How Inflation Quietly Erodes the Value of Your Savings

1. The Number Stays the Same — So Why Are You Poorer?

A few years back I pulled up an old account where I’d parked some emergency cash. The number hadn’t dropped a single cent. And yet, when I tried to buy the things I used to buy with it, the money came up short. The figure was unchanged, but the amount it could buy had shrunk.

This calls for a shift in perspective. We usually learn that inflation is “prices going up.” Not wrong, exactly, but the sharper way to see it is this: inflation is your money losing purchasing power. Bread didn’t get more valuable — your dollars lost some of their power to buy bread.

- Nominal value: the number printed on your statement. This stays put.

- Real value (purchasing power): what that money can actually buy. This quietly shrinks.

That’s why inflation gets called a silent tax. No bill arrives, nobody visibly takes a cut, and yet the value of idle money slips away a little every year.

2. The Rule of 72: How Long Until Your Money Is Cut in Half

So how fast does it erode? There’s a wonderfully simple tool for this: the Rule of 72.

72 ÷ inflation rate (%) ≈ the number of years for purchasing power to halve

I checked it against the exact (logarithmic) values myself, and across the low-to-mid range it holds up impressively well.

| Inflation rate | Rule of 72 | Exact (log) |

|---|---|---|

| 2% | 36 yrs | 35.0 yrs |

| 3% | 24 yrs | 23.4 yrs |

| 5% | 14.4 yrs | 14.2 yrs |

| 7% | 10.3 yrs | 10.2 yrs |

| 10% | 7.2 yrs | 7.3 yrs |

In plain terms: with prices rising just 3% a year, your money’s purchasing power is cut in half in about 24 years. For a touch more precision people also use the “Rule of 70” — at 3%, 70÷3 = 23.3 years, even closer to the exact 23.4.

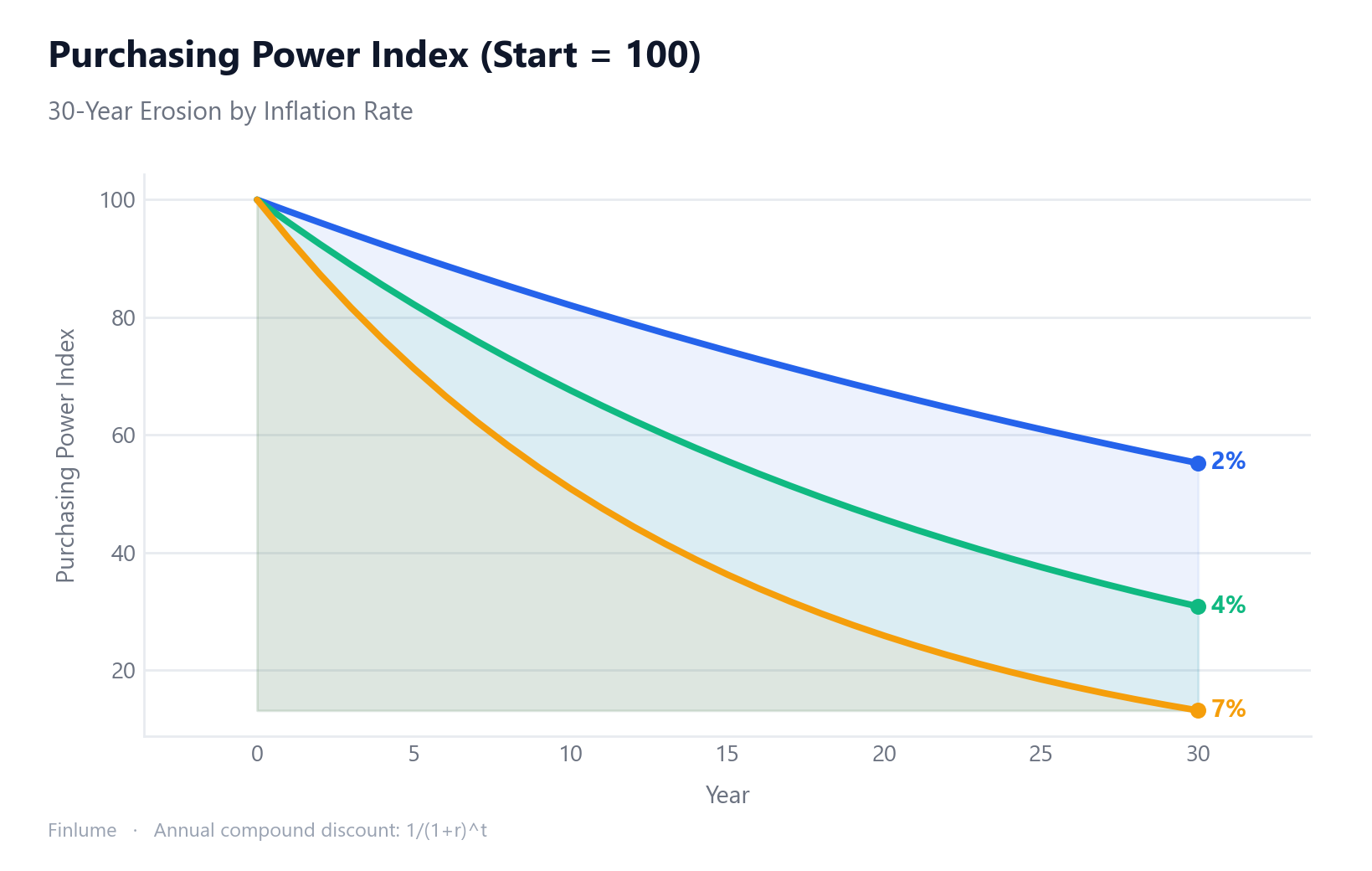

3. Inflation Compounds — Losses Accelerate Over Time

Here’s the part many people miss. Inflation works as compounding, not simple, erosion. Each year it bites into what’s left, so the longer the horizon, the faster the damage piles up. It’s the exact mirror image of how compounding explodes when it’s growing your money — see why compound interest takes decades to pay off to make the structure click.

At 3% inflation, here’s what 100 today is really worth down the road.

| Time elapsed | Real value of 100 today |

|---|---|

| After 1 year | 97.09 |

| After 5 years | 86.26 |

| After 10 years | 74.41 |

| After 20 years | 55.37 |

| After 30 years | 41.20 |

After 30 years, only about 41% of the original purchasing power survives. More than half — 59% — has evaporated. It drips away slowly at first, then the curve steepens. That acceleration is the signature of compounding.

4. “But I’m Earning Interest — How Am I Losing?”

“Sure, but if I park it in a deposit account I earn interest.” True. The thing to measure, though, isn’t the nominal rate — it’s the real return.

The precise calculation uses the Fisher equation.

real return = (1 + nominal rate) ÷ (1 + inflation rate) − 1 quick approximation ≈ nominal rate − inflation rate

A couple of worked examples:

- Savings interest of 2% vs inflation of 5% → real return −2.86% (approx −3%). Even with interest, your purchasing power drops roughly 3% a year.

- Savings interest of 0.5% vs inflation of 4% → real return −3.37%. You collect interest and still lose ground.

When the nominal rate is below the inflation rate, the real return goes negative. That’s a negative real interest rate. “It’s safe because it’s a deposit” only means the number is safe — the purchasing power can shrink while you sit still. Fees gnaw at your returns just as quietly as inflation does; why a 1% fee quietly costs you half your retirement shows how closely the two resemble each other.

5. Small Gaps, Big Differences — The Power of 1–2 Points

A small change in the inflation rate produces a wildly different long-run result, because the effect is non-linear. Suppose you let $10,000 sit for 30 years with no interest at all.

| Inflation rate | Real value after 30 yrs | Purchasing power lost |

|---|---|---|

| 3% | $4,120 | $5,880 (about 59%) |

| 5% | $2,314 | $7,686 (about 77%) |

Bumping inflation up by just two percentage points pushes the loss from 59% to 77%. “Only a few percent” turns out to be anything but, once decades are involved.

5b. The Real-Return Lookup: Is Your Deposit Rate Actually Keeping Up?

The article’s Section 4 showed two Fisher-equation examples. But one or two examples are easy to dismiss. What if you looked at every realistic combination at once?

The table below shows exact real returns (Fisher equation, not the approximation) for five typical deposit rates against five inflation scenarios. Every cell marked negative means your purchasing power is shrinking even while the interest credits arrive.

| Deposit rate \ Inflation | 2% | 3% | 4% | 5% | 6% |

|---|---|---|---|---|---|

| 0.5% | −1.47% | −2.43% | −3.37% | −4.29% | −5.19% |

| 1.0% | −0.98% | −1.94% | −2.88% | −3.81% | −4.72% |

| 2.0% | 0.00% | −0.97% | −1.92% | −2.86% | −3.77% |

| 3.0% | +0.98% | 0.00% | −0.96% | −1.90% | −2.83% |

| 4.0% | +1.96% | +0.97% | 0.00% | −0.95% | −1.89% |

Assumption: Fisher equation, (1 + deposit rate) ÷ (1 + inflation rate) − 1. Diagonal cells (bold 0.00%) are the break-even points where deposit rate equals inflation rate exactly.

19 out of 25 combinations produce a negative real return. The only positive-real-return cells require either low inflation (2–3%) combined with a deposit rate that exceeds it, or an unusually high deposit rate. Most everyday savings accounts sit in the 0.5–2% row — and nearly every cell in those rows is red territory.

To put a negative real return in concrete terms: a real return of −2.88% (e.g., 1% deposit rate vs. 4% inflation) leaves only 74.6% of original purchasing power after 10 years and 55.7% after 20 years — almost the same damage as holding zero-interest cash at 3% inflation. The interest barely registers against the inflation headwind.

6. So How Should You Think About It?

Let me be clear on a few things. The 2%, 3%, and 5% figures above are illustrative examples to explain the principle. Real inflation varies by era and region — there are low-inflation stretches and high-inflation ones. Low today does not mean low forever.

And being wary of inflation doesn’t make all cash bad.

- Short-term money (emergency fund, anything you’ll spend within 1–2 years): keeping it in cash or deposits is sensible. Here, liquidity and stability matter far more than inflation drag. For how much to hold and how to build it, see emergency fund 101: how much you need and how to build it fast.

- Cash left idle for the long haul: this is where inflation risk genuinely bites. If it’s money you’ll leave untouched for 10 or 20 years, look at it through the purchasing-power lens. If you’re weighing assets that aim to hold real value, why every portfolio needs bonds is a good starting point.

Key Takeaways

- See inflation not as rising prices but as falling purchasing power.

- 72 ÷ inflation rate = years until your money halves (about 24 at 3%).

- Inflation compounds, so losses accelerate over time (59% gone at 3% over 30 years).

- If the nominal rate is below inflation, your real return is negative.

- A 1–2 point difference in inflation creates a huge long-run gap (non-linear).

- Cash makes sense for short-term money; long-idle cash is the real risk.

- Across realistic deposit/inflation combinations, 19 of 25 produce a negative real return — interest income alone rarely offsets inflation.

This isn’t a pitch for any particular product. But building one habit — judging money by purchasing power, not the printed number; by real returns, not nominal ones — is enough to keep the silent tax from quietly winning. That perspective is the most valuable thing to walk away with today.

🧮 See it with your numbers: Enter an amount and inflation rate into the inflation calculator to see how much purchasing power you lose over time.

FAQ

Q. How exactly does inflation erode the value of my savings? The number on your statement (the nominal value) stays the same, but the amount that money can buy (its purchasing power) shrinks. Bread didn’t get more valuable — your dollars lost some power to buy it. Because no bill ever arrives, this loss is called a silent tax.

Q. How long does it take inflation to cut my money in half? Use the Rule of 72: 72 divided by the inflation rate (%) gives the years for purchasing power to halve. At 3% annual inflation, for example, your money’s purchasing power is cut in half in about 24 years.

Q. Can I lose money even while earning interest on a deposit? Yes. What matters is the real return, not the nominal rate. When the nominal rate is below the inflation rate, your real return turns negative — a negative real interest rate. You collect interest and still lose purchasing power each year.

Q. So is holding cash always a bad idea? No. For an emergency fund or any money you’ll spend within 1–2 years, cash and deposits are sensible, because liquidity and stability matter more than inflation drag. The real risk is cash left idle for 10 or 20 years.

Q. Does a 1–2 percentage point difference in inflation really matter that much? Over long horizons, yes, because the effect is non-linear. Left untouched for 30 years with no interest, about 59% of purchasing power vanishes at 3% but about 77% vanishes at 5%. Two points create a huge gap over decades.