Index Funds vs. Individual Stocks: Which Is Better for Beginners?

Newer investors ask me one question more than any other: “Should I buy an index fund, or just pick a few good stocks myself?”

I was a stock-picker first, for what it’s worth. My thinking was, “Why settle for the average when I can pick winners and win big?” The result? It took me a few wandering years before I sat down and actually looked at the data. Today I want to walk you through that data.

1. The First Fork in the Road Every Beginner Hits

Let’s define the terms in one sentence each. An individual stock means buying a direct stake in one specific company. An index fund means buying one basket that holds the whole market at once (say, the 500 largest companies).

The first says, “If the company I picked does well, I win big.” The second says, “I track the market average.” Intuitively the first sounds sexier. Who wants to settle for average?

But this article answers exactly one question: From a beginner’s seat, which is the statistically better bet? Not by gut feel. By the numbers.

2. The Uncomfortable Truth: The Average Stock Loses to the Market

There’s one study that makes you pause. Bessembinder (2018) ran the numbers on all 25,967 U.S. listed stocks from 1926 to 2016, roughly 90 years.

The findings are sobering. More than half of all stocks (about 57%) returned less over their lifetime than a one-month Treasury bill. They underperformed a boringly safe government bond. More striking: essentially 100% of the net wealth the market ever created came from the top ~4% of stocks (exactly 1,092 companies). The other 95.7%, combined, barely matched T-bills. The top 90 stocks alone (about 0.36% of all of them) accounted for more than half of all the wealth created.

In plain English: stock returns are extremely concentrated in a tiny handful of mega-winners. So when you pick a few at random, the “average stock” is actually closer to a loss. It’s like buying a lottery ticket without knowing which numbers won.

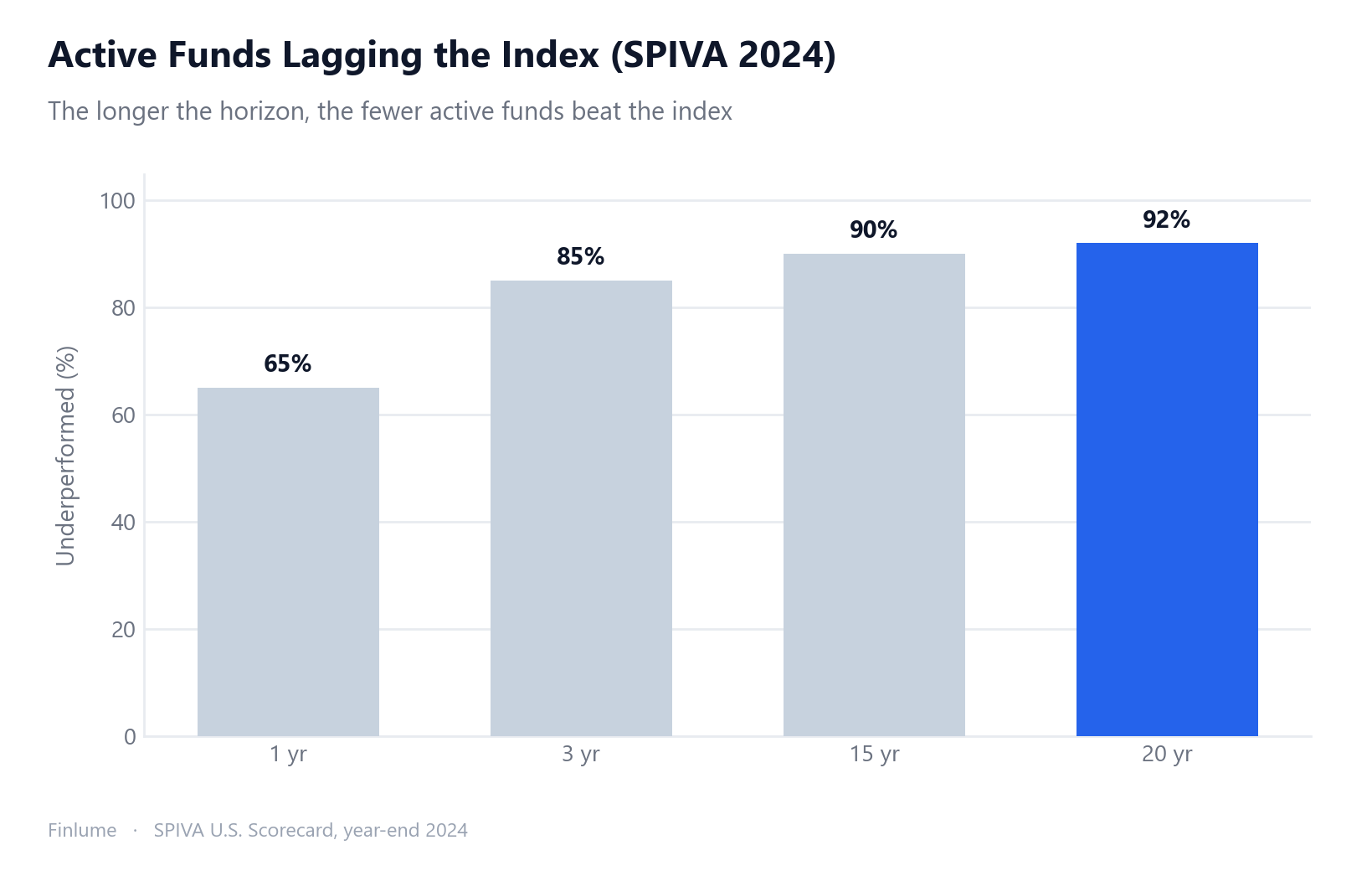

3. Even the Pros Lose: The SPIVA Scorecard

“Sure, that’s random picking. I’d pick the good ones.” Fair. So how do the professionals who analyze stocks all day do?

Look at S&P’s annual SPIVA report (year-end 2024). In 2024 alone, 65% of U.S. large-cap active funds failed to beat the S&P 500. Stretch the timeline and it gets brutal.

| Period | Active funds that lagged the index |

|---|---|

| 1 year | ~65% |

| 3 years | ~85% |

| 15 years | ~90% |

| 20 years | ~92% |

Over 15 years, not a single category had a majority of funds beat their index. Nine out of ten paid, full-time professionals lost to the index over 15 years. So what are the odds for a beginner glancing at tickers after work? I’ll let you do that math.

4. The Power of Diversification: Why One Click Replaces Dozens of Picks

There are two kinds of risk. Unsystematic risk (the risk a single company blows up) and systematic risk (the risk the whole market drops). The first you can diversify away; the second you can’t.

The catch is that to diversify properly with individual stocks, you typically need dozens or more (traditionally 20 to 30, stricter studies say 50+) and then you have to manage them. A beginner buying, tracking, and rebalancing all of that while holding down a day job? Honestly, close to impossible.

An index fund gets you diversified across roughly 500 companies in a single purchase, so-called “instant diversification.” Diversification doesn’t erase every risk, though, which I unpack in how diversification reduces risk and where it quietly fails. Worth noting: per JP Morgan’s analysis, even within the S&P 500, an average of about 151 stocks fall more than 5% in a given year, and over the long run more than half of stocks actually destroyed shareholder value. Winners and losers separate even inside the index, and the index spares you the burden of telling them apart.

5. The Two Invisible Enemies: Fees and Your Own Emotions

Two things never show up on the return chart but quietly eat your wealth over time.

First, fees. The average passive index fund charges roughly 0.05% to 0.11%, and broad-market ETFs drop into the 0% range. Active funds, by contrast, average roughly 0.42% to 0.59%, with some hitting 1.50%. Sounds trivial? Compounding changes the story.

Say you invest $10,000 at 7% a year for 30 years. At 0.05% annual cost you end with about $75,063. At 1.0% you end with about $57,435. The gap is roughly $17,600, meaning about 23.5% of your final wealth evaporated into fees. A 0.95-percentage-point difference per year eats a quarter of your money over 30 years. If you want the full mechanics of why a small fee compounds into so much, see why a 1% fee quietly costs you half your retirement.

Second, your emotions. Per Morningstar’s “Mind the Gap” (10 years through year-end 2024), investors’ actual returns trailed the funds’ own returns by about 1.1 percentage points a year, surrendering roughly 15% of potential gains over the decade. The culprit: buying high, panic-selling low. That’s the same reason market timing fails in long-term investing. Individual stocks are more volatile and tempt you to fiddle more often, which tends to widen that gap.

5b. The Alpha Hurdle: How Much Edge Do You Actually Need?

Here’s a number most articles skip entirely. To merely keep pace with a low-cost index fund, a stock picker doesn’t just have to match the market — they have to beat it by a meaningful margin every single year.

The math is straightforward (assumptions stated explicitly below). Assume the market returns 7%/yr gross. An index fund at 0.05% fee nets 6.95%/yr. A DIY stock picker incurs realistic costs — brokerage commissions, bid-ask spreads, and the occasional tax drag — which I’ll conservatively peg at 0.75%/yr total. That means the picker’s net return is (7% + their alpha) − 0.75%. Solving for the break-even point:

Index net = Picker net → 6.95% = 7% + alpha − 0.75% → break-even alpha = +0.70%/yr

A stock picker must outperform the raw market by at least +0.70 percentage points per year, every year, consistently just to end up where a passive investor lands doing nothing but holding. The table below shows what happens across a range of realistic alpha scenarios (starting value = 1.00 in all cases):

| Scenario | Net return/yr | 10 yr | 20 yr | 30 yr |

|---|---|---|---|---|

| Stock picker (alpha +2.0%) | 8.25%/yr | 2.21× | 4.88× | 10.79× |

| Stock picker (alpha +0.7%) — break-even | 6.95%/yr | 1.96× | 3.83× | 7.51× |

| Stock picker (alpha 0%) — matches market gross | 6.25%/yr | 1.83× | 3.36× | 6.16× |

| Stock picker (alpha −1.0%) — slightly below market | 5.25%/yr | 1.67× | 2.78× | 4.64× |

| Stock picker (alpha −2.0%) — underperforms | 4.25%/yr | 1.52× | 2.30× | 3.49× |

| Index fund (passive) | 6.95%/yr | 1.96× | 3.83× | 7.51× |

Assumptions: market gross return 7%/yr; index fund cost 0.05%/yr; stock picker costs 0.75%/yr (brokerage, spreads, incidental tax drag — conservatively estimated); alpha = annual outperformance versus the raw market return. All figures are illustrative growth multiples on a starting value of 1.00. Past market returns do not guarantee future results.

The row to stare at is “alpha 0% — matches market gross.” A picker who genuinely has no edge but thinks they’re average ends up at 6.16× vs 7.51× over 30 years — about 18% less final wealth — simply from the cost gap. And recall from the SPIVA data above: most active professionals don’t achieve consistent positive alpha. A beginner starting cold would need to clear the +0.70% hurdle every year, net of all costs, to just break even.

6. But Index Funds Aren’t a Magic Bullet

If you’ve read this far and concluded “index funds are always the answer,” that’s not my point. Let’s stay balanced.

Index funds never escape systematic risk, the whole market dropping. If the market falls 30%, your index falls 30% right along with it. “I’m diversified, so I’m safe” is only half true. The index removes single-company risk; it leaves market risk fully on your shoulders.

There are cases where individual stocks make sense. If you genuinely understand a specific industry deeply, and you invest a small amount you can afford to lose, for learning and experience, go for it. Nothing teaches you how investing actually feels like holding one position and riding its swings. But that’s strictly a “learning” allocation, not your core.

7. A Practical Verdict and Checklist for Beginners

After plenty of trial and error, the structure I suggest to newcomers is simple: hold low-cost, diversified index funds as your core for the long haul, and keep individual stocks to a small learning allocation. With the index as your core, how you split between stocks, bonds, and cash is the next decision, and a guide to asset allocation walks through it.

The key takeaways:

- Accept the odds: Even pros lose to the index ~90% of the time over 15 years. A beginner’s stock-picking duel is a statistically unfavorable bet.

- Understand concentration: Individual stocks aren’t high return, they’re high concentration. The average stock leans toward a loss.

- Instant diversification: One index purchase spreads you across hundreds of companies. If you can’t manage dozens yourself, this is your answer.

- Defend against fees: A 1-point annual difference eats about a quarter of your wealth over 30 years. Always check the expense ratio.

- Control emotions: Chasing highs and panic-selling cost about 1.1 points a year. Looking less often is how you win.

- Know the hurdle: A stock picker must beat the market by +0.70%/yr just to match the index’s net return. A picker with no edge ends up ~18% poorer over 30 years purely from cost drag.

As someone who started flashy and then floundered, let me leave you with this: investing isn’t a contest of cleverness, it’s a contest of consistency and cost control. Quietly capturing the average beats most people in the end. Go slow, but don’t stop.

FAQ

Q. As a beginner, should I start with index funds or individual stocks? For most beginners, starting with low-cost, diversified index funds as your core is the statistically better bet, because even professionals lose to the index about 90% of the time over 15 years. Keep individual stocks to a small amount you can afford to lose, purely for learning.

Q. Are index funds a safe, loss-proof investment? No. An index fund removes single-company (unsystematic) risk, but it carries full market (systematic) risk. If the market falls 30%, your index falls 30% with it. “I’m diversified, so I’m safe” is only half true.

Q. Is the difference between a 0.05% and a 1.0% fee really that big? With compounding, yes. Investing $10,000 at 7% for 30 years ends at about $75,063 with a 0.05% fee versus about $57,435 with a 1.0% fee. That 0.95-point annual gap surrenders roughly 23.5% of your final wealth, about a quarter, to fees.

Q. Should beginners never buy individual stocks? Not necessarily. They can make sense if you genuinely understand an industry and invest a small amount you can afford to lose, for learning and experience. Just treat it as a learning allocation, not your core.

Q. Why do investors earn less than the index even when they hold one? Usually emotions. Morningstar found investors’ actual returns trailed the funds’ own returns by about 1.1 percentage points a year, driven by buying high and panic-selling low. Looking less often and holding for the long haul is how you close that gap.