Why Compound Interest Takes Decades to Pay Off

I’ll be honest: the first time I looked at a compound interest table, I shrugged. “Interest earns interest” sounded like a fine sentence and nothing more. Then I traced my finger down to the 30-year row, and it stopped being a sentence. Here’s the conclusion up front: compounding doesn’t pay off early - it pays off suddenly, late. So the single most important thing today is the time you stay invested. The most realistic way to put time on your side is to buy steadily every month with dollar-cost averaging.

What Compounding Actually Is

Compound interest means the interest you earn starts earning interest too. Simple interest only ever pays on your original principal; compounding folds each year’s interest back into the pile so it grows alongside everything else. Picture a snowball: it starts the size of your fist, but the more you roll it, the bigger its surface gets - so each roll picks up more snow than the last. That’s compounding. Every year, the amount you gain gets a little bigger.

The Difference in Numbers

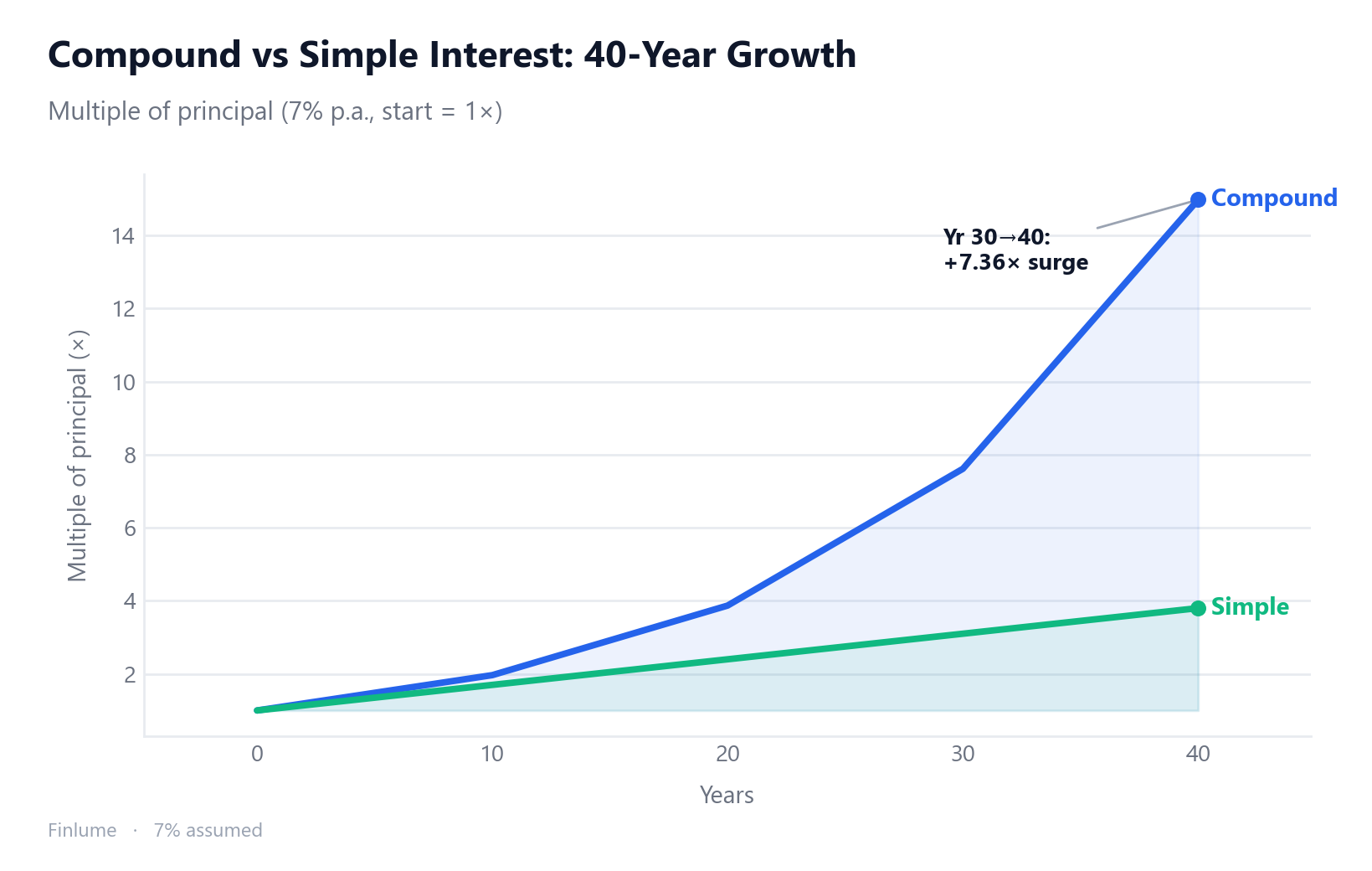

Say you put $10,000 to work at 7% a year, compounded. (That 7% is an illustration, not a promise - more on that below.)

| Years | Compound value | × principal |

|---|---|---|

| 10 | $19,670 | 1.967× |

| 20 | $38,700 | 3.870× |

| 30 | $76,120 | 7.612× |

| 40 | $149,740 | 14.974× |

See it? It barely doubles in the first decade, then nearly doubles again between year 30 and year 40 - in just ten years. The later squares weigh far more than the early ones.

Find Your Own Scenario

The 7% line above is just one illustration. Your real outcome depends on the return you assume and how long you stay invested - so here’s the full grid. Each cell is the ending value as a multiple of whatever you start with, which means it works for any amount, any currency:

| Assumed return | 10 yrs | 20 yrs | 30 yrs | 40 yrs |

|---|---|---|---|---|

| 4% | 1.48× | 2.19× | 3.24× | 4.80× |

| 6% | 1.79× | 3.21× | 5.74× | 10.29× |

| 7% | 1.97× | 3.87× | 7.61× | 14.97× |

| 8% | 2.16× | 4.66× | 10.06× | 21.72× |

| 10% | 2.59× | 6.73× | 17.45× | 45.26× |

Read across any row and the late-years surge jumps out. Read down any column and you see how much the assumed rate matters: two percentage points (6% vs 8%) barely separate at 10 years - 1.79× against 2.16× - yet by year 40 the gap has blown open to 10.29× versus 21.72×. Time doesn’t just grow your money; it amplifies whatever rate you earn, for better or worse.

Simple vs Compound: the 30-Year Gap

That same $10,000 at 7% simple interest grows to $31,000 after 30 years (3.10× the principal). Compound, at the same moment, sits at $76,120. Divide one by the other and you get roughly 2.45×. Same rate, same principal - the only difference is whether interest earned interest, and that alone splits the outcome by 2.45 times.

The Formula and the Rule of 72

The formula is A = P(1+r/n)^(nt), where P is principal, r is the annual rate (as a decimal, 0.07), n is how many times a year it compounds, and t is time. Simple interest is just I = P·r·t.

For mental math, use the Rule of 72: 72 divided by your return (as a whole number) gives the rough years to double. At 8%, 72÷8 = 9 years - almost exactly the precise figure (9.006). It’s most accurate in the 6-10% range. Note the quirk: the rate is a decimal (0.07) in the formula but a whole number (8) in the Rule of 72.

Compounding Frequency Matters Less Than You’d Think

People often ask whether daily compounding is a big edge. Compare them directly and the gaps are surprisingly small. Here are the multiples on principal at 10% over one year.

| Compounding | 1-year multiple |

|---|---|

| Annual | 1.10000× |

| Quarterly | 1.10381× |

| Monthly | 1.10471× |

| Daily | 1.10516× |

| Continuous (cap) | 1.10517× |

Even daily can’t beat the continuous-compounding ceiling. Rate and time move the needle far more than frequency does.

The Caveats You Need to Hear

No jokes in this part. The 7% is an assumption, not a guarantee. Markets fluctuate, and some years are negative. That a higher expected return always carries more volatility is exactly why risk and return go together. A nominal 7% minus 3% inflation leaves you around 4% in real terms - it’s worth seeing how inflation quietly erodes your savings to feel that real-return math. And compounding isn’t only your friend: a 1% annual fee compounds against you over decades just as relentlessly - that mirror-image compounding is laid out in numbers in how a 1% fee erodes your returns. The Rule of 72 is an approximation, too.

What You Actually Keep

Here’s the part the “compounding is magic” posts skip. Take that same $10,000 at 7% for 30 years, then strip out the two forces that quietly compound against you - a typical 1% fund fee and 3% inflation:

| $10,000 at 7%, 30 years | Multiple | Value |

|---|---|---|

| Nominal (the headline number) | 7.61× | $76,123 |

| After a 1% annual fee | 5.74× | $57,435 |

| In today’s money (3% inflation) | 3.14× | $31,361 |

| After both fee and inflation | 2.37× | $23,662 |

That $76,000 headline is really worth about $23,700 in today’s purchasing power once fees and inflation take their cut - roughly a third. Compounding is still well worth it, but the honest number to plan around is the bottom row, not the top one.

🧮 Try it yourself: Plug your own starting amount, monthly contribution, and time horizon into the compound interest calculator to see how the numbers grow.

Key Takeaways

- Compounding is interest on interest; it accelerates in the later years.

- $10,000 at 7%: $76,120 after 30 years, about 2.45× simple interest.

- 72 ÷ return (%) ≈ years to double, most accurate at 6-10%.

- Frequency differences are tiny and capped.

- 7% is an assumption; inflation and fees compound too. After a 1% fee and 3% inflation, that 30-year $76,120 is worth about $23,700 in today’s money.

The small snowball you start today only becomes something thirty years out if you keep rolling it. Go slow, and go long.

FAQ

Q. Why does compound interest grow so suddenly in the later years?

Because interest earns interest, the amount you gain each year keeps getting bigger. At $10,000 and 7% a year, it barely doubles in the first decade, then nearly doubles again between year 30 and year 40 - in just ten years. The later years weigh far more than the early ones.

Q. How big is the gap between simple and compound interest after 30 years?

Starting with $10,000 at 7%, simple interest reaches $31,000 after 30 years while compound interest sits at $76,120. Same rate, same principal - whether interest earned interest is the only difference, and it splits the outcome by about 2.45 times.

Q. How do I use the Rule of 72?

Divide 72 by your return as a whole number to get the rough years to double. At 8%, 72÷8 = 9 years, almost exactly the precise figure of 9.006. Just remember it is most accurate in the 6-10% range.

Q. Is daily compounding much better than annual compounding?

The gap is smaller than you’d think. At 10% over one year, the multiple on principal is 1.10000× annually and 1.10516× daily, and neither can beat the continuous-compounding ceiling of 1.10517×. Rate and time matter far more than frequency.

Q. What should I watch out for with compounding?

The 7% is an assumption, not a guarantee - markets fluctuate and some years are negative. A nominal 7% minus 3% inflation leaves about 4% in real terms, and a 1% annual fee compounds against you over decades just as relentlessly.