Zero-Based Budgeting: Give Every Dollar a Job and Stop Losing Track

The first time I tried to budget seriously, I hit a wall. Money landed in my account every month, yet by the end of it I was always asking the same question: “Where did all of that go?” That’s when I ran into zero-based budgeting. Despite the intimidating name, the idea is surprisingly simple.

1. What Is Zero-Based Budgeting? — The Real Meaning of “Income − Every Allocation = 0”

Zero-based budgeting (ZBB) fits in one sentence: you give every dollar a job, so that income minus everything you’ve allocated equals zero.

The most misunderstood part is that “zero.” It does not mean “spend your whole paycheck.” It means “the amount of unassigned, floating money is zero.” The key insight is that saving, investing, your emergency fund, and debt repayment are all treated as spending (allocation) categories too. Setting aside $400 to save isn’t leftover money — it’s $400 sent to do the job called “savings.”

Mathematically it’s just an identity. Say your monthly income is $3,000:

| Category | Allocation |

|---|---|

| Housing | $1,000 |

| Food | $400 |

| Transport | $200 |

| Utilities | $150 |

| Savings | $400 |

| Investing | $300 |

| Debt repayment | $250 |

| Fun / misc | $300 |

| Total | $3,000 |

Add it all up and it matches your income exactly. The leftover balance is zero.

2. Where It Came From — From Corporate Budgets to the Kitchen Table

ZBB wasn’t built for households. In the late 1960s to around 1970, Peter Pyhrr designed it at Texas Instruments as a corporate budgeting technique. The corporate idea was blunt: “start from zero every period and justify every expense from scratch.” No more spending something just because you spent it last year.

When the concept crossed over into personal finance, it got a friendlier phrasing: “give every dollar a job.” Don’t let a single dollar sit around idle. Honestly, that line is what finally made budgeting click for me — it felt less like accounting and more like hiring.

3. How to Actually Build One — 5 Steps

Having done this myself, the order is what keeps it simple.

- Add up expected net income for one cycle (usually a month) — the money you’ll actually receive.

- Allocate fixed costs first: housing, utilities, phone, minimum debt payments — the stuff that barely moves.

- Allocate variable costs: food, transport, household goods — the items that swing month to month.

- Allocate financial goals: emergency fund, savings, investing. The trick is treating these as essential, not as an afterthought. To size these, how much emergency fund you actually need and what savings rate to aim for make the numbers easy to set.

- Adjust until the balance hits zero. Money left over? Add to goals or savings. Coming up short? Trim variable spending.

Here’s the line that separates ZBB from everything else: you start from scratch every cycle. It’s not “copy last month’s budget” — it’s a blank page each time.

4. The Upside — Control and Goals at the Same Time

The biggest win is visibility. Every dollar wears a name tag, so you always know where it went. It was only after switching to ZBB that I spotted the small subscriptions and impulse buys quietly leaking out each month. If impulse buying is your leak, systems beat willpower — see 7 psychology-backed strategies to stop impulse buying. For finding and cutting accidental, wasteful spending, nothing beats it.

The second win is enforcement. Because saving, investing, and debt repayment become pre-allocated must-haves rather than “if there’s anything left” options, your goals naturally rise to the top. And since you re-examine priorities every month, the plan flexes as life changes.

5. The Downsides and Cautions — Time, Irregular Income, Emergencies

I’ll be straight with you: it takes work. Tracking and allocating every category each cycle is more hands-on than a simple method like 50/30/20.

It’s especially tricky for people with irregular or variable income. If your earnings are hard to predict, there are two fixes. Budget based on your lowest expected income for the month, or put money you receive now into next month’s budget so you’re always living a month ahead.

Two things you cannot skip. First, keep a “buffer” or “miscellaneous reserve” category for emergencies — car repairs, medical bills — or the system won’t survive contact with reality. Second, don’t build it too tight. Give “fun” a real, non-zero allocation. A budget with no room to breathe is a budget that collapses.

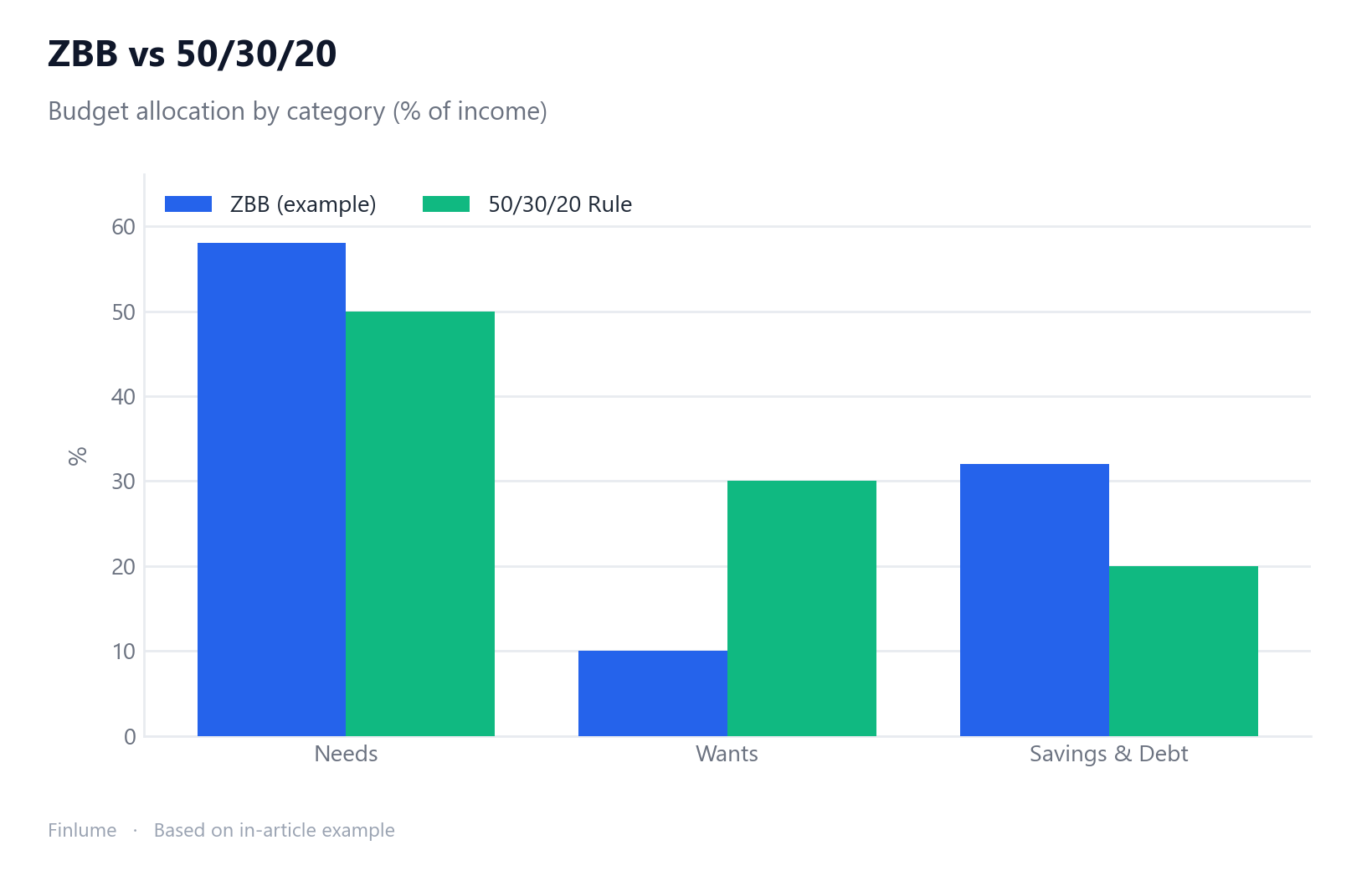

6. Compared to 50/30/20 — Precision vs. Simplicity

The usual comparison is the 50/30/20 rule, popularized by Elizabeth Warren: 50% to needs, 30% to wants, 20% to savings and debt repayment.

| Aspect | Zero-Based Budgeting | 50/30/20 Rule |

|---|---|---|

| Method | Allocate every category until zero | Three broad percentages |

| Flexibility | Precise but tight | Simple and loose |

| Effort | Track every cycle, hands-on | Low |

| Best for | People who want fine control | People who want simplicity |

Neither is “correct.” Need precision? ZBB. Need a low-effort big-picture frame? 50/30/20.

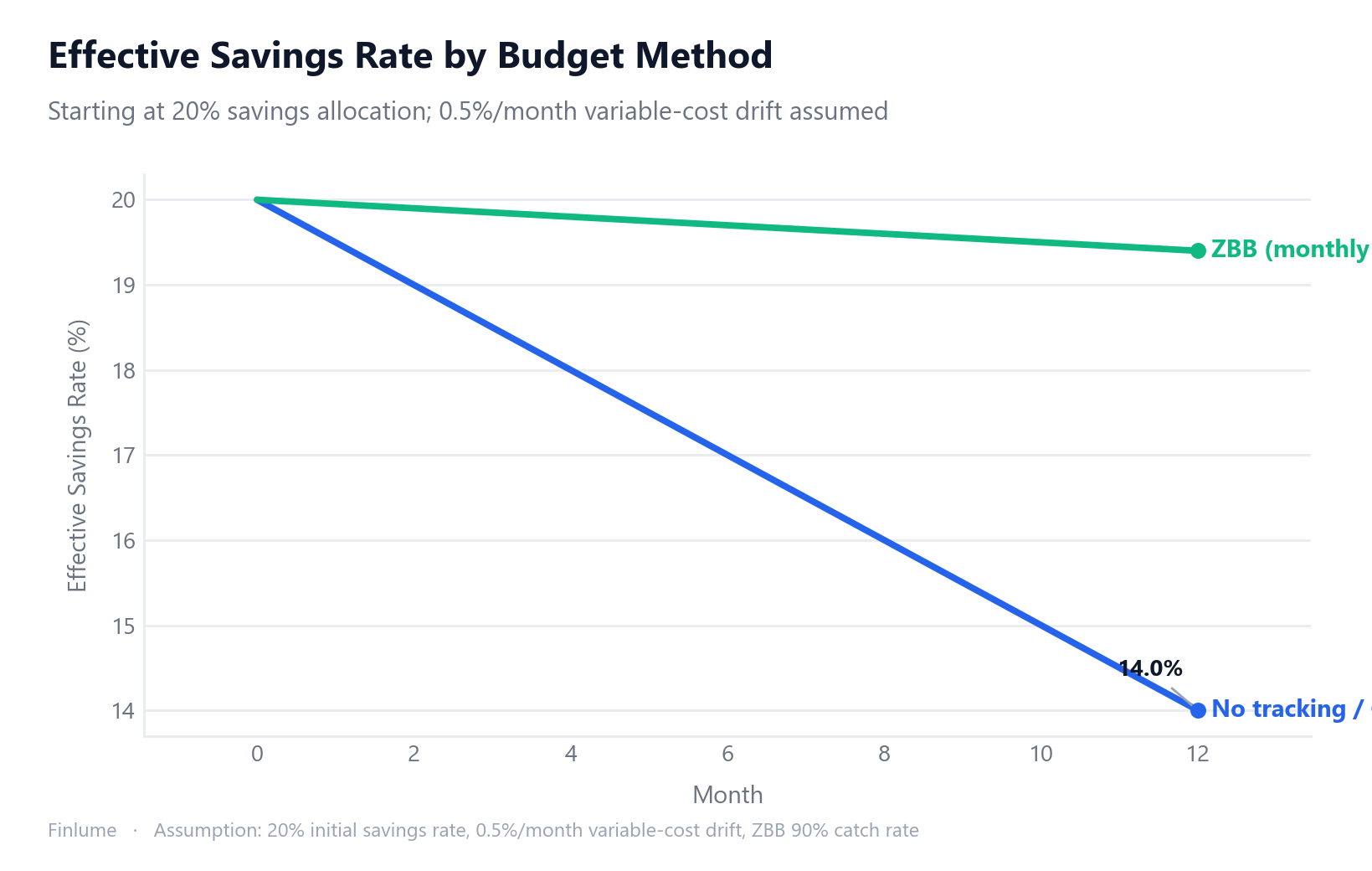

7. The Drift Problem — Why Monthly Reallocation Protects Your Savings Rate

The comparison table above captures the method difference. But there is a compounding arithmetic consequence that rarely gets spelled out: budget drift quietly erodes your savings rate over time, and ZBB’s monthly reallocation is the structural antidote.

Here is how it plays out in practice. Suppose you set a 20% savings allocation at the start of the year — a reasonable, common target. In a copy-paste or set-and-forget budget, variable spending tends to creep up by small amounts: a new streaming service here, slightly higher grocery bills there. A reasonable estimate for this unnoticed drift is around 0.5% of income per month. ZBB’s monthly review catches and corrects most of it (estimated 90% catch rate); a copy-paste budget catches none until you notice the damage.

Assumption: 20% starting savings allocation; 0.5% of income per month unnoticed variable-cost drift (illustrative).

| Month | No tracking / Copy-paste budget | ZBB (monthly reallocation) |

|---|---|---|

| 1 | 19.5% | 19.9% |

| 3 | 18.5% | 19.9% |

| 6 | 17.0% | 19.7% |

| 9 | 15.5% | 19.6% |

| 12 | 14.0% | 19.4% |

After 12 months, the copy-paste budget’s effective savings rate has slid to 14.0% — a loss of 6 percentage points from the original intent. ZBB holds at 19.4%, giving up only 0.6 points. The gap is 5.4 percentage points of savings per month.

What does that mean in real terms? If your goal is to build a 6-month emergency fund and you started intending to save 20%:

- Without ZBB (average effective rate 17.0% due to drift): reaches the target in 35.3 months.

- With ZBB (average effective rate 19.7%): reaches the target in 30.5 months.

That is 4.8 months sooner — not because ZBB is magic, but because the monthly blank-page reallocation forces you to see and correct the drift before it compounds.

8. Who It Fits and Who It Doesn’t — A Self-Check Checklist

Let me pull it together.

A good fit if you:

- want detailed control over your money’s movement

- are paying down debt fast or have aggressive savings goals

- have no idea where your money keeps leaking

- are willing to log spending in a notebook or app consistently

- want to protect your savings rate from silent drift (the monthly reallocation keeps it anchored)

Less of a fit if you:

- have almost no time to spend on tracking

- have highly irregular income that’s hard to forecast (workable, but harder)

- simply prefer simplicity → here, a percentage-based budget like 50/30/20 is the realistic alternative

In my experience, the real payoff of ZBB was never hitting a perfect zero. It was the monthly act of giving each dollar a job and, in doing so, reminding myself what I actually value. Try one month from a blank page. You may find your priorities get organized before the numbers do.

FAQ

Q. Does the “zero” in zero-based budgeting mean spending your whole paycheck?

No. The zero means the amount of unassigned, floating money is zero. Saving, investing, your emergency fund, and debt repayment are all treated as allocation categories, so setting money aside to save counts as sending it to do the job called “savings.”

Q. Zero-based budgeting vs. the 50/30/20 rule — which is better?

Neither is objectively correct. Zero-based budgeting allocates every dollar until the balance hits zero, so it’s precise but hands-on. The 50/30/20 rule splits income into three broad percentages, so it’s simple and loose. Choose ZBB for fine control, 50/30/20 for a low-effort frame.

Q. Can I use zero-based budgeting with irregular income?

Yes, but it’s harder. Two fixes help: budget based on your lowest expected income for the month, or put money you receive now into next month’s budget so you’re always living a month ahead.

Q. How do I start building a zero-based budget?

Follow five steps: add up expected net income, allocate fixed costs, allocate variable costs, allocate financial goals (emergency fund, savings, investing), then adjust until the balance hits zero. The key is starting from a blank page each cycle rather than copying last month.

Q. My budget keeps collapsing — what am I doing wrong?

Usually it’s built too tight. Keep a “buffer” or reserve category for surprises like car repairs and medical bills, and give “fun” a real, non-zero allocation. A budget with room to breathe is the one that lasts.