FIRE Basics: How Financial Independence Actually Works (and the Math Behind It)

“At what age could I actually stop working?” Once you start asking that question seriously, you bump into the word FIRE. And then the numbers start flying — the 4% rule, the Rule of 25, savings rates. Let’s slow down and work through the math together, step by step.

1. What FIRE Actually Is — Not Early Retirement, but Freedom of Choice

FIRE stands for Financial Independence, Retire Early. It describes a state where the income from your assets — your investment returns — can cover your living expenses, so working for money is no longer a requirement.

Here’s the part people often miss when I talk this through with them. The heart of FIRE isn’t “retire.” It’s the freedom to choose. You can stop working, or you can keep going. If you love what you do, stay. If you don’t, walk away whenever you like. That optionality is the real prize.

The intellectual roots go back to the 1992 book Your Money or Your Life by Vicki Robin and Joe Dominguez. It went mainstream in the 2000s–2010s through blogs like Mr. Money Mustache.

2. Core Formula #1: The 4% Rule and the Safe Withdrawal Rate

The starting point for all FIRE math is the 4% rule (Safe Withdrawal Rate, or SWR).

William Bengen first published it in 1994, and the 1998 Trinity Study (three professors at Trinity University) validated and popularized it. The idea:

Withdraw 4% of your portfolio in the first year of retirement, then adjust that amount upward only for inflation each year, and the risk of running out of money over roughly 30 years is very low.

The assumptions are a stock/bond mix (say, 50–75% stocks) and a 30-year horizon. Across most historical scenarios using U.S. stock and bond data, it held up. How you set that stock/bond split is covered in the guide to asset allocation, and pushing for a higher withdrawal rate ties straight into why higher returns always come with higher risk.

There’s an interesting update worth knowing. Bengen himself now argues that with broader diversification across asset classes, the safe withdrawal rate is higher than 4%. In his recent work (A Richer Retirement, 2025) he puts it at around 4.7%. So think of 4% as a conservative floor, not a ceiling.

3. Core Formula #2: Find Your FIRE Number with the Rule of 25

Flip the 4% rule and you get the famous Rule of 25, since 1 ÷ 0.04 = 25.

FIRE number = annual living expenses × 25

Say your annual expenses are $40,000. Your target is $40,000 × 25 = $1,000,000. Check it the other way: $1,000,000 × 4% = $40,000. It ties out perfectly.

Choose a more conservative withdrawal rate and the multiple climbs.

| Withdrawal rate | Multiple needed | Target on $40,000/yr |

|---|---|---|

| 4.0% | 25× | $1,000,000 |

| 3.5% | ~28.6× | ~$1,143,000 |

| 3.0% | ~33× | ~$1,333,000 |

The trade-off is plain to see: more safety means more assets.

4. The Real Variable Is Your Savings Rate — the One Number That Sets Your Date

Here’s the most powerful insight in all of FIRE. What governs how long it takes you to retire isn’t your absolute income — it’s your savings rate (amount saved ÷ after-tax income).

Why? A high savings rate works twice. First, you accumulate faster. Second, because you spend less, your target number itself shrinks. That double effect is what makes the savings rate decisive. Not sure what rate to target? What savings rate should you actually aim for? walks through the common benchmarks.

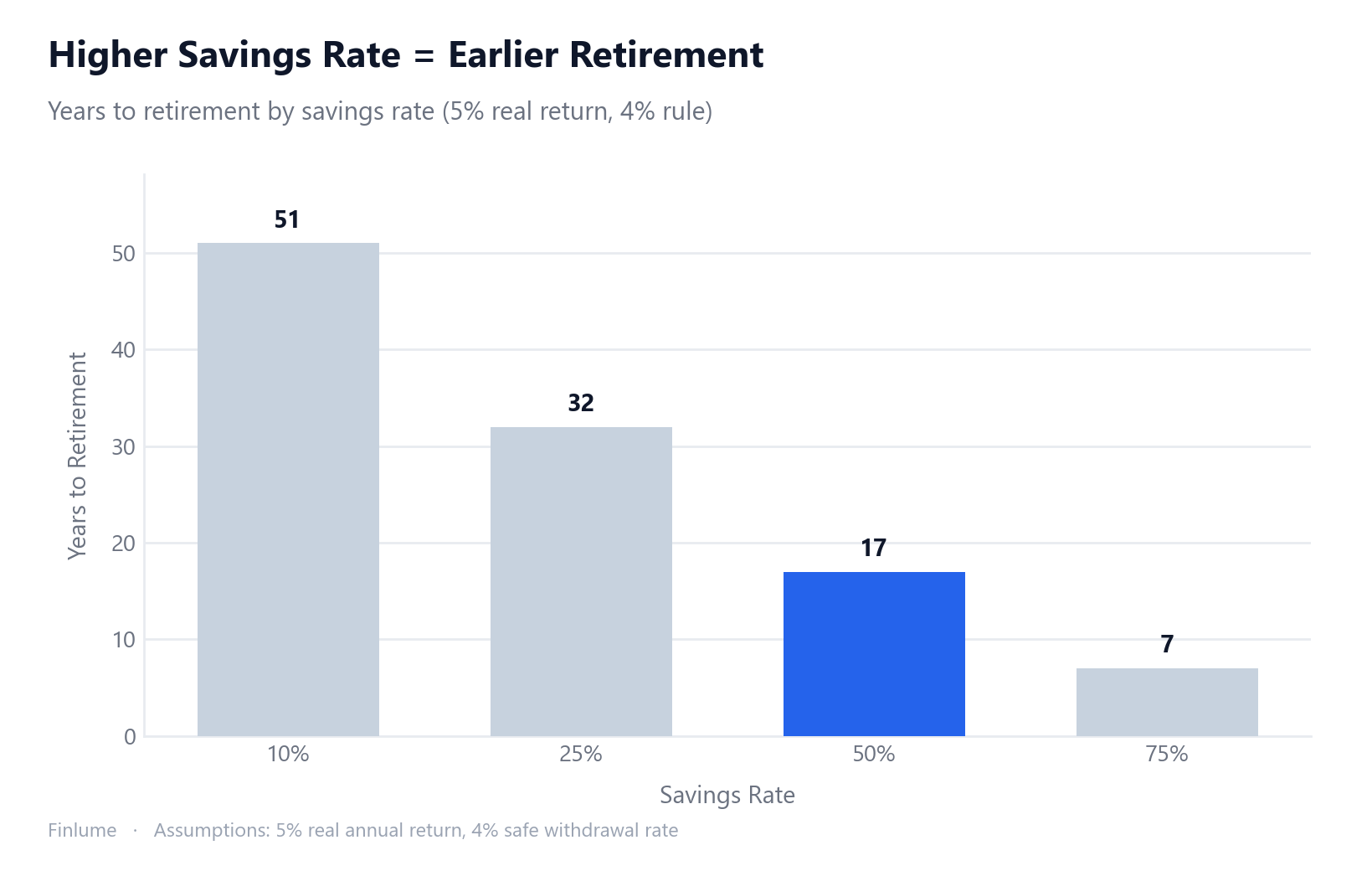

Here’s the widely cited table (assumptions: starting from zero, 5% real annual return, retire when you hit the 4% rule).

| Savings rate | Years to retirement |

|---|---|

| 10% | ~51 years |

| 25% | ~32 years |

| 50% | ~17 years |

| 75% | ~7 years |

The source is Mr. Money Mustache’s “The Shockingly Simple Math Behind Early Retirement,” reproducible with standard compound-interest math. The numbers shift with your return assumption. But notice: the gap between a 10% and a 50% savings rate is a staggering 34 years. Worth sitting with. The engine behind all of it is compounding — and why compound interest takes decades to pay off explains why the curve bends so sharply later on.

5. Which FIRE Fits You — Lean / Fat / Coast / Barista

FIRE isn’t one-size-fits-all. There are several lifestyle variants.

- Lean FIRE: Achieved on a minimal, frugal budget. Smaller target, but it demands tight spending control.

- Fat FIRE: Retire while maintaining a comfortable, generous lifestyle. The target number is large.

- Coast FIRE: Invest enough while you’re young, and compounding alone “coasts” you to your retirement target — no further saving needed. After that, you only need to cover current expenses.

- Barista FIRE: Not full retirement. You cover part of your income (and often benefits) with part-time or low-intensity work, keeping portfolio withdrawals to a minimum.

Pick the target that fits your spending habits and your relationship with work.

6. What Can Wreck Your FIRE — Sequence Risk and the Limits of the 4% Rule

This is the part to read carefully.

Sequence-of-returns risk: If the market drops sharply in the early years of retirement, your assets deplete much faster — even at the same average return. The first few years after you retire weigh heavily on long-term success.

Also, the 4% rule is built on a 30-year horizon. Early retirement can stretch to 40–50 years, so many argue you need a more conservative withdrawal rate (say, 3–3.5%).

Beyond that, inflation, medical and long-term care costs, market volatility, and unpredictable expenses don’t fit neatly into a simple model. That’s why a margin of safety (extra assets) and flexible withdrawals (spending less when markets are bad) matter so much.

Finally, every one of these calculations rests on historical data — it does not guarantee future returns. And the accuracy of your expense estimate is the foundation of everything. Underestimate your spending, and the whole target number is off.

7. Return Assumptions Matter — But Less Than You Think

The existing savings-rate table (Section 4) assumes a 5% real annual return. What happens if markets deliver more, or less? The table below computes years to FIRE across five savings rates and four real-return scenarios — all using the same 4% rule and zero starting balance (assumptions stated, figures computed with compound-interest math).

| Savings rate | 4% real return | 5% real return | 6% real return | 7% real return |

|---|---|---|---|---|

| 10% | 59 yrs | 51 yrs | 46 yrs | 42 yrs |

| 20% | 41 yrs | 37 yrs | 33 yrs | 31 yrs |

| 30% | 31 yrs | 28 yrs | 26 yrs | 24 yrs |

| 40% | 23 yrs | 22 yrs | 20 yrs | 19 yrs |

| 50% | 18 yrs | 17 yrs | 16 yrs | 15 yrs |

Assumptions: starting from zero, annual contributions made at year-end, 4% safe withdrawal rate, no taxes or fees modeled.

Two things stand out. First, the return assumption matters a great deal at low savings rates — the gap between 4% and 7% real returns at a 10% savings rate is 17 years. Second, and more importantly, that same gap shrinks to just 3 years at a 50% savings rate. In other words: the higher your savings rate, the less your retirement date depends on market performance. At 50% savings, a pessimistic market (4% real) only delays you 3 years versus an optimistic one (7% real). Your savings behavior, not the market, is the dominant variable. This is why most FIRE practitioners focus on controlling spending first and worry about return optimization second.

8. Wrap-Up: Your 3-Step FIRE Roadmap

- ① Calculate your living expenses: Pin down your actual annual spending as precisely as you can. It’s the starting point for all the math.

- ② Compute your FIRE number: Annual expenses × 25 (or 28–33× if you’re conservative) sets your target.

- ③ Set your savings rate and let compounding work: The higher your savings rate, the sooner the date arrives — and the less it matters whether markets deliver 4% or 7% real. Add a margin of safety and a flexible withdrawal plan.

The math is simpler than it looks — the hard part is walking toward the number, year after year. But even calculating your FIRE number once turns a vague “someday” into a concrete plan. Go slow if you have to. Just don’t stop.

🧮 See your numbers: Use the FIRE calculator for your target and timeline, and the retirement withdrawal calculator to see how long the money lasts.

FAQ

Q. How do I calculate my FIRE number? Multiply your annual living expenses by 25. That’s the Rule of 25, which is just the 4% rule flipped over. For example, if you spend $40,000 a year, your target is about $1,000,000. If you want to be more conservative, use a multiple of 28–33×.

Q. Is the 4% rule safe? On historical data assuming a 30-year retirement, the risk of running out of money was very low in most scenarios. But for early retirement, where the horizon can stretch to 40–50 years, many argue for a more conservative withdrawal rate such as 3–3.5%.

Q. Is FIRE impossible on a low income? What sets your retirement date is your savings rate, not your absolute income. A high savings rate works twice — you accumulate faster and your target number shrinks at the same time — so even on a modest income, raising your savings rate can pull the date forward.

Q. What is sequence-of-returns risk? It’s the risk that a sharp market drop in the early years of retirement depletes your assets much faster, even at the same average return. The first few years after you retire weigh heavily on long-term success, which is why a margin of safety and flexible withdrawals (spending less when markets are bad) matter so much.

Q. What’s the difference between Coast FIRE and Barista FIRE? With Coast FIRE you invest enough while young that compounding alone reaches your target with no further saving — after that you only cover current expenses. Barista FIRE isn’t full retirement: you cover part of your income with part-time or low-intensity work and keep portfolio withdrawals to a minimum.

This article is for general informational purposes only and does not recommend any specific investment product or security. All investing carries the risk of loss of principal. The figures above are based on historical data and assumptions and do not guarantee future returns. Investment decisions are your own responsibility.