How to Set SMART Financial Goals

Every January I used to promise myself I’d “save more money this year,” then stare at my account in December and sigh. Sound familiar? Here’s the blunt takeaway up front: vague goals almost always fail. A resolution with no number, no deadline, and no one responsible isn’t a goal, it’s a mood. In this article we’ll put a skeleton under your goals using the SMART framework, look at what behavioral research says about writing them down and sharing them, and run the real numbers on how small automatic savings compound. There’s a copy-and-go checklist at the end.

1. Why “Just Save More” Always Fails

The problem with “save more money” is that nobody knows what success looks like, how much, by when, starting how. If you can’t measure it, you can’t check it, and if you can’t check it, it quietly fizzles out.

The SMART idea first appeared in 1981, when George T. Doran published a piece in Management Review (Vol. 70, Issue 11). He was a corporate planning man at a power company, and he proposed five letters to help managers actually write usable objectives. Here’s the part people forget: Doran himself wrote that not every goal has to meet all five criteria. It was meant as a practical guideline, not a rigid formula.

2. The Five Letters, Applied to Money

Doran’s original letters were S (Specific), M (Measurable), A (Assignable, as in someone owns it), R (Realistic), and T (Time-related). The version most common in personal finance today swaps a few words: A = Achievable, R = Relevant, T = Time-bound. Different words, same spirit.

Watch what happens when you SMART-ify the same wish:

| Vague goal | SMART goal |

|---|---|

| Save more money | Build a $6,000 emergency fund in 12 months = $500/month |

| Do some saving | Save $5,000 within 12 months = about $417/month |

| Money for a house | $25,000 down payment over 5 years (60 months) = about $417/month |

$6,000 ÷ 12 = $500. $5,000 ÷ 12 ≈ $417. $25,000 ÷ 60 ≈ $417. The moment you divide a goal by its timeline, a fuzzy wish turns into “what I do this month.” That’s the core magic of SMART. If you’re not sure what that monthly number should be, start with what savings rate to aim for or use the 50/30/20 budget rule to free up the cash.

3. Measurement, Deadlines, and Accountability Change Outcomes

You’ll often see a “Yale/Harvard graduate goals study” cited here. Skip it, it’s an urban myth that never actually happened.

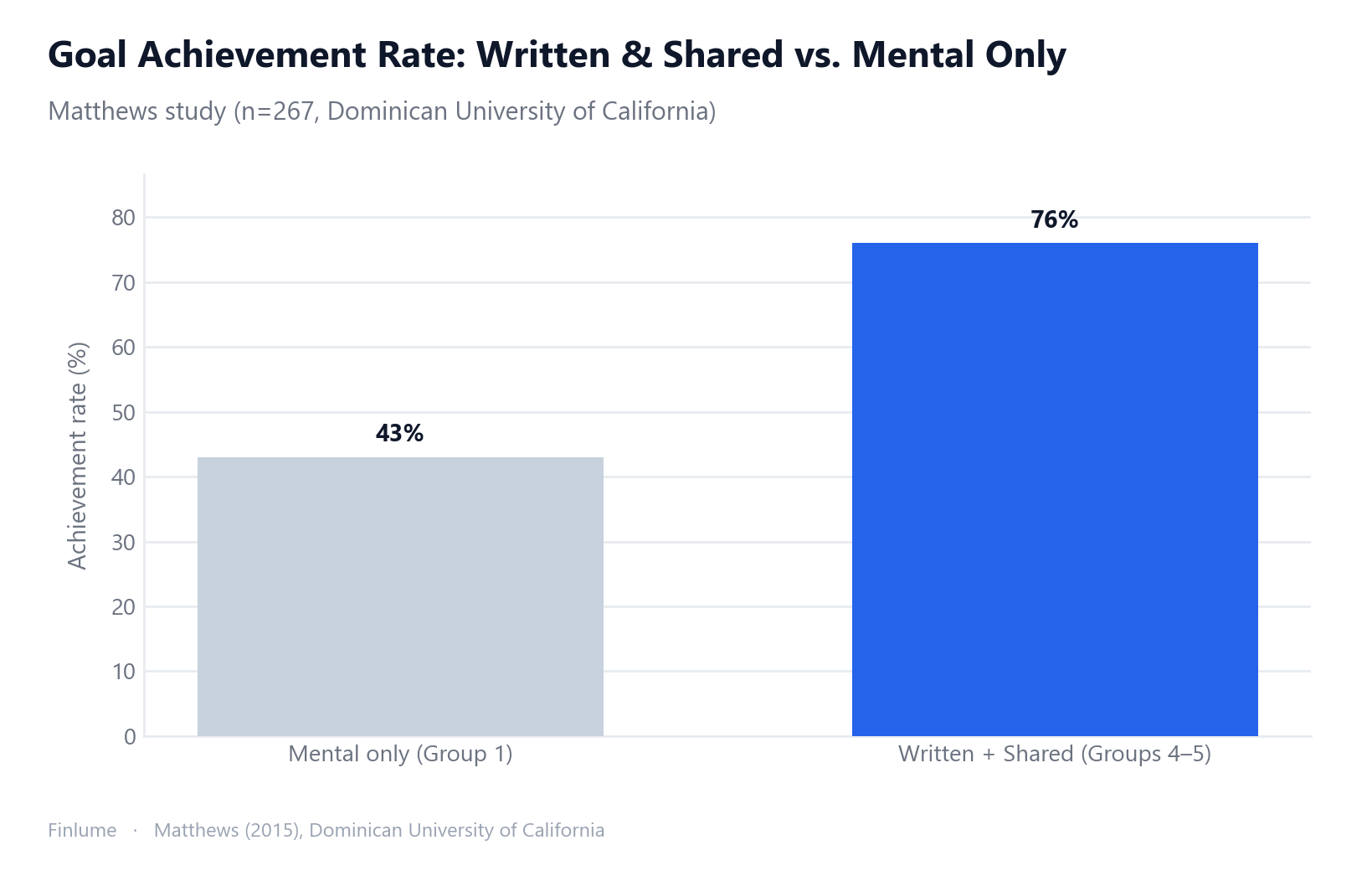

Here’s a real one instead. Dr. Gail Matthews of Dominican University of California split 267 participants (ages 23 to 72) into five groups. Group 1 only thought about their goals. Group 4 wrote them down, committed to action, and shared them with a friend. Group 5 added weekly progress reports on top of that. The result was clear: people who wrote their goals down and shared them regularly hit a far higher success rate (about 76%) than those who just kept them in their heads (about 43%).

The lesson is simple. SMART’s M (measurable) and T (time-bound) make tracking possible, and tracking creates accountability. Write it down, tell someone, and check in on a schedule.

4. The Compounding Power of Small Automatic Savings

“What’s $300 a month going to do?” is an easy thought to have. So I ran the numbers myself.

Assumptions: 7% annual return (an educational long-run stock-market average), $300 invested monthly, for 30 years (360 months).

| Item | Amount |

|---|---|

| Actual money you put in | $108,000 |

| Future value after 30 years | about $365,991 |

| Growth from compounding | about $257,991 |

The formula is FV = PMT x [((1+r)^n - 1) / r], with r = 0.07/12 and n = 360. You contribute roughly a hundred grand, and time does the rest of the work to push it past $365,000. Small, specific, automated savings end up making the biggest difference. Always pair a SMART goal with an automatic transfer. (Note: 7% is an assumption, not a guaranteed return.)

5. Sorting Goals into Short, Medium, and Long Term

Goals get easier to manage once you split them by horizon.

- Short term (under 1 year): The classic example is an emergency fund. Nearly every financial institution recommends 3 to 6 months of living expenses. Single-income households, dependents, or shaky job security often call for 6 months or more.

- Medium term (1 to 5 years): house down payment, replacing a car, funding a course or certification.

- Long term (5+ years): retirement, a child’s education, the big-picture stuff. If you’re thinking that far out, the basics of FIRE and financial independence are worth a look.

Attach a separate SMART number to each layer, and wire them all to automatic transfers. A system that doesn’t lean on willpower beats willpower every time.

6. The Limits of SMART, and How to Cover Them

SMART isn’t a cure-all. Critics point out that over-emphasizing “achievable” and “specific” can shrink bold, long-range vision. Chase only the goals within easy reach and you may quietly downsize your bigger dreams.

The fix: keep your big vision separate from SMART, then break the execution steps underneath it into SMART pieces. Also, rigid deadlines and figures drift out of sync when your income changes. Lock a quarterly or semi-annual review into your checklist so you actually revisit them.

7. Time-Bound, Quantified: What Your Deadline Actually Demands

A SMART goal is Measurable and Time-bound, and those two letters work together: the deadline is what turns the goal into a concrete monthly number. But the deadline does something less obvious too — it decides whether investing even helps. Take a goal of 10,000 units and watch how the required monthly amount shifts as the deadline moves.

| Goal deadline | Save only (0% return), monthly | Invest @7%/yr, monthly | Growth covers |

|---|---|---|---|

| Short — 1 year | 833 | 807 | ~3% |

| Short — 3 years | 278 | 250 | ~10% |

| Medium — 5 years | 167 | 140 | ~16% |

| Long — 10 years | 83 | 58 | ~31% |

(Assumptions: goal = 10,000 units; the “Invest” column assumes 7% p.a. compounded monthly; “Growth covers” is the share of the goal filled by compound growth rather than your own contributions. Illustrative, not guaranteed.)

For short deadlines, expected return barely moves the number — saving (833) and investing (807) are almost identical, and growth covers only about 3%. So short-term SMART goals belong in safe savings, not the market; chasing return over one to three years adds real risk for a rounding-error benefit.

For long deadlines, investing does the heavy lifting — at 10 years, compounding covers roughly 31% of the goal, cutting the required monthly contribution from 83 (saving) to 58 (investing). This is exactly why Section 5 sorts goals into short, medium, and long: the deadline, not preference, decides the vehicle. That makes the T (Time-bound) the most financially consequential letter in SMART.

8. Action Checklist + Disclaimer

Steps you can follow today:

- Write your goal in one sentence, with an amount and a deadline (e.g., “$6,000 in 12 months”).

- Divide by the timeline to get your monthly savings (6,000 ÷ 12 = 500).

- Set up an automatic transfer for that amount.

- Share the goal with a friend or family member.

- Check your progress weekly or monthly.

- Sort your goals into short, medium, and long term.

- Review everything each quarter or half-year.

- Match each goal to its deadline: short-term goals belong in safe savings, long-term goals in invested growth.

Even a small goal, once you write it down, divide it, automate it, and share it, becomes far more likely to happen. This year, let’s swap the December sigh for a December smile.

🧮 Put a number on it: Enter your goal and time frame into the savings goal calculator to see exactly how much to save each month.

Frequently Asked Questions

Q. What is a SMART financial goal? SMART is a goal-setting framework standing for Specific, Measurable, Achievable, Relevant, and Time-bound. George T. Doran first proposed it in Management Review in 1981. It turns a vague resolution into an actionable goal by attaching a number and a deadline to it.

Q. What is the first step to setting a SMART financial goal? Write the goal in one sentence with an amount and a deadline, such as “$6,000 in 12 months.” Then divide it by the timeline to get your monthly savings ($6,000 ÷ 12 = $500), and set up an automatic transfer for that amount.

Q. Does writing down and sharing your goals really improve success rates? In Dr. Gail Matthews’ study at Dominican University of California (267 participants), people who wrote their goals down and shared them regularly hit a success rate of about 76%, versus about 43% for those who only thought about them. Writing it down, telling someone, and checking in builds accountability.

Q. Is saving a small amount like $300 a month worth it? At a 7% annual return (an educational assumption), $300 saved monthly for 30 years grows from $108,000 in contributions to about $365,991. Small, specific, automated savings make the biggest difference through compounding. Note that 7% is an assumption, not a guaranteed return.

Q. How much should an emergency fund be? Nearly every financial institution recommends 3 to 6 months of living expenses. Single-income households, dependents, or shaky job security often call for 6 months or more. An emergency fund is the classic short-term SMART goal.

Note: This article is for educational purposes and is not investment or financial advice. Return examples (such as 7%) are assumptions and are not guaranteed.