Good Debt vs. Bad Debt: 4 Ways to Tell Them Apart

1. Is All Debt Bad?

For a long time I believed debt was simply something to wipe out, no exceptions. Then I spent enough years actually handling money to notice something: there’s debt that moves you toward wealth, and debt that quietly eats away at it.

The idea is simple. Does this debt help future-you earn more, or does the money just vanish? Get that one lens right and the whole picture changes.

2. What Is Good Debt?

Good debt is borrowing used to buy an appreciating asset, or to grow your future income or net worth. It usually carries a lower interest rate, too.

The classic examples are three: a mortgage (real estate that tends to appreciate), student loans (an investment in your earning power), and business financing (a tool that makes money). See the pattern? In each case, money borrowed today is structured to create more money tomorrow. (Investopedia, Bankrate, Fidelity)

3. What Is Bad Debt?

Bad debt is the opposite. It funds something that loses value over time, or pure consumption, and it comes with a high interest rate.

Credit card revolving balances, payday loans, and luxury splurges are the textbook cases. Car loans sit in a gray zone—a car depreciates fast the moment you drive it off the lot, which leans “bad,” but if you genuinely need it to get to work, it’s not that simple. Don’t label it blindly; just ask whether you truly need it, and whether you’re buying more car than you should.

4. The Four Tests

Here’s the frame I actually use:

- Interest rate — the lower, the better. If the rate is higher than the asset’s expected return, it’s bad debt.

- Asset direction — if what you buy goes up (real estate, education, business), good debt; if it goes down (consumer goods, cars), bad debt.

- Net worth impact — if it grows your net worth long term, good debt.

- Income creation — if it helps you earn more later, good debt.

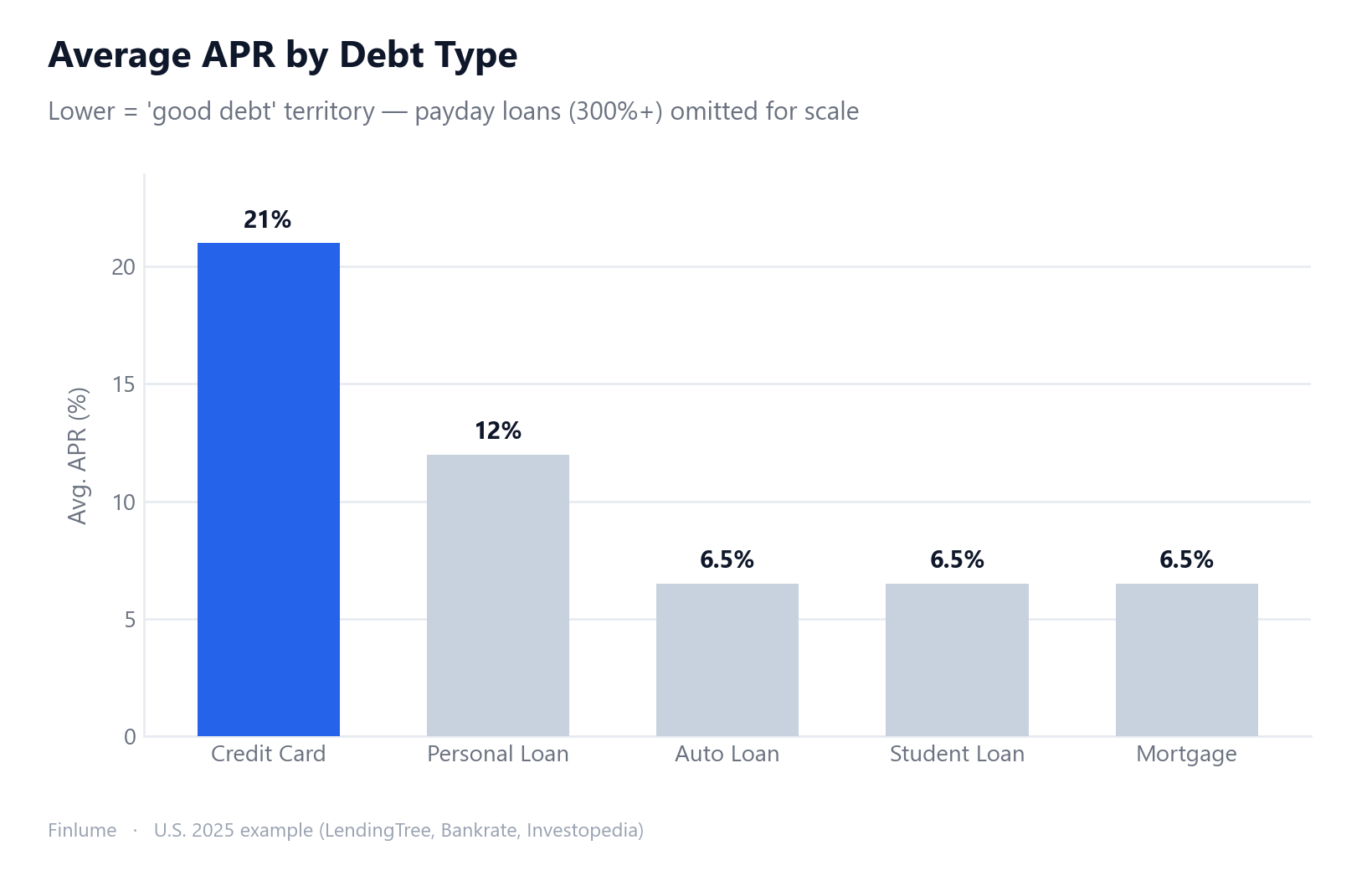

Interest rates get intuitive once you see the debt “pecking order.” Below is a U.S. 2025 example—the absolute numbers vary by country and time, but the ranking is roughly universal.

| Debt type | Avg. rate (U.S. 2025 example) |

|---|---|

| Payday loan | 300–400% APR or more |

| Credit card | ~20–22% APR |

| Personal loan | ~12% APR |

| Auto loan | ~6–7% APR |

| Student loan | ~6.5% APR |

| Mortgage | ~6–7% APR |

Cards and payday loans are the priciest; mortgages and student loans are the cheapest. That ranking holds almost everywhere. (LendingTree, Investopedia, Bankrate)

5. When Good Debt Turns Bad

This is the part that matters most, so I’ll drop the jokes here. Even good debt becomes bad debt when there’s too much of it.

A mortgage stretched past what you can afford, student loans that never lift your earning power, leverage that’s heavy relative to your income and assets, or a variable rate that swells over time—each is a moment where good debt flips bad.

There are widely used rules of thumb (not laws) to anchor you. By DTI (debt-to-income ratio): 35% or below is healthy, 36–43% is manageable but a signal to stop borrowing more, 43% is often cited as the ceiling for a Qualified Mortgage approval in the U.S., and 50%+ is a warning light. The 28/36 rule suggests housing costs under 28% of gross income and total debt payments under 36%. (Investopedia, CFPB, Bankrate)

6. The Minimum-Payment Trap—Pay Off High-Rate Debt First

Credit card minimum payments look friendly, but they’re actually engineered to keep you in debt longer. Whether the balance is $50 or $5,000, paying only the minimum can stretch repayment over many years, and the total interest often rivals the principal itself. (Bankrate)

So the strategy is clear: attack your highest-rate debt first (the avalanche method). Look back at the ranking table—killing payday loans and credit cards first is mathematically the fastest route out. For a deeper look at payoff order, see debt snowball vs. avalanche.

The same logic works in reverse when you’re building wealth. Just as a high rate compounds your debt, fees that erode compounding quietly shrink your investment returns.

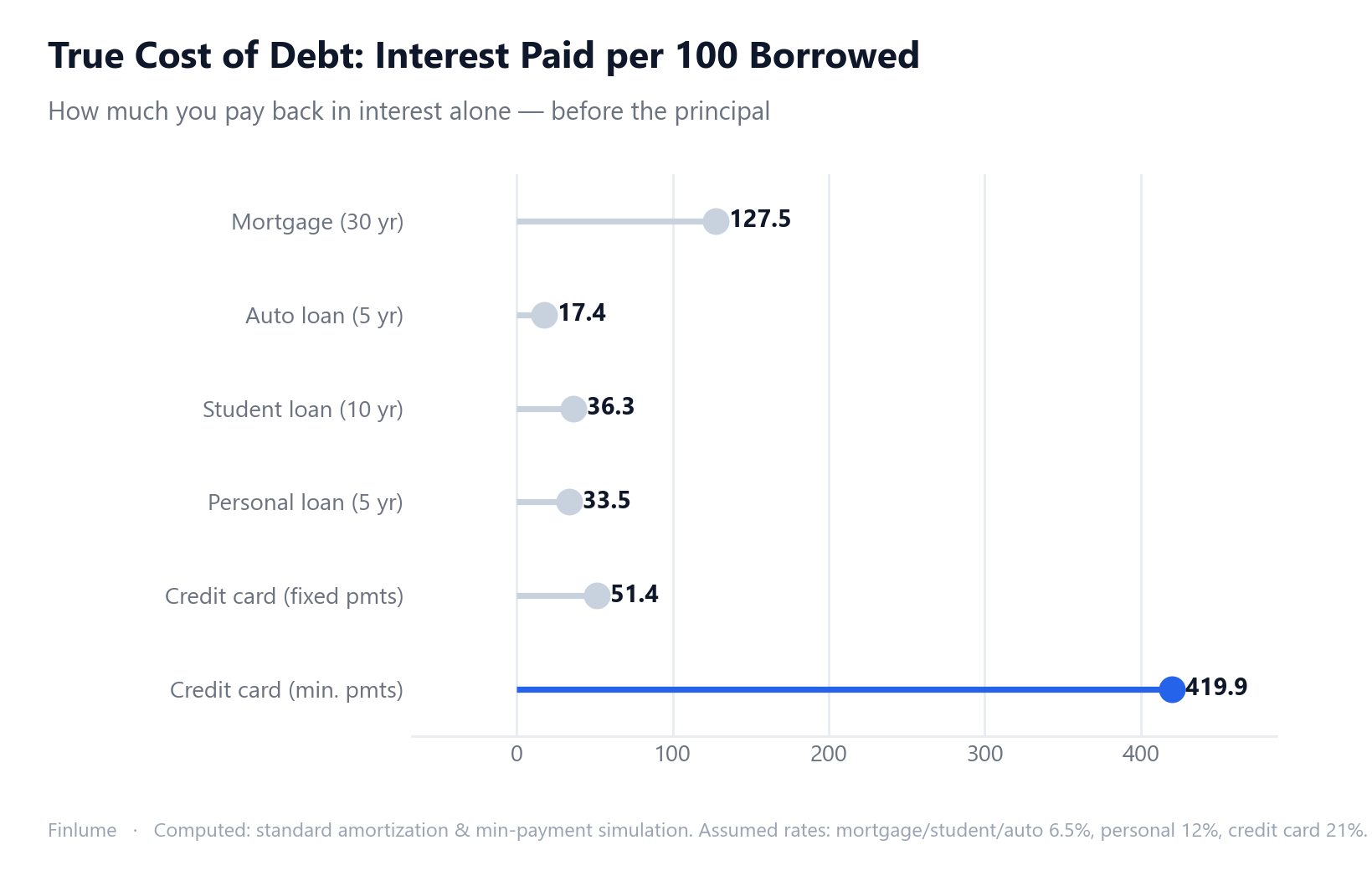

7. The True Cost Multiplier: How Much Interest You Actually Pay

Generic articles tell you credit card debt is expensive. Here’s the number that makes it real. The table below shows how much interest you pay per 100 units borrowed — assuming typical rates and either a standard amortizing repayment or credit card minimum payments (2% of balance, with a $10-equivalent floor per $1,000 of balance). All figures are computed from standard loan-amortization formulas; assumed rates are illustrative.

| Debt type | Assumed rate | Term | Interest per 100 borrowed | Multiplier |

|---|---|---|---|---|

| Mortgage | 6.5% | 30 yr | 127.5 | 1.28× |

| Student loan | 6.5% | 10 yr | 36.3 | 0.36× |

| Auto loan | 6.5% | 5 yr | 17.4 | 0.17× |

| Personal loan | 12% | 5 yr | 33.5 | 0.33× |

| Credit card — fixed payments (3%/mo) | 21% | 4.2 yr | 51.4 | 0.51× |

| Credit card — minimum payments only | 21% | ~33 yr | 419.9 | 4.20× |

The last two rows are the same debt — same balance, same 21% rate — but completely different outcomes. Pay a fixed amount each month and you clear it in 4 years, paying 51 in interest per 100 borrowed. Pay only the minimum and you’re still paying it off 33 years later, with 420 in interest — more than four times the original balance, paid purely in interest.

That gap — 51.4 vs. 419.9 — is the real cost of bad debt behavior, not just bad debt type. A credit card that you pay off aggressively is actually cheaper than a 30-year mortgage in total interest paid (0.51× vs. 1.28×).

8. Your Debt Self-Check

Ask yourself just three questions:

- Does this debt buy something that rises in value?

- Is the rate lower than the asset’s expected return?

- Does it grow my future income or net worth?

Key takeaways

- Good debt = appreciating asset, future income, low rate. Bad debt = depreciation, consumption, high rate.

- The four tests: interest rate, asset direction, net worth, income creation.

- Even good debt goes bad in excess. Use DTI 35% and 28/36 as rules of thumb.

- High-rate debt first; sidestep the minimum-payment trap.

- The minimum-payment trap in numbers: the same credit card balance costs 4.20× the principal in interest on minimum payments — vs. 0.51× on a fixed repayment schedule. Same debt, 8× more interest.

You don’t have to fear debt itself—only the wrong kind of debt. Run your balances through those three questions today.

Frequently Asked Questions

What separates good debt from bad debt?

Four tests: interest rate, asset direction, net worth impact, and income creation. If the debt buys an appreciating asset, carries a rate below that asset’s expected return, and grows your future income or net worth, it’s good debt. The opposite is bad debt.

Is a car loan good debt or bad debt?

A car depreciates fast the moment you drive it off the lot, which leans toward bad debt. But if you genuinely need it to get to work, it sits in a gray zone. Just ask whether you truly need it and whether you’re buying more car than you should.

What DTI ratio should I stay under?

As a rule of thumb, 35% or below is healthy, 36–43% is manageable but a signal to stop borrowing more, 43% is often cited as the ceiling for a Qualified Mortgage approval in the U.S., and 50%+ is a warning light. The 28/36 rule suggests housing under 28% of gross income and total debt payments under 36%.

Which debt should I pay off first?

Attack your highest-rate debt first—the avalanche method—because it’s mathematically the fastest route out. Payday loans and credit cards are usually the priciest, so clear those first and avoid the minimum-payment trap.