What Savings Rate Should You Actually Aim For?

When I first started tracking my money, the first thing I’d look at was “how much is left this month?” Took me years to realize that exact mindset is why nothing was piling up.

Start Here: Not “How Much,” But “How Many Days of Your Paycheck”

If you treat savings as “whatever’s left after spending,” you’ll save nothing. Leftover money almost always rounds to zero. So flip the order: when your paycheck lands, set money aside first, then live on the rest. People call this “pay yourself first.”

But “save 20%” never really landed for me. So I converted it into days. If a month is 30 days, a savings rate of X% means setting aside (30 × X/100) days of your paycheck every month.

| Savings rate | Days of pay |

|---|---|

| 10% | 3 days |

| 20% | 6 days |

| 30% | 9 days |

| 50% | 15 days |

In working-day terms (about 21.7 workdays a month), 20% is roughly 4.3 workdays. In other words: “about one day a month, you work for future-you.” Suddenly 20% doesn’t sound so brutal, does it?

The Most Common Benchmark: 20% (the 50/30/20 Rule)

The first number that shows up in any savings conversation is the 50/30/20 rule: split your after-tax income into 50% needs, 30% wants, and 20% savings and debt repayment.

This rule was popularized by Elizabeth Warren and Amelia Warren Tyagi in All Your Worth: The Ultimate Lifetime Money Plan (2005). It’s simple, it sticks, and that’s why it’s the most-cited starting point. For how to actually split those buckets and run them, see how to split your paycheck with the 50/30/20 budget rule.

But don’t misread it. 20% is a minimum starting line, not the answer. It’s a benchmark you adjust up or down based on income, cost of living, goals, and age—not a finish line you cross once and forget.

Thinking About Retirement: Around 15% of Income

Retirement might feel far off, but it pays to know the number early. The common guideline from Fidelity and other asset managers is to save about 15% of income for retirement (employer match included), assuming you start early—say, your mid-twenties.

The key word is “early.” The later you start, the steeper the required rate climbs, because you’ve robbed compounding of its working hours. When you start matters as much as how much you save. I learned that one the slow way.

Before Any of That: 3–6 Months of Emergency Fund

Honestly, there’s a priority above everything above: the emergency fund. Pour everything into investments to juice your savings rate, then hit a sudden big expense, and you’ll end up borrowing or selling at a loss. Been there.

The standard advice is to hold 3–6 months of living expenses (based on needs) in cash-like assets. If your income is unstable or you’re a single earner, stretch it past 6 months. For sizing the target and building it fast, see how much emergency fund you need and how to build it. Lay this safety net before you optimize anything else.

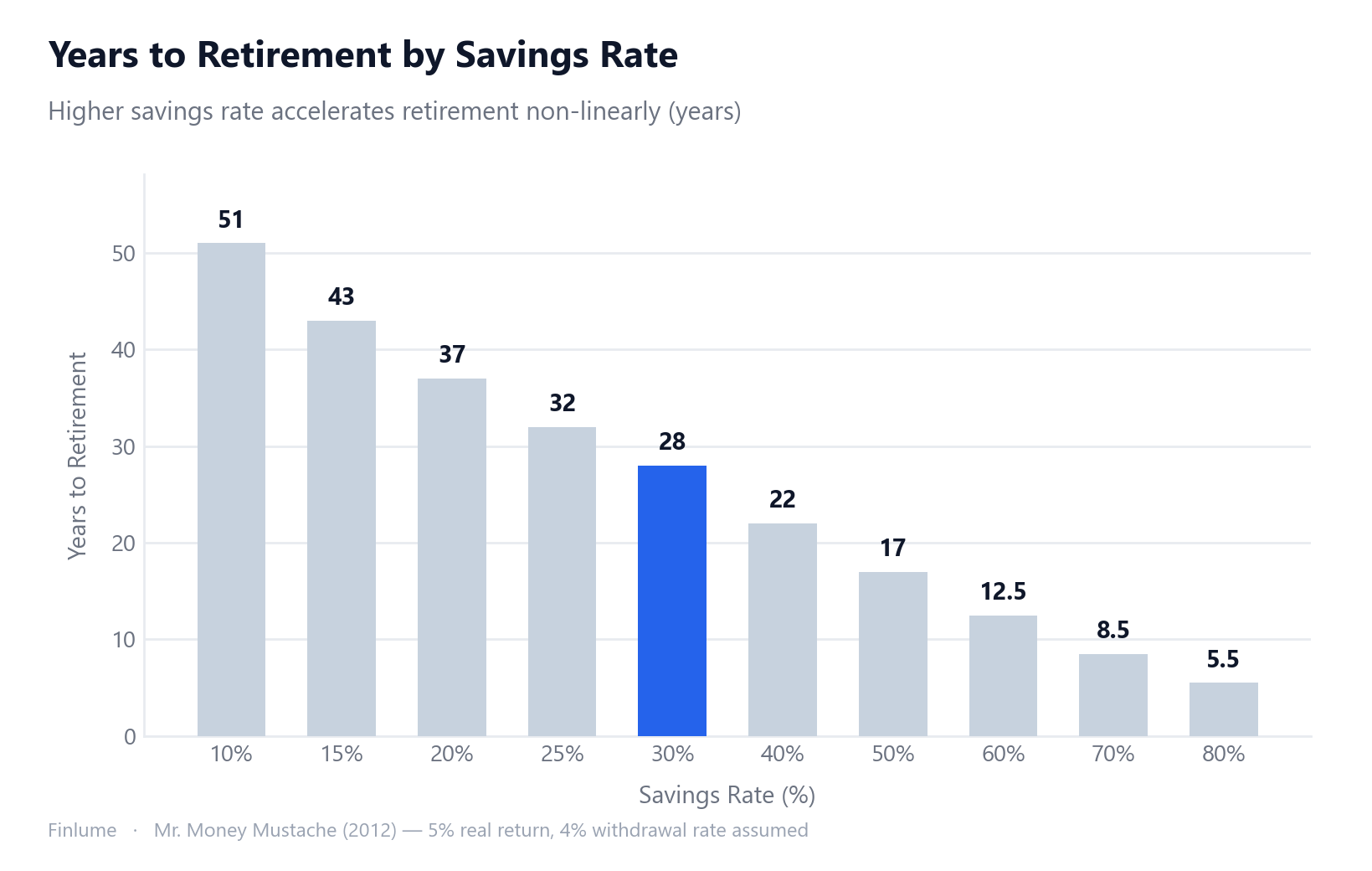

What Your Savings Rate Really Buys: Time

This is the part I most want you to see. Your savings rate isn’t just “how much you accumulate”—it decides when you can stop working.

| Savings rate | Years to retirement |

|---|---|

| 10% | ~51 years |

| 15% | ~43 years |

| 20% | ~37 years |

| 25% | ~32 years |

| 30% | ~28 years |

| 40% | ~22 years |

| 50% | ~17 years |

| 60% | ~12.5 years |

| 70% | ~8.5 years |

| 80% | ~5.5 years |

This model was popularized in The Shockingly Simple Math Behind Early Retirement (Mr. Money Mustache, 2012). Assumptions: ~5% real return, a 4% withdrawal rate (25× your annual spending), starting from zero, on after-tax income. If the 4% rule and FIRE number math intrigue you, see how financial independence actually works.

See how the numbers collapse non-linearly? That’s the double effect of thinking in percentages. A higher savings rate means (1) you accumulate faster, and (2) since you spend less, the nest egg you need shrinks too. Bump your rate by just 10 points and you can shave off years—sometimes a decade or more.

One caveat. This is a simplified model. It ignores return volatility, taxes, inflation, and changing income. Treat it as a thinking tool that shows the power of your savings rate, not a precise forecast.

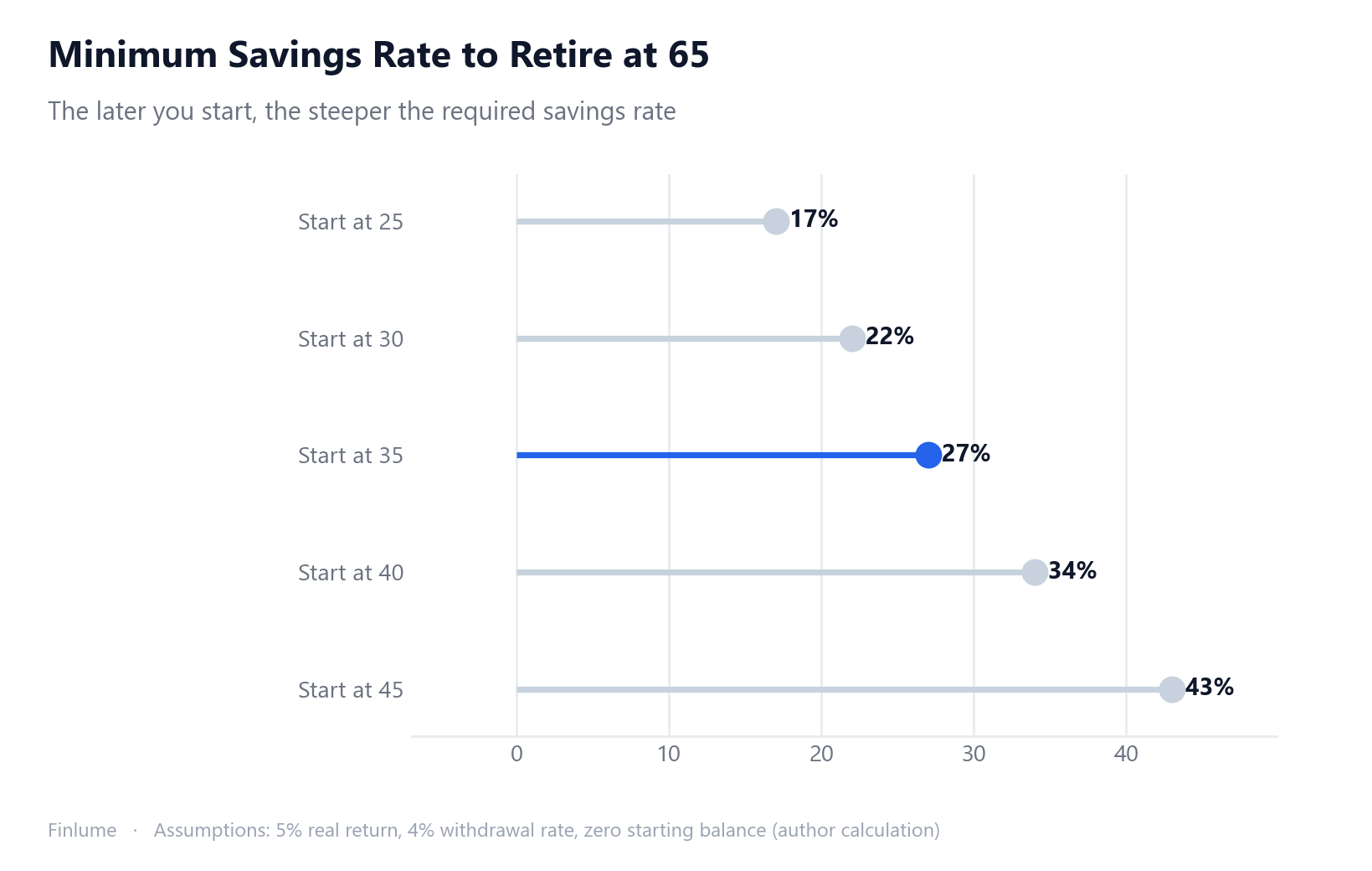

The Cost of Starting Late: A Catch-Up Rate Calculator

The years-to-retirement table above assumes you start today and run the math from zero. But most people ask a different question: “I’m already 35 (or 40). What savings rate do I actually need to retire at 65?”

The table below answers that directly. It shows the minimum savings rate required to reach financial independence by age 65, depending on your starting age — assuming a 5% real annual return, a 4% withdrawal rate (the standard 25× spending target), and zero existing savings. If you already have savings, your required rate is lower.

| Start Age | Years to Invest | Min Savings Rate Needed |

|---|---|---|

| 25 | 40 | 17% |

| 30 | 35 | 22% |

| 35 | 30 | 27% |

| 40 | 25 | 34% |

| 45 | 20 | 43% |

Assumptions: 5% real return, 4% withdrawal rate, zero starting balance. Source: author calculation.

Notice the acceleration: each 5-year delay costs roughly 5–9 extra percentage points. Waiting from 25 to 35 turns a manageable 17% into 27%. Wait until 45 and you need 43% — nearly half your take-home pay. The lesson isn’t to panic; it’s to act now rather than wait for a “better” time, and to accept that a late start means a higher rate, not a hopeless situation.

Two practical notes: (1) Any savings you already have reduces your required rate — use this table as a ceiling, not a fixed number. (2) If 34% feels impossible at 40, a part-time income, a later target retirement age, or a leaner spending target can all bring the required rate back down.

A Step-by-Step Roadmap for Your Own Rate

In practice, climb these steps in order:

- Step 0: Lock in 3–6 months of emergency fund first.

- Step 1 (starting line): 20% of your paycheck (6 days) = 50/30/20.

- Step 2 (standard): Automate at least 15%, retirement included.

- Step 3 (accelerate): When income rises, freeze your lifestyle and route a big chunk of the raise into savings → push toward a 30–50% rate.

Step 3 is all about fighting lifestyle creep—the habit of spending more the moment you earn more. Upgrade your car the day your raise clears, and your savings rate stays flat forever.

And the caveat that overrides everything: paying off high-interest debt beats any savings. Investing for a hoped-for 5% while paying 15% interest is just pouring water into a leaky bucket. To decide which debts to attack first, see good debt vs. bad debt: 4 ways to tell them apart.

Closing: The Answer Isn’t a Percentage—It’s “Set Aside First, Then Automate”

OECD household net saving rates run the gamut, from negative to double digits depending on the country. Which means the average can’t be your benchmark. You set your rate against your goals.

The checklist:

- Saving is “setting aside first,” not “keeping what’s left” (pay yourself first)

- Priority zero is a 3–6 month emergency fund, then high-interest debt

- Starting line 20% (6 days); automate 15%+ including retirement

- A 10-point difference in savings rate can move your retirement date by years

- The key to success is automation, not willpower

- Every 5-year delay in starting raises the required savings rate by 5–9 percentage points (17% at 25 → 27% at 35 → 43% at 45)

Today, set aside even one day’s worth of your paycheck and put it on autopilot. Future-you will thank you for it more than almost any other decision.

FAQ

What savings rate should I start with?

The 20% from the 50/30/20 rule is the most widely used starting line. But it’s a minimum starting point, not the answer—adjust it up or down based on your income, cost of living, goals, and age.

How much should I save for retirement?

The common guideline from Fidelity and other asset managers is to save about 15% of income for retirement (employer match included), assuming you start early—say, your mid-twenties. The later you start, the steeper the required rate climbs.

Should I build an emergency fund or save first?

The emergency fund comes first. Hold 3–6 months of living expenses (based on needs) in cash-like assets before pushing your savings rate higher. If your income is unstable or you’re a single earner, stretch it past 6 months.

How much faster can a higher savings rate make me retire?

In the Mr. Money Mustache (2012) model (5% real return, 4% withdrawal rate), a 10% savings rate takes about 51 years while 50% takes about 17. Bumping your rate by just 10 points can shave off years—a non-linear effect. It’s a thinking tool, not a precise forecast.

Should I invest or pay off debt first?

Paying off high-interest debt beats any savings or investing. Chasing a hoped-for 5% return while paying 15% interest is just pouring water into a leaky bucket.