Debt Snowball vs. Avalanche: Which Strategy Costs You Less?

With Several Debts, What Order Should You Pay Them Off?

One debt is easy. You just pay it. The trouble starts when credit cards, an overdraft, and a student loan all pile up at once. The money you can spare each month is fixed, and it is genuinely hard to know where to point it first.

One thing worth settling first: not all debt is the same. Knowing how to tell good debt from bad debt makes it much clearer which balances deserve your most aggressive attack.

When I started cleaning up my own debt, my plan was basically “throw a little at everything.” It took me far too long to realize that is the slowest and most expensive approach there is. The order you pay things off changes your total interest, your debt-free date, and even the odds you stick with the plan at all. Let’s walk through the two big strategies: snowball and avalanche.

The Snowball Method: Smallest Balance First, Quick Wins

The snowball method targets the debt with the smallest balance first. You pay only the minimum on everything else and throw every spare dollar at that one smallest balance.

Once it’s gone, you take the payment you were making on it and roll it onto the next-smallest debt. Each debt you kill makes the amount rolling onto the next one bigger. Like a snowball picking up size as it rolls downhill, which is exactly where the name comes from.

The point is that your count of paid-off debts drops fast. Crossing a line off the list feels great, and anyone who’s done it knows that little hit of momentum is real.

The Avalanche Method: Highest Rate First, Lowest Cost

The avalanche method goes after the debt with the highest interest rate (APR) first. Same drill: minimums on everything else, spare cash concentrated on the highest-rate debt. When it’s cleared, you move to the next-highest rate.

What the two methods share is clear. (a) You pay the minimum on every debt, (b) you keep the same fixed total payment each month, and (c) you roll a paid-off balance’s payment onto the next target. The only difference is the order.

Why is avalanche so powerful? Simple: it removes your most expensive money first, the debt growing interest fastest. So avalanche always costs the least interest (or ties) and reaches debt-free in the shortest time (or ties). It is the mathematically optimal route.

By the Numbers: Same Money, Different Outcome

Words only get you so far, so I ran the math. Assume three debts and a fixed total of $500 a month.

| Debt | Balance | APR | Minimum |

|---|---|---|---|

| A | $1,000 | 5% | $25 |

| B | $3,000 | 12% | $60 |

| C | $6,000 | 20% | $120 |

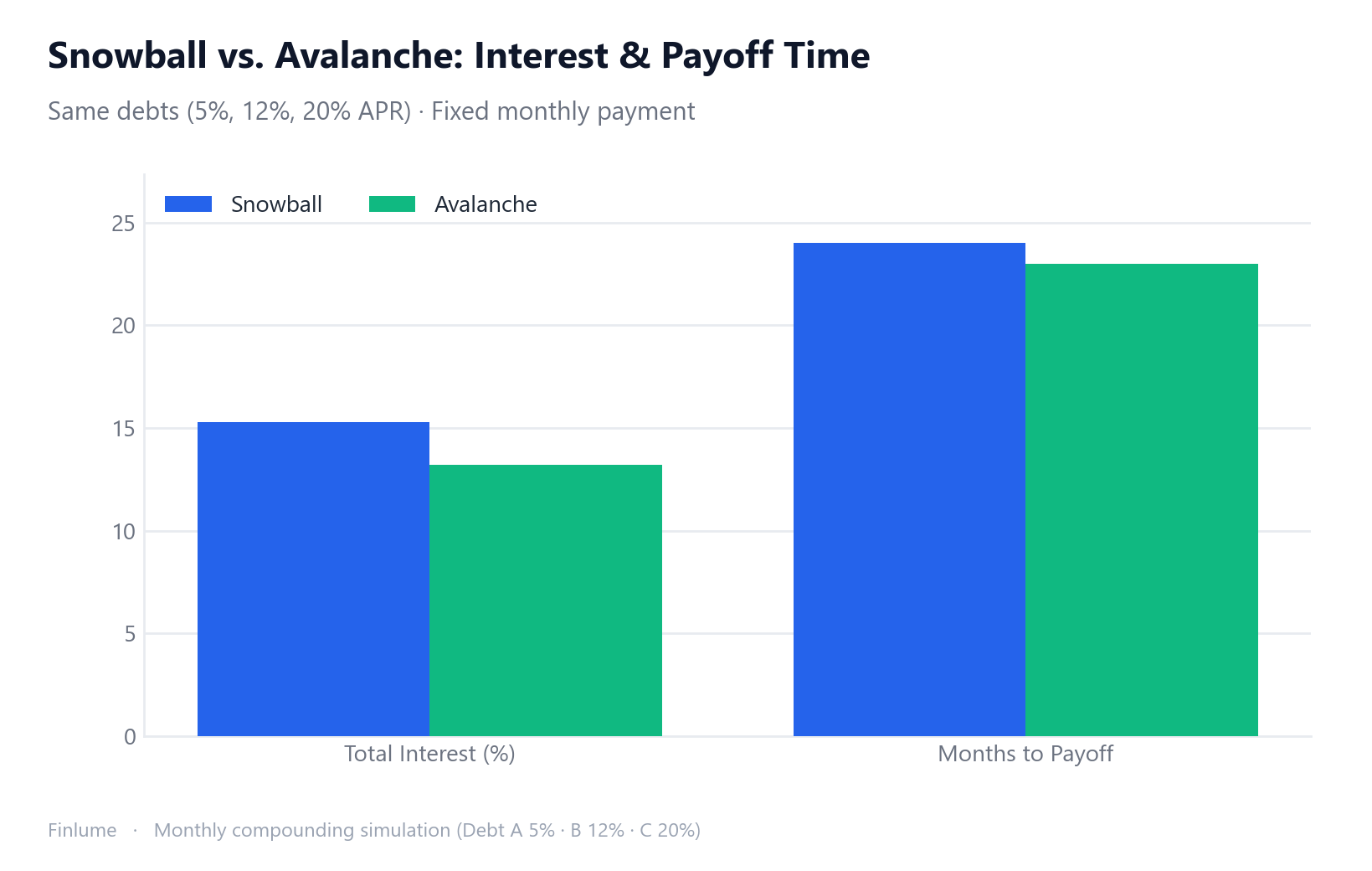

Here’s the result, simulated with monthly compounding and the leftover cash after minimums concentrated on one target.

| Method | Order | Total time | Total interest |

|---|---|---|---|

| Snowball | A→B→C (smallest first) | 24 months | ~$1,531 |

| Avalanche | C→B→A (highest rate first) | 23 months | ~$1,318 |

Avalanche saves about $213 in interest and finishes one month sooner. Leaving a high-rate debt sitting there is the mirror image of how investment fees quietly erode your compounding: in one case compounding works for you, in the other it works against you. The key takeaway: the wider the rate gap, the bigger avalanche’s edge. This example spanned 5% to 20%, a big gap. Flip it around: if your debts carry similar rates, the difference in total interest shrinks to nearly nothing.

Money vs Motivation: What Behavioral Research Says

So is avalanche always the answer? On paper, yes. But we’re people, not calculators.

A 2012 study by David Gal and Blakeley McShane in the Journal of Marketing Research is worth knowing. Analyzing real consumer debt data, they found the strongest predictor of paying off all your debt wasn’t interest saved. It was the share of debt accounts you’d already paid in full.

In other words, people who cleared small debts first and banked those small wins were more likely to finish the whole journey. Follow-up work covered by Harvard Business Review echoes this: when progress is visible (the number of debts shrinking), motivation and persistence go up. Snowball isn’t mathematically optimal, but it raises the odds a real human actually sees the plan through.

Choosing the Method That Fits You

The right answer depends on you.

- Weak self-control or a history of quitting a payoff plan partway → snowball. The quick wins help you finish.

- Comfortable with numbers and confident you’ll push through → avalanche. It saves the most interest.

- Debts at similar rates → the cost difference is tiny, so picking the more motivating snowball costs you little.

Personally, I’d suggest a hybrid: knock out one or two very small debts fast to build confidence, then switch to highest-rate order for the rest. You feed your motivation and your wallet at the same time.

Principles and Cautions for Either Method

There’s a foundation that matters more than the order itself. I’ll say this part plainly, no jokes.

- Always pay every minimum on time. Late payments mean fees and credit damage.

- Don’t take on new debt. Paying one down while borrowing elsewhere cancels the whole effort.

- Keep a small emergency fund. It stops a surprise expense from dragging you back into debt. (See how much you really need and how to build it.)

And finally, whichever method you choose, the principle of “concentrate spare cash on one debt and roll each payoff onto the next” always beats spreading a little across everything. Always faster, always cheaper.

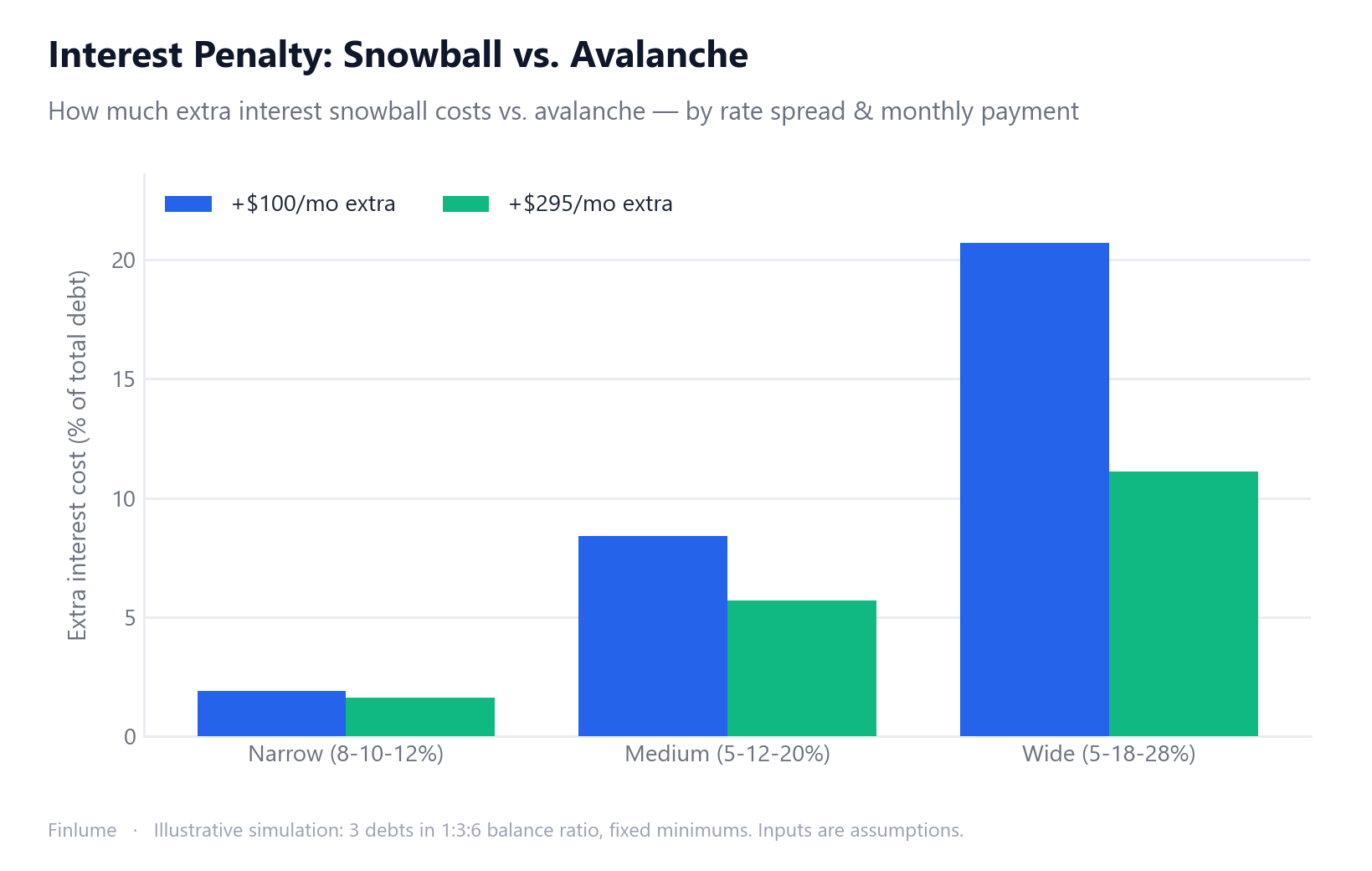

How Much Does the Order Choice Actually Cost? A Rate-Spread Lookup

The existing example uses a 15-percentage-point rate gap (5% to 20%), which is wide. But what if your debts are closer together — or further apart? This table shows the interest penalty of choosing snowball over avalanche, expressed as a percentage of your total initial debt, across realistic rate-spread combinations.

| Rate spread (low / mid / high APR) | Modest extra payment | Standard extra payment |

|---|---|---|

| Narrow (8% / 10% / 12%) | +1.9% of debt | +1.6% of debt |

| Medium (5% / 12% / 20%) | +8.4% of debt, +3 months | +5.7% of debt |

| Wide (5% / 18% / 28%) | +20.7% of debt, +7 months | +11.1% of debt, +4 months |

Assumptions: three debts in a 1:3:6 balance ratio (e.g., $1k / $3k / $6k, total $10k); fixed minimums of 2.5%, 2%, and 2% of balance; “modest” = $100/mo above minimums, “standard” = $295/mo above minimums. Monthly compounding. Illustrative only.

Two things stand out. First, at a narrow spread (8-10-12%), the snowball’s interest penalty is only about 1.6–1.9% of total debt — a genuinely small price for the motivational benefit, which may well be worth paying. Second, at a wide spread (5-18-28%) with a modest payment budget, snowball costs an additional 20.7% of your total debt in interest and takes 7 months longer. At those numbers, the method choice is no longer a lifestyle preference — it is a material financial decision.

The practical read: check your own rate spread before choosing. If the gap between your highest and lowest rate is under 5 percentage points, pick the method that keeps you motivated. If the gap is 10+ points — and especially if your extra monthly payment is small — avalanche has a hard financial case that is hard to ignore.

Key Takeaways

- Avalanche (highest rate first) costs the least interest — mathematically optimal

- Snowball (smallest balance first) raises your odds of finishing — the behavioral edge

- Big rate gaps favor avalanche; similar rates favor snowball

- Narrow rate spread (under 5 pp gap)? The cost difference is tiny — pick snowball freely

- Wide rate spread + tight budget? Avalanche can save 10–20%+ of your total debt in interest

- If you need confidence, a hybrid is a smart middle road

- Minimums on time + no new debt + an emergency fund are non-negotiable

🧮 Run your payoff: Enter your balance, rate, and monthly payment into the debt payoff calculator to see your payoff time and total interest.

Frequently Asked Questions

Which is better, snowball or avalanche?

On total interest, the avalanche (highest rate first) always costs the least or ties, so it’s mathematically optimal. But research shows the snowball (smallest balance first) raises your odds of finishing. Pick avalanche if numbers come first, snowball if motivation and persistence matter more.

Which method wins when the rates are close together?

When your debts carry similar rates, the difference in total interest shrinks to nearly nothing. In that case the cost penalty is tiny, so choosing the more motivating snowball costs you almost nothing.

What about the minimum payments?

Both methods require paying every minimum on time, and you only concentrate your spare cash on one debt on top of that. Late payments mean fees and credit damage, so this rule comes before any payoff order.

Can I combine snowball and avalanche?

Yes, a hybrid can be a smart choice. Knock out one or two very small debts fast to build confidence, then switch to highest-rate order for the rest. That way you feed both your motivation and your wallet.

The moment you decide on an order, you’re already halfway done. Write out your list today. You’ve got this.