Emergency Fund 101: How Much You Need and How to Build It Fast

Whenever I talk money with someone, the same line comes up first: “I want to start investing.” And I always ask one thing before anything else: “If your fridge died tomorrow, could you fix it without reaching for a credit card?” A lot of people pause. An emergency fund isn’t glamorous, but it’s the ground floor of every financial plan. If the floor is weak, the upper stories don’t matter.

1. What an Emergency Fund Is, and Why You Actually Need One

An emergency fund is money set aside for the things you can’t predict: a job loss, a medical bill, a sudden repair. The key mindset shift is this: it’s not money for “just in case” — it’s money for “when, not if.”

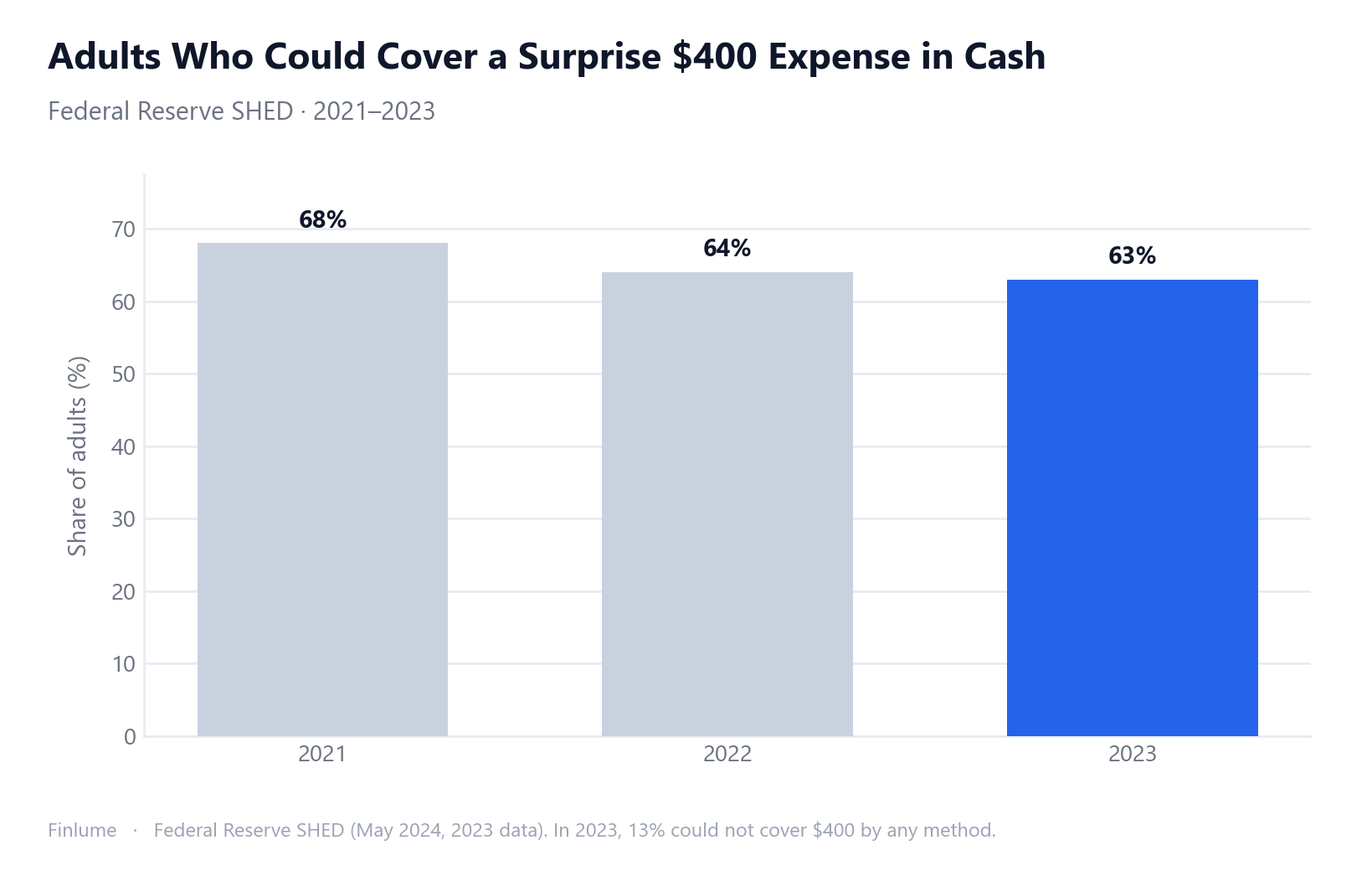

The Federal Reserve’s Survey of Household Economics and Decisionmaking (SHED, released May 2024, covering 2023) makes that concrete. Only 63% of adults said they could fully cover a surprise $400 expense with cash or its equivalent (savings, or a card paid off on the next statement). Flip that around: roughly 37% couldn’t fully absorb even a $400 shock with cash alone.

Without a buffer, a small shock turns into high-interest debt. You carry a card balance, interest piles on, and next month it’s even harder to pay down — the familiar spiral. An emergency fund cuts the fuse before it lights.

2. The Vulnerability in Numbers, and How Much Is Enough

The year-over-year trend tells a story: 68% in 2021 → 63% in 2022 → 63% in 2023. Pandemic-era support nudged it up briefly, then it dropped sharply and has held there. And in 2023, a sobering 13% of adults said they couldn’t pay the $400 by any method at all.

So how much is enough? The standard recommendation is 3-6 months of essential expenses. The word that matters is essential — not total spending. Rent or mortgage, food, utilities, transport, insurance, minimum debt payments — the things that don’t stop when a crisis hits. Dining out, travel, subscriptions? Those are discretionary; you can dial them down, so they usually don’t count.

| Your situation | Target |

|---|---|

| Stable job, dual income, few dependents | Closer to 3 months |

| Single income, dependents, shaky industry | 6 months or more |

| Self-employed / freelance / variable income | Up to 6-12 months |

Aiming for six months on day one is how people never start. Build a small “one-month buffer” first, then grow it.

3. Sizing Your Target: Essential Spending x Months

The formula is simple: target = monthly essential spending x months of coverage.

Let’s feel it as ratios. If essentials are about 50% of your income and you save 20% of income, then six months of essentials equals 3.0x your monthly income (6 x 0.5). Divide: 3.0 ÷ 0.20 = 15 months to fully fund six months of coverage. If that 20% feels arbitrary, start with what savings rate to actually aim for.

In plain numbers: if essentials are 600 a month and you want six months, that’s 3,600. Save 200 a month and 3,600 ÷ 200 = 18 months to finish.

The target looks big, but skim a steady percentage and you usually get there within one to two years. The trick isn’t doing it “all at once” — it’s “automatic and gradual.”

3a. The Hidden Price Tag of Skipping the Fund

Knowing how much to save is useful. Knowing what it costs you not to is what makes it urgent.

When an emergency hits with no fund in place, the typical move is to put the expense on a credit card and pay it off over the next several months. That’s not just inconvenient — it’s a quantifiable premium on top of the original emergency.

The table below shows interest paid as a percentage of the original emergency amount, computed for three common card APRs and four realistic payoff timelines (all arithmetic, no estimates):

| Payoff period | 20% APR | 24% APR | 28% APR |

|---|---|---|---|

| 6 months | 5.9% | 7.1% | 8.3% |

| 12 months | 11.2% | 13.5% | 15.8% |

| 18 months | 16.6% | 20.1% | 23.6% |

| 24 months | 22.1% | 26.9% | 31.7% |

Assumptions: equal monthly payments, stated annual rate compounded monthly. Computed figures, not estimates.

Read that middle column plainly: if you carry a 24% APR card and take 12 months to clear the balance, you pay 13.5% on top of whatever the emergency actually cost. Stretch repayment to 18 months and that surcharge grows to 20.1% — a fifth of the original bill, paid for nothing but the privilege of not having saved first.

The counterargument is that keeping cash in a savings account has an opportunity cost too: you could invest it instead. Keeping an emergency fund in a high-yield savings account (assume 4.5% APY) instead of a diversified portfolio (assume 7% annual return) costs roughly 2.5 percentage points per year in foregone return. By contrast, even a single 12-month payoff at 24% APR costs 13.5% of the original amount — already more than 5× the annual opportunity cost of holding the fund. The math consistently favors building the fund.

- Understood the real cost of financing emergencies on credit: 11–32% extra depending on rate and timeline

4. Where to Keep It: Balancing Liquidity, Safety, and a Little Yield

You choose the home for your fund by balancing three principles.

- Liquidity: you can pull it out within days, with no penalty.

- Safety: you don’t park it in something whose value swings (like stocks).

- A little yield: take some interest to offset inflation, but never put yield ahead of liquidity and safety.

Good homes: a high-yield or online savings account, a money-market-style account, and a slice in short-term certificates of deposit — only a portion, and laddered so maturities are staggered.

I’ll drop the jokes here, because this part matters. Park your fund in stocks and you risk needing it exactly when the market is down, locking in a loss as you withdraw (timing risk). Park all of it in zero-interest cash and inflation quietly eats its real value (cash drag). That’s why “safe plus a little interest” is the answer.

5. How to Build It: Auto-Transfer, Separate Account, 50/30/20

Willpower is unreliable. Trust the system instead.

- Pay yourself first: set an automatic transfer to your emergency account on payday, so you live on what’s left after saving, not save what’s left after living.

- Separate the account: keep it out of sight from your everyday account and impulse spending drops.

- The 50/30/20 rule: 50% of after-tax income to needs, 30% to wants, 20% to saving and debt payoff. Point that 20% at filling the fund first. If you’d rather give every dollar a job, zero-based budgeting pairs well here.

- Use windfalls: route bonuses, tax refunds, and side income straight to the fund to accelerate.

Starting small but automatic beats waiting to start big. That’s the whole game.

6. Common Mistakes, and the Refill Rule

The mistakes I see again and again: mixing the emergency fund with investments or goal savings (a trip, a house) in one pot; setting the target so high you never begin; spending the fund and never refilling it; stashing it somewhere locked up or volatile and losing liquidity.

The last two deserve emphasis. An emergency fund isn’t spent once and forgotten — refilling whatever you draw down is part of running it.

Key takeaways checklist

- Calculated my monthly essential spending (discretionary excluded)

- Picked a target in months that fits my situation (3-6, more if income is variable)

- Started with a small “one-month buffer” first

- Moved the fund into a liquid, safe, separate account

- Set up an automatic transfer on payday

- Remembered the refill rule after any withdrawal

- Understood that financing emergencies on credit costs 11–32% extra vs the original bill (computed, not estimated)

An emergency fund isn’t money for getting rich. It’s the money that lets you stand back up when life stumbles once. Start small today — even a single auto-transfer line is a real beginning.

🧮 Size your fund: Enter your monthly expenses and target months into the emergency fund calculator to see your number and how long it takes to reach it.

FAQ

How much should an emergency fund be? The standard recommendation is 3-6 months of essential expenses — not total spending, but rent or mortgage, food, utilities, transport, insurance, and minimum debt payments. If your income is variable, as with self-employment or freelancing, stretching to 6-12 months is safer.

How do I calculate my emergency fund target? The formula is monthly essential spending multiplied by months of coverage. For example, if essentials are 600 a month and you want six months, you need 3,600; saving 200 a month finishes it in 18 months. Start with a small one-month buffer and grow from there.

Where should I keep my emergency fund? Choose the home by balancing liquidity, safety, and a little yield. A high-yield or online savings account, a money-market-style account, and a laddered slice of short-term certificates of deposit all work. Avoid stocks or other volatile assets, since you risk locking in a loss right when you need the money.

What do I do after I spend my emergency fund? An emergency fund isn’t spent once and forgotten — refilling whatever you draw down is part of running it. After a withdrawal, point your automatic transfers back at the fund first and rebuild it to your target before redirecting that money elsewhere.

Should I build an emergency fund before investing? Yes. The fund is the ground floor of every financial plan. Without a buffer, a small shock turns into high-interest debt that drags on your returns. Secure at least a minimal buffer first, then scale up your investing.