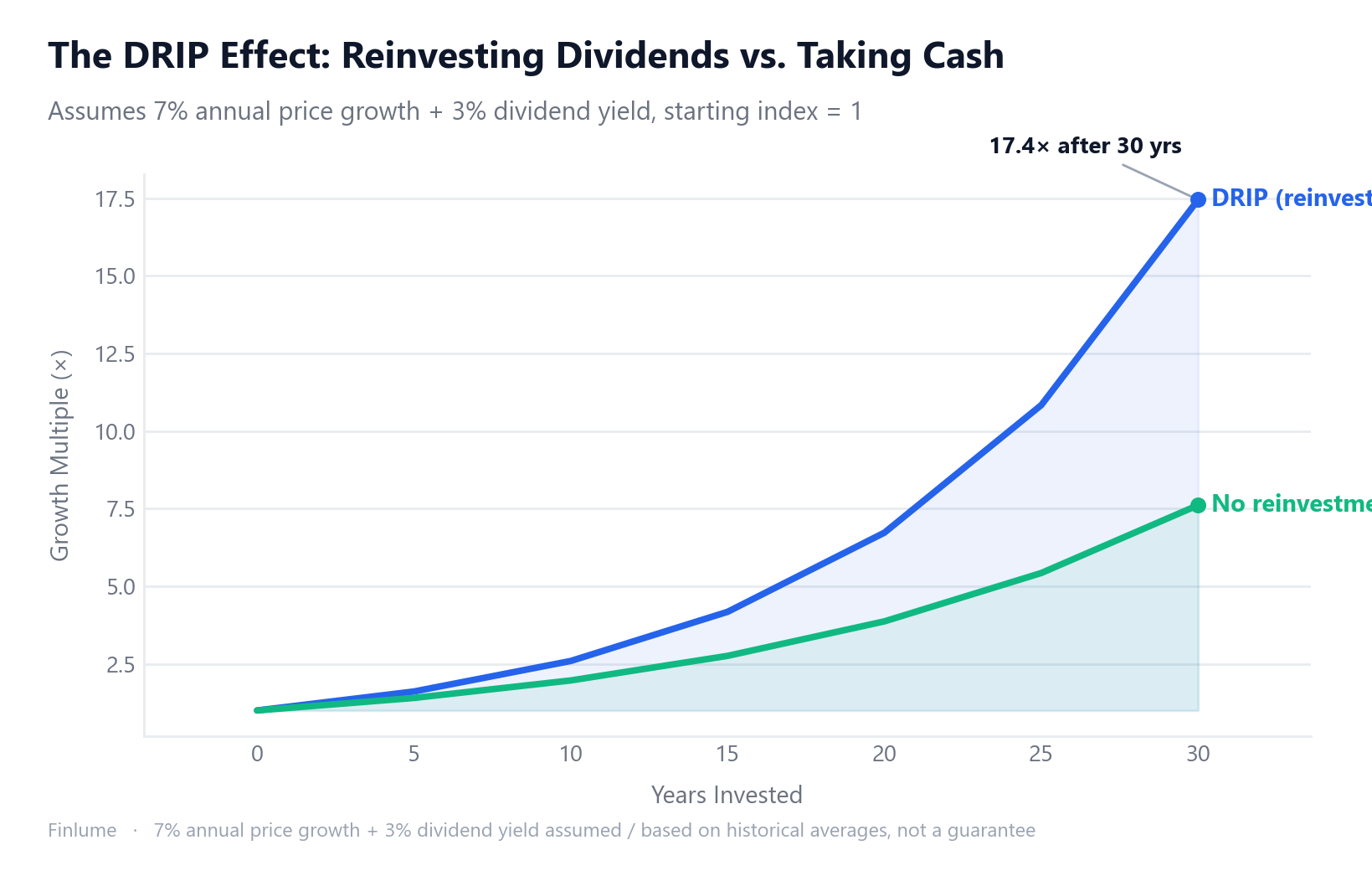

DRIP: Turning Dividends Into Compounding

DRIP stands for Dividend Reinvestment Plan. Instead of taking dividends as cash, you use them to buy more shares automatically. The compounding logic is straightforward — and if you want to understand why the effect feels slow at first and then explosive later, Why Compound Interest Takes Decades to Pay Off is worth reading alongside this:

More shares → larger dividend next cycle → more shares purchased → even larger dividend after that.

Historical data shows that reinvested dividends have contributed a meaningful share of long-term total stock market returns — not just price appreciation, but the cumulative effect of dividends being put back to work. That said, past data reflects averages; future results vary.

Practical note: most brokerages offer automatic DRIP enrollment. Setting it up once removes the temptation to spend the dividend and eliminates the friction of manually reinvesting each time. It’s a small behavioral trick with a real long-term edge.

Not Every Stock Pays a Dividend — And That’s Fine

A common assumption among new investors: own a stock, collect dividends. Not quite.

Growth companies typically reinvest every dollar back into the business — R&D, expansion, acquisitions. Their logic is that the return on reinvesting exceeds what they’d generate by handing cash back to shareholders. Many high-growth technology companies pay no dividend at all.

Dividend-paying companies tend to be more mature, with stable, predictable cash flows. Think consumer staples, utilities, financials. They’ve grown past the phase where every dollar needs to fuel expansion. If you’re weighing dividend stocks against growth-oriented alternatives, Value vs. Growth Investing: Why Neither Always Wins covers that tradeoff in depth. One specific category worth knowing: REITs, which are legally required to distribute at least 90% of taxable income to shareholders — making them some of the most consistent dividend-payers in any portfolio.

Neither approach is inherently better. If you need current income from your portfolio, dividends make sense. If you’re in an accumulation phase and don’t need cash flow today, growth stocks might fit your timeline better. The answer depends on your goals, not a blanket rule.

The Risk Nobody Talks About Enough: Dividends Can Be Cut

I’ve seen this catch people off guard: a stock with a long, consistent dividend history cuts the payout with little warning. It feels like a betrayal, but it’s entirely within a company’s rights.

Dividends are not guaranteed. The board can reduce or suspend them at any time — and they do, especially under financial stress. During the 2008–2009 financial crisis, roughly one-third of S&P 500 companies cut or suspended their dividends. Companies with decades of uninterrupted payouts were not immune.

Watch out for the dividend trap: an unusually high yield can be a warning sign, not an opportunity. If the yield looks too good to be true, the price may have fallen sharply for a reason — and if it keeps falling, capital losses can easily swamp dividend income.

On tax: dividend income is taxable in most jurisdictions, but the rules differ significantly by country, account type, and your personal tax situation. Always factor in after-tax yield when comparing dividend-paying investments, and verify the applicable rules for your situation.

The Dividend Trap, Quantified: Break-Even Years

Most articles warn you about the dividend trap. Few tell you exactly how long it takes to dig out of it. Here is the arithmetic, assuming the stock price freezes at its new lower level after the drop — the most optimistic scenario for a distressed company (if the price keeps falling, break-even never arrives).

Assumptions: yield is measured at the original purchase price; stock price stays flat after the initial drop; dividends taken as cash (no reinvestment).

| Yield at purchase | −10% price drop | −20% price drop | −30% price drop | −40% price drop |

|---|---|---|---|---|

| 4% | 2.5 yrs | 5 yrs | 7.5 yrs | 10 yrs |

| 6% | 1.7 yrs | 3.3 yrs | 5 yrs | 6.7 yrs |

| 8% | 1.2 yrs | 2.5 yrs | 3.8 yrs | 5 yrs |

| 10% | 1 yr | 2 yrs | 3 yrs | 4 yrs |

| 12% | 0.8 yrs | 1.7 yrs | 2.5 yrs | 3.3 yrs |

Break-even years = price drop % ÷ annual yield %. This table shows the minimum time required just to recover capital losses through dividends alone — ignoring taxes, transaction costs, and any further price moves.

The table makes the trap visible. A stock yielding 6% that drops 30% needs five full years of uninterrupted dividends just to get back to zero — and that only works if the company keeps paying the same dividend throughout, which is exactly what distressed companies often fail to do. At 4% yield with a 40% price drop, you are looking at ten years to break even under the rosiest possible assumptions.

The uncomfortable implication: the higher the yield looks, the harder the math often gets, because high yields frequently accompany large price drops. That is the trap.

Key Takeaways

- Dividend = a share of company profits paid to shareholders; declared by the board of directors.

- Four dates: Declaration → Ex-Dividend (cutoff for eligibility) → Record → Payment.

- Dividend yield = annual dividend ÷ share price × 100. A rising yield on a falling stock isn’t necessarily a good sign.

- Payout ratio = dividends ÷ earnings × 100. Very high ratios raise sustainability questions.

- DRIP = automatically reinvesting dividends to buy more shares, compounding over time.

- Growth stocks often pay no dividend — reinvesting profits instead. Neither path is wrong.

- Dividends can be cut. During the 2008 crisis, roughly one-third of S&P 500 companies did exactly that.

- Tax treatment varies by country and account type — always calculate after-tax yield.

- Dividend trap math: a 6% yield on a stock that drops 30% means 5 years of uninterrupted payouts just to break even — assuming price stays flat (it often doesn’t).

Dividends can be a genuinely rewarding part of investing — the sense that the portfolio is working even while you’re not watching. But that reward is only sustainable when you understand the mechanics and respect the risks alongside it.

🧮 Estimate your income: Enter an investment and yield into the dividend calculator to see your annual and monthly dividend income.

Frequently Asked Questions

What is the ex-dividend date and why does it matter?

The ex-dividend date is the cutoff: buy shares on or after this date and you will not receive the upcoming dividend. To qualify, you must own the shares before this date. It sits one or two business days before the record date because stock trades take time to settle.

Is a high dividend yield always a good sign?

Not necessarily. Yield rises when a stock price falls, so an unusually high yield can signal that the price has dropped sharply for a reason. This is the dividend trap — chasing high yield into a declining stock where capital losses quickly exceed dividend income.

How does DRIP compounding actually work?

DRIP stands for Dividend Reinvestment Plan. Instead of taking dividends as cash, you automatically buy more shares. More shares means a larger dividend next cycle, which buys even more shares — the cycle repeats and accelerates over time, especially over decades.

Can dividends be cut or cancelled?

Yes. Dividends are never guaranteed. The board of directors can reduce or suspend them at any time. During the 2008–2009 financial crisis, roughly one-third of S&P 500 companies cut or suspended their dividends — including many with long, uninterrupted payout histories.

Do all stocks pay dividends?

No. Growth companies typically reinvest profits into the business rather than paying dividends. Many high-growth technology companies pay nothing. Dividend-paying stocks tend to be more mature businesses with stable, predictable cash flows, such as consumer staples, utilities, and financials.