What Is a REIT? The Practical Guide to Investing in Real Estate Without the Hassle

Most people know that real estate builds wealth over time. The problem is the entry price. To buy an investment property directly, you’re typically looking at a substantial down payment, years of mortgage payments, and the ongoing headache of tenants and maintenance. I’ve watched plenty of would-be real estate investors stall at exactly this step.

A REIT (Real Estate Investment Trust) is a publicly traded company that owns income-generating real estate — office towers, warehouses, hospitals — and pays out most of its rental income to shareholders as dividends. They let you invest in income-producing real estate for the cost of a single share, with all the liquidity of a publicly traded stock. Here’s how they actually work, what the risks look like, and whether they belong in your portfolio.

What Exactly Is a REIT?

A REIT is a publicly traded company that owns and operates income-generating real estate. Think office towers, shopping centers, logistics warehouses, hospitals, and data centers. The company collects rent from tenants, and most of that income flows to investors as dividends.

The key word is traded. You can buy and sell a REIT on a stock exchange the same way you’d buy any share. That’s the fundamental difference from owning property directly.

The global REIT market is estimated at roughly $2 trillion as of 2024–25. REITs originated in the U.S. in the 1960s and have since expanded to more than 40 countries. What was once an institutional tool is now accessible to anyone with a brokerage account.

How REITs Turn Rent Into Dividends

The mechanics are more straightforward than they look. Two steps:

Step 1 — Generate income from real estate An equity REIT owns physical properties and collects rent. A mortgage REIT lends money to real estate buyers and earns interest on those loans. Either way, there’s a stream of income flowing into the trust.

Step 2 — Distribute that income to investors REITs are structured to pay out a large portion of their earnings as dividends. This distribution requirement — which varies by country — is precisely why REIT dividend yields tend to run higher than the typical stock. The exact rules differ across jurisdictions, so you’ll want to check the specifics for wherever you’re investing.

I’ve seen investors focus entirely on the yield number and miss the structure behind it. Understanding where that yield comes from — and what threatens it — is what separates a thoughtful REIT investor from someone chasing a high percentage. If the mechanics of how dividends are declared and paid are still fuzzy, it’s worth getting clear on those before going deeper into REIT analysis.

Three Types of REITs

Not all REITs operate the same way. The main categories:

| Type | Primary Income Source | Key Characteristic |

|---|---|---|

| Equity REIT | Rent from owned properties | Most common type; covers offices, retail, industrial, healthcare, and more |

| Mortgage REIT (mREIT) | Interest on mortgages and MBS | Highly sensitive to interest rate moves; margin can flip quickly in a rate-hiking cycle |

| Hybrid REIT | Both owned properties and mortgages | Less common; combines the profiles of both types |

By how they trade:

- Publicly traded REITs — Listed on major exchanges. Highest liquidity and transparency.

- Non-traded REITs — Not listed publicly. Hard to exit and price discovery is opaque.

- Private REITs — Restricted to institutional investors and high-net-worth individuals.

If you’re new to REITs, publicly traded equity REITs are the sensible starting point. You get real-time pricing, easy liquidity, and public disclosure of financials.

Four Reasons REITs Belong in a Portfolio

1. Low entry barrier Buying an investment property directly requires a large upfront commitment. A single share of a publicly traded REIT can cost as little as a few dollars. That changes who gets to participate.

2. Liquidity you can actually use Selling a building takes months. Selling a REIT position takes seconds during market hours. That optionality matters, especially when circumstances change.

3. Built-in diversification A single REIT already owns multiple properties. Buy a REIT ETF and you’re spread across dozens or hundreds of properties and sectors in one transaction. How diversification actually reduces risk — and where it quietly fails is worth understanding before you assume the spread eliminates all exposure.

4. Professional management Lease negotiations, maintenance schedules, capital improvement decisions — all handled by a team whose job it is to maximize the portfolio’s performance. You receive the results without the phone calls at midnight from tenants.

The Risks — And Why Interest Rates Are the Big One

Real estate doesn’t mean risk-free. REITs have a specific vulnerability that every investor should understand clearly.

Interest rate sensitivity is the defining risk. REITs borrow heavily to acquire properties. When rates rise, borrowing costs climb and compress net income. Simultaneously, rising bond yields make fixed-income alternatives more attractive relative to REITs, pulling capital away from the sector. The 2022–2023 rate-hiking cycle was a live demonstration: REIT indexes fell sharply even as the underlying properties kept generating rent.

Other risks to keep in mind:

- Short-term correlation with equities: Publicly traded REITs track the stock market in the short run. During a broad market selloff, REITs will fall too, regardless of what’s happening to occupancy rates or lease income.

- Real estate fundamentals: Rising vacancies, falling rent, or a structurally challenged sector (office buildings post-pandemic being the obvious example) can drag on returns for years.

- Liquidity risk in non-traded and private REITs: If you can’t sell when you want to, and you don’t have reliable price data, you can end up stuck in a position you can’t exit cleanly.

REITs are not a defensive asset class. They carry both real estate risk and equity market risk. That said, the income they generate and their role in portfolio diversification can still make them valuable — if you go in with your eyes open.

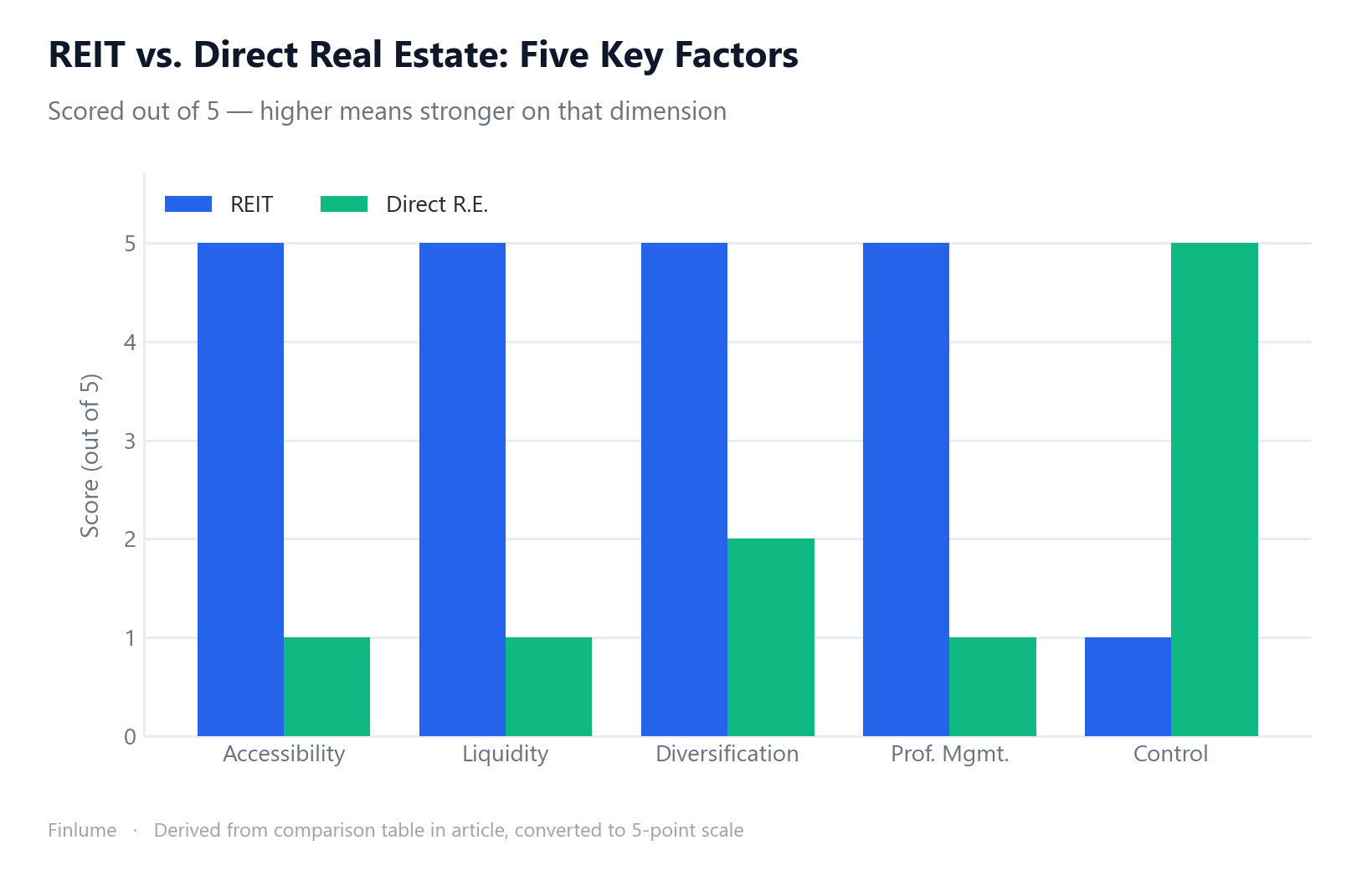

REIT vs. Direct Real Estate — A Clear Comparison

| Factor | REIT | Direct Real Estate |

|---|---|---|

| Capital required | Low (one share) | High (down payment + financing) |

| Liquidity | High (sell during market hours) | Low (months to close a sale) |

| Diversification | Automatic (multiple properties) | Concentrated (one or two assets) |

| Management burden | None (professional team) | Significant (or delegate at a cost) |

| Control | None (management decides) | High (your decisions) |

| Leverage | Set by the REIT | Your choice |

| Costs and taxes | Varies by account and country | Acquisition costs, ongoing taxes, transaction costs |

Neither is universally better. REITs win on accessibility and diversification. Direct ownership wins on control and the ability to deploy leverage on your own terms. The right choice depends on your capital, your time, and what you’re trying to achieve.

The Rate Squeeze in Numbers: What Rising Rates Actually Do to REIT Prices

The article has explained why interest rates hurt REITs. Here is what that squeeze looks like as a computed scenario — something most REIT explainers skip.

Setup (assumed inputs): A REIT trades at an index of 100 and pays a fixed dividend of 5 units per 100 invested — a 5.0% yield. The risk-free rate (government bond yield) starts at 2%, giving a yield spread of +3.0% above bonds. That spread is the premium investors demand for taking on real estate and equity risk instead of holding bonds.

When rates rise, the dividend is slow to change (leases are multi-year). The REIT yield printed on the screen stays at 5.0% — but the spread over bonds collapses. To restore the same +3.0% risk premium, the REIT price must fall until the yield (dividend ÷ price) rises enough to match the new rate plus the premium. The table below shows what that implies across seven rate scenarios.

| Risk-Free Rate | REIT Dividend Yield | Yield Spread (vs. bonds) | Implied Price Index | Price Change |

|---|---|---|---|---|

| 2% | 5.0% | +3.0% | 100.0 | baseline |

| 3% | 5.0% | +2.0% | 83.3 | -16.7% |

| 4% | 5.0% | +1.0% | 71.4 | -28.6% |

| 5% | 5.0% | 0.0% | 62.5 | -37.5% |

| 6% | 5.0% | -1.0% | 55.6 | -44.4% |

| 7% | 5.0% | -2.0% | 50.0 | -50.0% |

| 8% | 5.0% | -3.0% | 45.5 | -54.5% |

Assumptions: fixed dividend (5.0 per 100 at baseline), target spread held constant at +3.0 percentage points. Illustrative arithmetic only — real REITs adjust dividends over time and spreads fluctuate with market sentiment.

Two things stand out. First, at a 5% risk-free rate the spread hits zero — bonds and the REIT yield the same return, so there is no compensation for the additional risk. Second, each percentage-point rate increase above 2% drives a progressively larger implied price drop: the relationship is non-linear because yield and price are inversely linked. The 2022–2023 hiking cycle moved rates roughly in the 4–5% range in many markets — squarely in the territory where this table shows the largest incremental damage per additional rate point.

This also explains why falling rates act as a tailwind: the same arithmetic runs in reverse, and a REIT trading at a suppressed price can re-rate sharply upward when bond yields decline.

Key Takeaways

REITs lower the barrier to real estate investing in a meaningful way. They offer income, diversification, and liquidity that direct ownership simply can’t match at small scale. But they carry real risks — particularly rate sensitivity — that deserve serious attention.

- Understand the basic structure: real estate ownership → rent income → dividends to investors

- Know the difference between equity REITs, mortgage REITs, and hybrid REITs

- Recognize why interest rate risk is the central issue for REIT valuations

- Understand the liquidity gap between publicly traded and non-traded REITs

- Compare REIT characteristics against direct real estate ownership for your situation

- Use the yield-spread table above to translate a rate outlook into a rough price-impact estimate for REITs

One final note. If picking individual REITs feels overwhelming, start with a REIT ETF instead. A single ETF can hold dozens or hundreds of individual REITs across multiple sectors, giving you automatic diversification with one transaction. It’s the most practical entry point for most investors, and there’s no rule that says you have to get more complicated than that. For the full picture on how ETFs work and where REITs fit within a broader asset allocation strategy, those two pieces are worth reading next.

Frequently Asked Questions

Is a REIT the same as a stock? REITs trade on stock exchanges just like shares, so yes, you buy and sell them the same way. But unlike a typical growth stock, REITs are structured to pay out most of their income as dividends, which makes them behave more like income-generating assets. You’re buying a stake in a company that owns real estate, not the property itself.

Why does interest rate risk matter so much for REITs? REITs routinely use borrowed money to acquire and manage properties. When interest rates rise, their borrowing costs increase and profit margins compress. At the same time, higher yields on bonds make REITs look less attractive by comparison, which puts downward pressure on share prices. It’s a two-sided squeeze that every REIT investor should understand before they start.

What’s the difference between a REIT and a REIT ETF? A single REIT is often focused on one sector — offices, logistics, healthcare, and so on — which concentrates your risk. A REIT ETF bundles dozens or hundreds of individual REITs into one fund, spreading that sector risk automatically. For most people starting out, a REIT ETF is a more straightforward entry point.