Net Worth 101: How to Calculate It, Track It, and Actually Grow It

Ask someone their salary and they’ll answer instantly. Ask “what’s your net worth?” and you usually get a blank stare. I was the same. I knew my paycheck down to the cent, but I’d never once put a number on my actual financial position. Let’s fix that today and learn how to calculate your net worth and track it over time.

1. What Is Net Worth? The Real Health Metric (Not Income)

The formula is almost embarrassingly simple.

Net worth = total assets − total liabilities

More assets than debt means a positive net worth; more debt than assets means a negative one. The key idea is that net worth is a snapshot at a single point in time — one financial photo of where you stand today.

This is where a lot of people trip up on income. Income is a flow, like water running through a pipe, not a stockpile of assets. So you never put your salary into the net worth calculation. You can earn a fortune and have a net worth of zero if it all goes out the door, while a modest earner who saves steadily can build a far bigger number. That’s exactly why net worth is a more complete health metric than income alone.

2. Sort Every Asset and Liability — Miss Nothing

Start by listing assets in six buckets so nothing slips through.

| Category | Examples |

|---|---|

| Cash & equivalents | Checking, savings, money market funds, deposits |

| Investments | Stocks, bonds, funds, retirement/pension accounts |

| Real estate | Primary home, rental/investment property |

| Vehicles | Car, motorcycle, boat |

| Personal property | Jewelry, art, collectibles, furniture |

| Business equity | Ownership stake, if any |

Things you can convert to cash fast are liquid assets; things like real estate that take time to sell are illiquid.

Liabilities are simpler. They’re every dollar you owe: mortgage, auto loan, student loans, credit card balances, personal loans, medical debt — every unpaid obligation goes on the list.

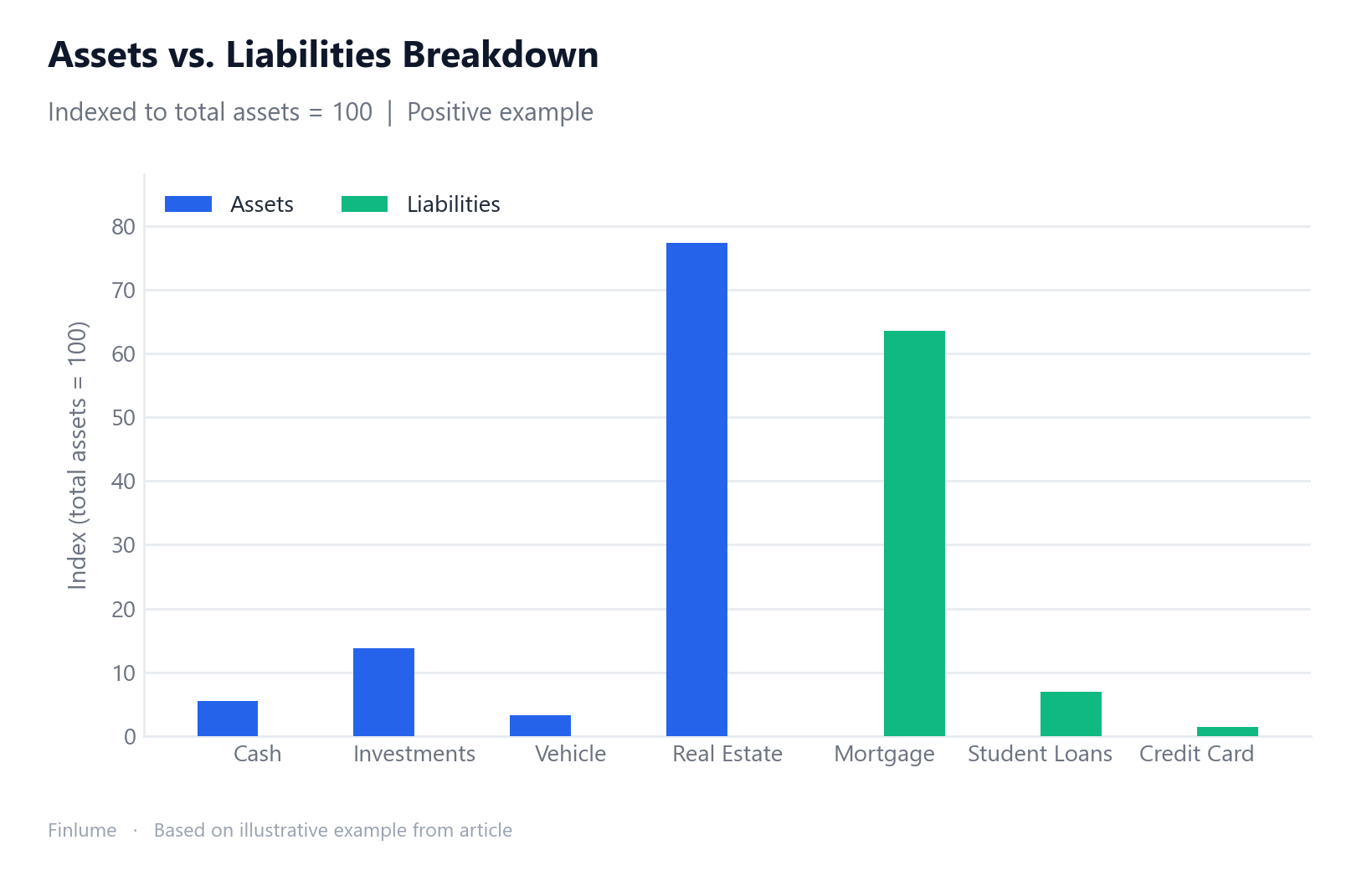

3. The 3-Step Calculation, With Real Examples

Just three steps.

- Add up the current market value of every asset

- Add up the current balance of every liability

- Assets − liabilities = net worth

Positive example: Assets = $20,000 cash + $50,000 investments + $12,000 vehicle (market value) + $280,000 home = $362,000. Liabilities = $230,000 mortgage + $25,000 student loans + $5,000 credit card = $260,000. → Net worth = $102,000.

Negative example: Assets = $3,000 cash + $8,000 vehicle = $11,000. Liabilities = $35,000 student loans + $4,000 credit card = $39,000. → Net worth = −$28,000.

Don’t panic if yours comes out negative. It’s incredibly common early in life.

4. Liquid vs. Total Net Worth, and Valuing Depreciating Assets

Total net worth is all assets minus all liabilities. But the money you could actually reach in an emergency is a different question — that’s your liquid net worth. You count only assets you can convert to cash quickly, and you exclude or discount real estate, retirement accounts, and vehicles.

In practice, apply roughly a 10–20% discount to account for illiquidity and selling costs. For real estate, shave off about 6–10% (some sources say 10–30%) for agent commissions and closing costs. If your total net worth looks great but it’s all locked up in a house and a pension, your liquid net worth may be surprisingly thin — and liquid net worth is what shows your real readiness for a crisis.

Then there’s depreciation. A car can lose about 20–30% of its value in the first year alone, and it keeps sliding after that. Electronics and furniture do the same. So always record assets at current market value, not purchase price. List a five-year-old car at what you paid, and your net worth becomes pure fiction.

4a. The Illiquidity Gap: Why Two People With the Same Net Worth Are Not in the Same Position

The article above noted that real estate gets an 8% haircut and illiquid assets (vehicles, locked pensions) get a 15% haircut when computing liquid net worth. But how much does that actually matter in practice? The answer depends almost entirely on what your net worth is made of.

The table below indexes every figure to total net worth = 100 (multiply by your real net worth to get actual amounts). Assumptions: real estate discount 8% (midpoint of 6–10%), illiquid-asset discount 15% (midpoint of 10–20%), cash and investments 0% (fully liquid).

| Profile | Cash & investments | Real estate | Illiquid assets | Total NW | Liquid NW | Gap |

|---|---|---|---|---|---|---|

| Renter / cash saver | 85% | 0% | 15% | 100 | 97.5 | 2.5 (2%) |

| New grad (recovering) | 22% | 0% | 78% | 100 | 86.5 | 13.5 (13%) |

| Balanced homeowner | 20% | 60% | 20% | 100 | 78.2 | 21.8 (22%) |

| Property-rich / cash-poor | 8% | 80% | 12% | 100 | 71.3 | 28.7 (29%) |

Two people can both show a total net worth of 100 on paper. One — the renter with cash savings — can actually access 97.5 of that in a crisis. The other — the homeowner with a large mortgage and thin cash reserves — can realistically access only 71.3. That is a 26-unit gap on identical headline figures. The bottom line: when you calculate your own net worth, run both numbers every time. Your total net worth tells you your overall financial score; your liquid net worth tells you whether you can survive next month’s emergency without selling your house.

5. How Often Should You Track? Monthly vs. Quarterly vs. Annual

The honest answer: whatever fits your situation.

| Frequency | Best for |

|---|---|

| Monthly | Actively paying down debt or saving hard; wants to catch trends early |

| Quarterly | Heavy in investments; wants to filter out short-term market noise |

| Annual | Simple finances or just checking the long-term trend (do this at least once a year) |

More important than the frequency itself is consistency. Pick a schedule, stick to it, and use the same valuation method every time. Measure erratically and the trend disappears in the noise.

6. The 6 Calculation Mistakes People Make

- Overvaluing assets — using purchase price or sentimental value (homes and cars especially)

- Missing debts or using old balances — that “paid off” balance sometimes isn’t

- Padding with small personal items — clothes and small furniture inflate the total

- Mistaking income for assets — salary is a flow; it never belongs here

- Inconsistent valuation — market value this time, purchase price next time… trust gone

- Ignoring liquidity — most of your assets may not be reachable on short notice

7. Negative Net Worth Is Normal — 6 Ways to Grow It

Let me say it again clearly: a negative net worth for new grads and people early in their careers is extremely common and is not a sign of failure. You’ve got student loans and you simply haven’t had time to accumulate assets yet. What matters is the direction.

- Pay off high-interest debt first — start with credit cards and similar (it helps to first tell good debt from bad debt, then pick a payoff order with the snowball vs. avalanche method)

- Build an emergency fund — typically 3–6 months of living expenses (see how much you actually need)

- Grow your income — strengthen your earning power

- Invest consistently — compounding lets time do the work

- Spend less than you earn — in the end, this is the whole game (setting a savings rate you can actually hit makes it concrete)

- Track regularly — you act on numbers you actually see

One note: your emergency fund is part of your liquid net worth and counts toward total net worth, but its purpose is financial safety, not wealth accumulation. Don’t confuse the two.

🧮 Calculate yours: Enter your assets and debts into the net worth calculator to get your number in seconds.

FAQ

How do I calculate my net worth? Subtract your total liabilities from your total assets (net worth = total assets − total liabilities). Add up every asset at current market value, add up the current balance of every debt, and the difference is your net worth at that point in time.

Does my income or salary count toward net worth? No. Income is a flow, not a stockpile of assets, so you never put your salary into the calculation. You can earn a high income and still have a net worth of zero if it all goes back out the door.

Is it OK to have a negative net worth? Yes — it’s very common. For new grads and people early in their careers who have student loans and haven’t had time to accumulate assets, a negative net worth is not a sign of failure. What matters is the direction, and you start by cutting high-interest debt.

How often should I check my net worth? Pick monthly, quarterly, or annual based on your situation, but do it at least once a year. Consistency — using the same valuation method every time — matters more than the frequency itself.

What’s the difference between liquid and total net worth? Total net worth is all assets minus all liabilities; liquid net worth counts only the assets you can convert to cash quickly. You discount illiquid assets by about 10–20% and real estate by about 6–10%, and liquid net worth is what shows your real readiness for an emergency.

Key Takeaways

- Net worth = total assets − total liabilities, a single-point snapshot

- Income is a flow; keep it out of the calculation

- Always use current market value (cars lose 20–30% in year one)

- For liquid net worth, discount illiquid assets 10–20%, real estate 6–10%

- Consistency beats frequency — same method every time

- Negative net worth is common — start by cutting high-interest debt

- Same total NW, very different reality: a property-heavy portfolio can leave liquid NW 29% below the headline number

Thirty minutes today is enough to log your first number. And if you don’t love that number, that’s fine. Just knowing your starting point already gets you halfway there. Let’s grow it together.