How to Start Investing With Little Money (A Realistic Plan)

“Investing is for people who already have money.” I used to believe that too. But after running money for years, the biggest thing I learned is this: the variable that decides your outcome isn’t the size of your contribution — it’s when you start and how consistently you keep at it. Let’s walk through a realistic way to start small, with verified numbers to back it up.

1. The “I Don’t Have Enough to Bother” Myth

The line I hear most from beginners is, “What’s $50 a month going to do?” I get it. It feels like a rounding error.

Then you look at the math and it changes your mind. Here’s a spoiler from the table below: $50 a month for 30 years grows to roughly $61,000 (assuming 7% annually). The point isn’t the amount — it’s the time. Small money compounding for 30 years often beats big money sitting for one.

The roadmap here is simple: ① emergency fund → ② fractional shares → ③ dollar-cost averaging → ④ compounding, diversification, fees. Follow it in order.

2. Before You Invest: The Emergency Fund

I know the itch — you want to buy your first share right now. Hold on. The foundation you have to lay first is an emergency fund.

Think of it as your goalkeeper, not your striker. When a surprise medical bill or car repair hits and you have no cash buffer, you’re forced to sell investments — usually right when the market is down. I’ve seen this play out, and it’s the most painful beginner mistake there is.

- Goal: 3 to 6 months of living expenses

- Start small: build momentum with one month’s expenses or around $1,000, then grow it

- Where to keep it: not in stocks — in a high-yield savings account (the goal is access and capital preservation)

- Never invest the emergency fund itself

For how to set a target amount and build it on autopilot, see Emergency Fund 101: How Much You Need and How to Build It Fast.

“$25 a week is about $1,300 a year.” Consistency beats size.

3. The Tool That Made Small Money Work: Fractional Shares

There was a time a stock trading at hundreds of dollars a share was simply out of reach. Now, thanks to fractional shares, you don’t have to buy a whole share.

If a stock is $1,000 and you put in $100, you own 0.1 of a share. You invest by dollar amount, not by share count. Say you have $60 and the stock is $50 — instead of buying one share and leaving $10 idle, you buy the full $60 worth, with no cash left over.

Many platforms let you start at the $1 to $5 level. The advantages are real:

- Diversify across several stocks and sectors even with little money

- Access to high-priced stocks

- Pairs beautifully with regular contributions

- Every dollar gets invested (no leftover cash sitting idle)

4. Automating Consistency: Dollar-Cost Averaging (DCA)

If fractional shares lowered the barrier, dollar-cost averaging (DCA) automates the consistency. You invest a fixed amount on a fixed schedule (weekly or monthly), regardless of price.

The mechanics are clean: with the same dollar amount, you automatically buy more shares when prices are low and fewer when they’re high. Your average cost smooths out over time.

But the real value of DCA, in my experience, is psychological. It kills the timing pressure — that “should I get in now, what if it drops more?” anxiety — and the impulsive decisions that come with it. Set up an automatic transfer on payday and discipline happens without you agonizing over it.

One honest caveat: studies show DCA does not deliver higher returns than lump-sum investing. In a long rising market, lump-sum wins on average. The point of DCA isn’t maximizing returns — it’s the accessibility and discipline that get you started and keep you going with small amounts. For a deeper look at the trade-offs, read The Pros and Pitfalls of Dollar-Cost Averaging.

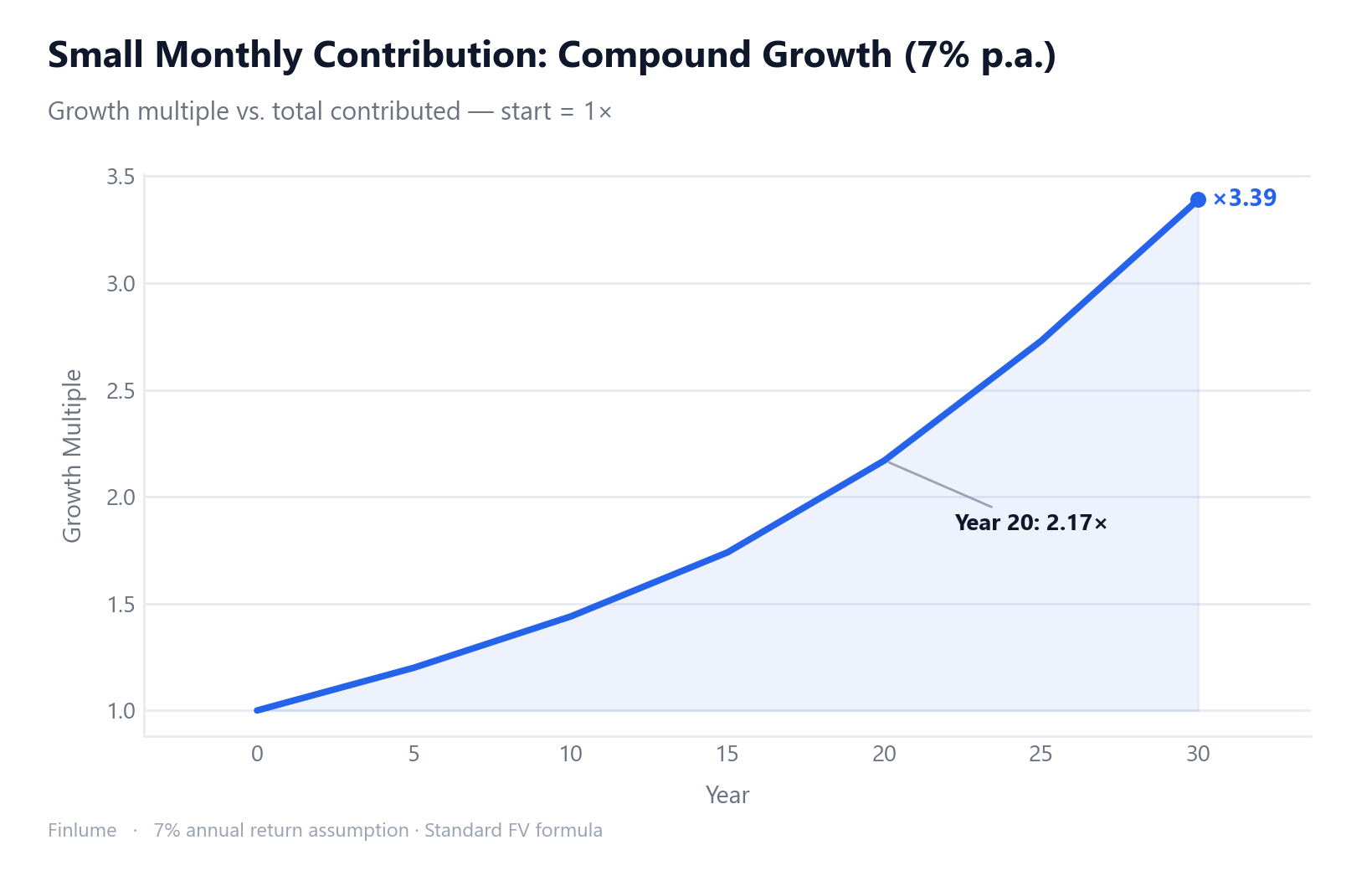

5. Time × Compounding = Small Money’s Real Weapon

Here’s the heart of it. Invest a fixed amount each month at an assumed 7% annual return, and watch what time does. (Rounded approximations using the standard future-value formula for regular contributions.)

| Monthly | 10 years | 20 years | 30 years |

|---|---|---|---|

| $100 | ~$17,300 | ~$52,000 | ~$122,000 |

| $50 | ~$8,650 | ~$26,000 | ~$61,000 |

Plotted as relative growth (start = 1×):

The shock comes when you compare to what you put in. $100/month for 30 years is roughly $122,000 — but you only contributed $36,000. The other ~$86,000 was earned by time and compounding. The principal stayed the same; time did the work.

Why 7%? The U.S. S&P 500’s long-run nominal return is about 10%, and roughly 6–7% in real (inflation-adjusted) terms over about a century of data. I used a conservative real ~7% as the assumption here. For why compounding starts slow and then accelerates, see Why Compound Interest Takes Decades to Pay Off.

⚠️ 7% is an assumption, not a guarantee. Past returns don’t guarantee future results, and you can lose principal. Every figure in the table is approximate.

6. Why Diversification and Fees Matter More When You’re Small

Diversification first. Instead of trying to pick individual winners, a single index fund or ETF that holds the whole market spreads you across hundreds or thousands of companies automatically. Fractional shares plus an index ETF gives you broad diversification with very little money — the most realistic approach for a beginner. If you’re weighing the two, see Index Funds vs. Individual Stocks: Which Is Better for Beginners?.

Next, fees (the expense ratio). This bites small investors harder, because fees compound too — you lose not just the money paid, but the growth that money would have earned.

There’s a widely cited SEC example. Hold $100,000 growing at 4% a year for 20 years:

| Annual fee | Balance after 20 years |

|---|---|

| 0.25% | ~$208,000 |

| 1.00% | ~$179,000 |

A mere 0.75-percentage-point difference costs about $30,000 (~14%) over 20 years. Intuitively: a 0.25% expense ratio is $25 a year per $10,000 invested. Good index funds often run under 0.10% (under $10 per $10,000), while active funds typically charge 0.50–1.50%. Check for low-cost platforms and low-expense index funds.

The Hidden Cost of Waiting: A Start-Age Lookup Table

The article has said “start early” several times. Here is what that actually costs in numbers — computed using the standard future-value formula for regular contributions at an assumed 7% annual return, all investing until age 65.

Assumption: 100 units/month invested until age 65, 7% annual return (assumed, not guaranteed). “Units” are currency-neutral — scale to your own monthly amount.

| Start Age | Years Invested | Total Contributed | Final Balance | Growth Multiple | vs. Starting at 25 |

|---|---|---|---|---|---|

| 25 | 40 | 48,000 | ~262,500 | 5.47× | baseline |

| 30 | 35 | 42,000 | ~180,100 | 4.29× | −31% |

| 35 | 30 | 36,000 | ~122,000 | 3.39× | −54% |

| 40 | 25 | 30,000 | ~81,000 | 2.70× | −69% |

The paradox is in the last two columns together. Someone starting at 35 contributes 75% as much money as someone starting at 25 (36,000 vs. 48,000 units), yet ends up with only 46% of the final balance (~122,000 vs. ~262,500). A 25% reduction in contributions produces a 54% reduction in outcome — because those ten missing years were the compounding runway, not just the contribution window.

Waiting five years from 25 to 30 costs 31% of your final balance. Waiting ten years costs more than half. The early years have a disproportionate weight — not because the math is magic, but because each early dollar has the longest time to multiply. This is why every month you delay is more expensive than the one before it.

All figures are approximations. Assumes a constant 7% nominal annual return, contributions made monthly, no taxes or fees deducted. Past returns do not guarantee future results.

7. Key Takeaways — 4 Steps to Start Today

No need to overcomplicate. Just go in order.

- Emergency fund first — 3–6 months in a high-yield account. Start small, grow it.

- Automatic, fixed contributions (DCA) — set up a transfer on payday and make it a habit.

- Diversify with a low-cost index ETF — one fund, hundreds or thousands of holdings.

- Check the fees — lower is better (they compound against you).

- Don’t delay the start — waiting 5 years from age 25 costs ~31% of your final balance; waiting 10 years costs ~54%, even though you only contribute 25% less.

Having little money was never the real problem. Putting off the start was. Even $50 a month — the single act of setting up that transfer today — may be the decision you thank yourself for 30 years from now.

Frequently Asked Questions

How much money do I need to start investing? Many platforms let you buy fractional shares starting at the $1 to $5 level, so the entry barrier is tiny. Consistency matters more than the amount: even $50 a month grows to roughly $61,000 over 30 years at an assumed 7% annual return. What decides your outcome isn’t the size of your contribution — it’s when you start and how consistently you keep at it.

Should I start investing or build an emergency fund first? Build the emergency fund first. Without a cash buffer, a surprise medical bill or car repair can force you to sell investments at a loss, often right when the market is down. Aim for 3 to 6 months of living expenses, kept in a high-yield savings account rather than stocks. Never invest the emergency fund itself.

Does dollar-cost averaging beat lump-sum investing? No. Studies show DCA does not deliver higher returns than lump-sum investing, and in a long rising market lump-sum wins on average. The real value of DCA isn’t maximizing returns — it’s the accessibility and discipline that let you start small, stay consistent, and avoid the stress of timing the market.

Why do fees matter more for small investors? Fees compound against you: you lose not just the money paid, but the growth that money would have earned. In a widely cited SEC example — $100,000 growing at 4% for 20 years — the gap between a 0.25% and a 1.00% annual fee is about $30,000 (roughly 14%). Look for low-cost platforms and low-expense index funds.

Disclaimer: This article is for information only and is not investment advice. Returns are not guaranteed, past performance does not guarantee future results, and you can lose principal. Take a long-term view.