The Pros and Pitfalls of Dollar-Cost Averaging

Same day, same amount, automatically — every month. That one boring habit quietly sidesteps the two hardest questions in investing: “When should I buy?” and “It’s dropping, do I dare add more?” Let me say it up front: dollar-cost averaging is a calm, sensible way to invest, but it is not a guarantee of profit. Today we’ll walk through what it genuinely does for you, and where it quietly lets you down.

What dollar-cost averaging actually is

Dollar-cost averaging, or DCA, sounds fancier than it is. The whole idea is this: you invest the same fixed amount at regular intervals, no matter what the price is doing. $300 into the same fund or ETF on the first of every month, rain or shine.

The magic word is “fixed amount.” When the price is high, your $300 buys fewer shares; when it’s low, it buys more. A simple rule does the thing your brain is terrible at doing under stress.

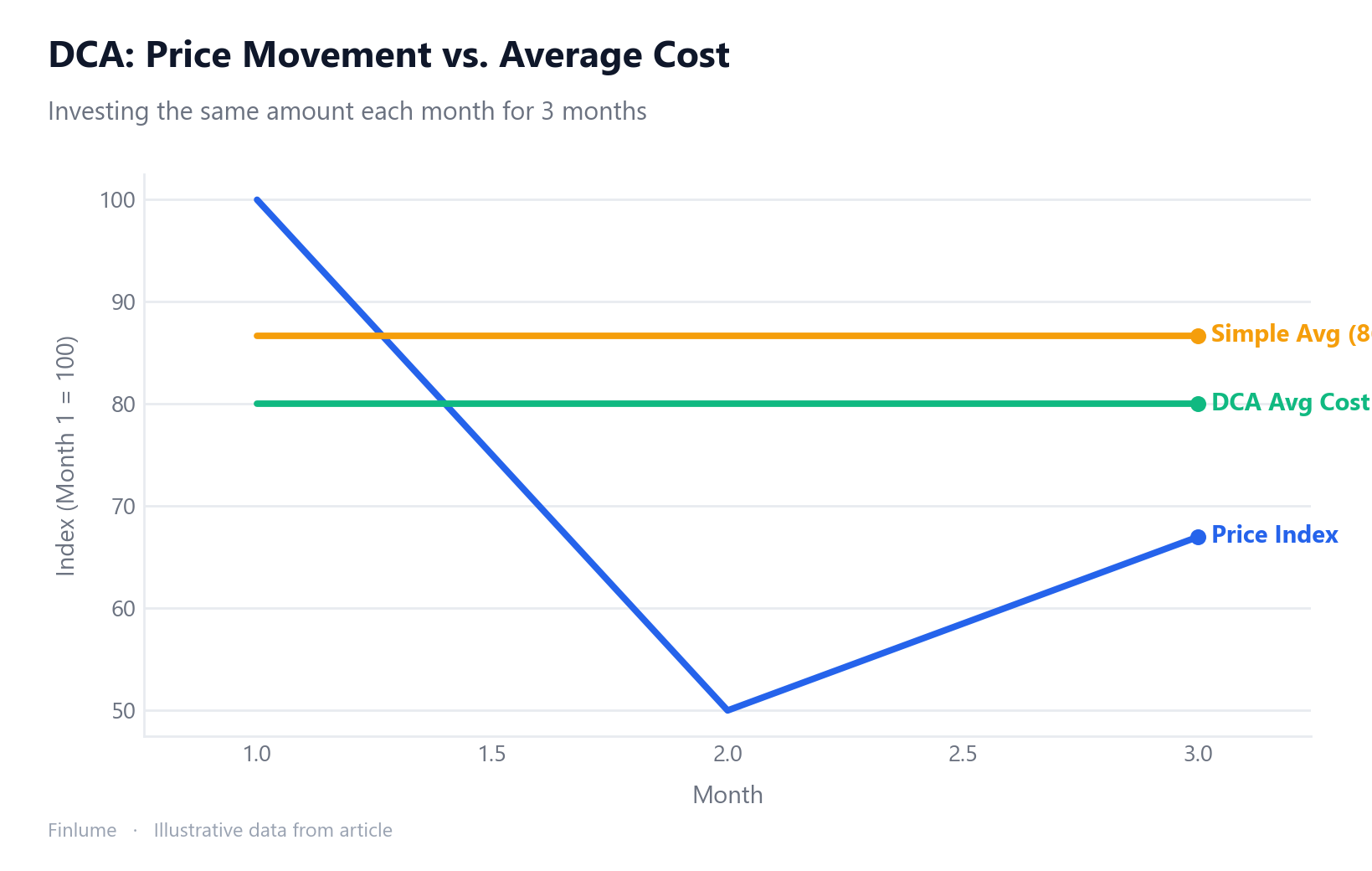

How it lowers your average cost

Here’s a quick example. You put in $120 a month for three months, and the price moves like this:

| Month | Price/share | Invested | Shares bought |

|---|---|---|---|

| 1 | $12 | $120 | 10 |

| 2 | $6 | $120 | 20 |

| 3 | $8 | $120 | 15 |

| Total | — | $360 | 45 |

The simple average of the three prices is ($12 + $6 + $8) ÷ 3 = $8.66. But your actual average cost is $360 ÷ 45 = $8.00. Because you bought more shares when they were cheap, your cost came in below the plain average. That’s the mathematical charm of DCA.

The biggest benefit is psychological

Honestly, the numbers aren’t even the best part. DCA’s real gift is that it lets you stop trying to time the market at all. Once you understand why market timing fails in long-term investing, giving up the attempt feels less like surrender and more like a smart move. Anyone who once went all-in at a peak and got stuck knows the feeling — that single decision haunts you for years.

Early on, I’d wait for “just a little lower” and miss the bounce, then panic-buy near a top because “if I don’t get in now I’ll miss it.” Setting up an automatic transfer finally ended that tug-of-war. When the market drops, I now think, “Next month the same money buys more” — and a falling market gets a lot less scary. That steadiness is the real fuel that keeps you invested for the long haul — which is the one condition for reaping the rewards of why compound interest takes decades to pay off.

Pitfall one: in a rising market, lump sum usually wins

This is the part where I drop the jokes and just give it to you straight. DCA is not always the better choice.

If you already have a chunk of cash, studies comparing investing it all at once (lump sum) versus spreading it out (DCA) are remarkably consistent. As long as markets trend upward over time, lump sum beats DCA on average. One widely cited Vanguard analysis found lump sum came out ahead roughly two-thirds of the time.

The reason is simple: markets rise on more days than they fall, so the longer your money sits on the sidelines, the less of that climb it captures. The “spreading out” in DCA doesn’t just split your risk — it splits your potential return too.

Pitfall two: it is not insurance against loss

This is the most common misunderstanding: “I’m dollar-cost averaging, so I can’t really lose.” Wrong. DCA spreads out your entry-point risk; it does nothing to stop the asset itself from falling. If what you’re buying grinds downward for years, no amount of lowering your average will pull the account out of the red. Lowering your average only helps when you’re buying a good asset while it’s cheap — it is not a tool for diligently catching a falling knife. Which means the choice of what you average into matters more than the method itself — a point that ties directly into why higher returns always come with higher risk. The method alone does not make risk disappear.

So who is it actually for

Here’s the bottom line. If you invest a slice of each paycheck, you don’t really have a choice — you have no lump sum, so DCA is the natural answer, and the psychological perks come free. If a small starting balance has you stuck, how to start investing with little money is a useful companion read. If instead you’re holding a windfall, an inheritance, or a payout, know that lump sum wins on average, but if “putting it all in and watching it crash the next morning” would cost you your sleep, the calmer DCA route is perfectly fine. The right answer isn’t the highest return; it’s the strategy you can actually stick with.

The volatility break-even: when does DCA actually win?

The article already said lump sum beats DCA “roughly two-thirds of the time.” But that figure hides something important: it depends almost entirely on how volatile the asset is. Run the numbers across realistic scenarios and a clear threshold emerges.

The table below is based on 100,000 Monte Carlo simulations each — 12 monthly contributions versus investing the whole sum at the start, over a 12-month deployment window, assuming a 7% annual return (all scenarios identical except volatility).

| Asset type | Annual volatility | Lump sum wins | Median LS edge | Verdict |

|---|---|---|---|---|

| Bonds / low-vol fund | ~12% | 66% of the time | +2.8% | Lump sum favored |

| Broad equity index | ~20% | 58% of the time | +2.1% | Lump sum favored |

| Small-cap / sector fund | ~35% | 50% of the time | ~0% | Roughly a coin flip |

| Single stocks / high-vol | ~50%+ | 45% of the time | −3.5% | DCA favored |

Assumptions: 7% annual drift (geometric Brownian motion), 12 equal monthly installments, no transaction costs.

Two things stand out. First, the “lump sum wins two-thirds of the time” figure specifically applies to low-volatility assets — as volatility rises, the advantage shrinks fast. Second, when DCA does win at high volatility (35%+ annual), it wins by a meaningful margin — the conditional median DCA edge when DCA wins at 35% vol is roughly +11%, compared to the conditional median LS edge of only about +6% when LS wins at 12% vol. In other words: DCA’s losses are frequent but small; DCA’s wins are rare but chunky.

The practical read: for a diversified broad-market ETF running ~15–20% annual volatility, lump sum is the mathematically superior default roughly 58–66% of the time — but the typical advantage is only about 2%. For a concentrated single-stock bet at 50%+ volatility, the math actually flips, and DCA becomes the rational choice. Most investors sit squarely in the 15–20% volatility range, which is why the standard advice (“lump sum if you have it”) holds — but it holds by less than people assume.

Key takeaways

- DCA = the same amount, on a schedule, regardless of price

- You buy more when it’s cheap, which lowers your average cost

- Its biggest strength is removing timing stress

- In rising markets, lump sum tends to beat DCA on average if you have the cash

- DCA is not insurance against loss — what you buy matters more

- It’s the most natural fit for anyone with a regular income

- The lump-sum advantage shrinks as volatility rises — at ~35% annual vol it disappears entirely, and above ~40% DCA takes the edge

Frequently asked questions

Is dollar-cost averaging or lump-sum investing better? As long as markets trend upward over the long run, lump sum beats DCA on average when you already hold the cash — one widely cited analysis found lump sum came out ahead roughly two-thirds of the time. That said, if a sudden drop right after investing everything would shake you out, the calmer DCA route is a perfectly reasonable choice.

Does dollar-cost averaging protect me from losing money? No. DCA spreads out your entry-point risk, but it does nothing to stop the asset itself from falling. If what you bought grinds downward for years, lowering your average cost won’t pull the account out of the red. That’s why what you average into matters more than the method.

How often and how much should I invest with DCA? The point isn’t a magic amount or frequency — it’s investing the same fixed amount at regular intervals, regardless of price. Tying an automatic transfer to your payday is the most natural setup, with an amount you can comfortably keep up over the long haul.

Does DCA always lower my average cost? When prices swing up and down, your fixed amount buys more shares when they’re cheap, pulling your average cost below the simple price average. But that only fine-tunes your entry price — in a market that only rises, getting in early with a lump sum can beat DCA.

There’s no perfect method. But for an ordinary investor, few things are as reliable as automating your own consistency. Start with a single automatic transfer this week and let it run.