ETFs Explained: What They Are and How They Actually Work

Invest in hundreds of assets at once, and trade the whole thing as easily as buying a single stock. That might sound like something dreamed up in a marketing meeting, but it’s exactly what ETFs deliver — and investors worldwide have taken notice. As of 2025, global ETF assets exceed roughly $19 trillion. That number tells you this isn’t a niche product anymore; it’s become the default way millions of people access financial markets.

This guide covers how ETFs actually work under the hood: the creation and redemption mechanism, how pricing stays honest, the differences from mutual funds, and the three things worth checking before you buy your first one.

What an ETF Is

ETF stands for Exchange-Traded Fund. The name is the whole pitch: it’s a fund (a basket of multiple assets) that trades on an exchange (like a stock, in real time).

Most ETFs are built around an index — a predefined list of securities with fixed rules for inclusion. An S&P 500 ETF, for example, holds all 500 companies in that index in roughly their index-weight proportions. The ETF doesn’t decide what to buy; it just follows the rules. That passive approach keeps costs low and removes the unpredictability of active stock-picking. If you’re weighing this against buying individual companies, our breakdown of index funds vs. individual stocks goes deeper on the trade-off.

Here’s the analogy I keep coming back to: think of a streaming playlist curated by an algorithm — you get the whole genre in one click, not just your favorite track. An ETF works the same way. You buy the basket, not each item in it individually.

How ETF Trading Works

If you’ve ever placed a stock trade, ETF trading is identical. You can buy or sell at the current market price any time the exchange is open. Want to set a specific price? Use a limit order. Need to exit quickly? Market order works the same way.

A term worth knowing: NAV (Net Asset Value). NAV is the total value of everything inside the ETF basket divided by the number of shares outstanding — in other words, what each share is theoretically worth based on its holdings. During market hours, the ETF’s actual price can deviate slightly from NAV due to supply and demand.

That gap matters for one practical reason: the bid-ask spread. In highly liquid ETFs (think large-cap index funds with millions of daily trades), the spread is tiny — sometimes a penny or less. In thinly traded ETFs, the spread can be meaningfully wider, meaning you’re paying a hidden cost every time you transact. It’s something to watch, especially in smaller or more specialized funds.

How ETFs Are Created and Redeemed

This is the mechanism that most investors never think about — but it’s what keeps ETF prices honest.

Everyday investors buy and sell ETFs on the exchange between each other. But a separate process handles the creation of new ETF shares and the retirement of existing ones. That process involves Authorized Participants (APs) — large financial institutions that have a direct relationship with the ETF issuer, the creation-and-redemption mechanism the SEC details in its investor bulletin on ETFs.

Creation: An AP assembles the exact basket of securities that the ETF holds, delivers that basket to the ETF issuer, and receives large blocks of new ETF shares (called Creation Units) in return. Those shares then flow into the market.

Redemption: The AP hands back a block of ETF shares to the issuer and receives the underlying securities in return.

This back-and-forth creates a powerful self-correcting mechanism. If the ETF’s market price rises above NAV, APs can buy the cheaper underlying stocks, create ETF shares, and sell those shares at the higher market price — pocketing a risk-free spread. That extra supply pushes the ETF price back toward NAV. The reverse happens when the ETF trades below NAV. I’ve seen this described as a “price gravity” system: the market pulls ETF prices back toward fair value automatically.

One more important detail: the in-kind exchange (securities for ETF shares, not cash) is why ETFs tend to be more tax-efficient than mutual funds in many jurisdictions. More on that below.

Types of ETFs

The ETF structure has been applied to nearly every asset class imaginable. Here’s a quick map:

| Type | What It Tracks | Key Note |

|---|---|---|

| Equity ETF | Stock index (broad or sector) | Most common, passive is dominant |

| Bond ETF | Fixed income index | Lower volatility, sampling common |

| Commodity ETF | Gold, oil, agricultural goods | May use futures, not just physical holdings |

| Global/Regional ETF | Developed or emerging markets | Geographic diversification |

| Active ETF | Manager discretion | Higher cost, seeks to beat an index |

| Thematic ETF | Specific trends or industries | Concentrated risk — use carefully |

The passive vs. active split matters beyond strategy. It’s a cost story too, which the next section covers.

ETF vs. Mutual Fund

Both are pooled funds. Both give you exposure to a diversified basket. But they’re built and operated differently.

| Feature | ETF | Mutual Fund |

|---|---|---|

| Trading hours | Real-time, market hours | Once per day, after market close |

| Price | Live market price | End-of-day NAV |

| Minimum investment | One share | Often a fixed minimum |

| Typical cost | Lower (passive) | Generally higher |

| Tax efficiency | Structurally favorable | Less favorable |

The tax efficiency gap comes from that in-kind redemption process I described earlier. When mutual fund investors redeem, the fund often sells holdings to raise cash — triggering taxable capital gains that get distributed to all shareholders, even those who didn’t sell. ETFs largely avoid this through the in-kind exchange with APs.

That said: “ETFs are always more tax-efficient” is too strong a claim. Tax treatment varies by country, account type, and fund structure. The structural advantage is real, but treat it as a tendency, not a guarantee.

One thing I’d flag about intraday trading: the ability to trade anytime sounds like a feature, but for long-term investors it can also be a temptation. The discipline to hold through volatility matters more than the mechanics of when you can trade. Mutual funds, ironically, enforce a kind of patience by design.

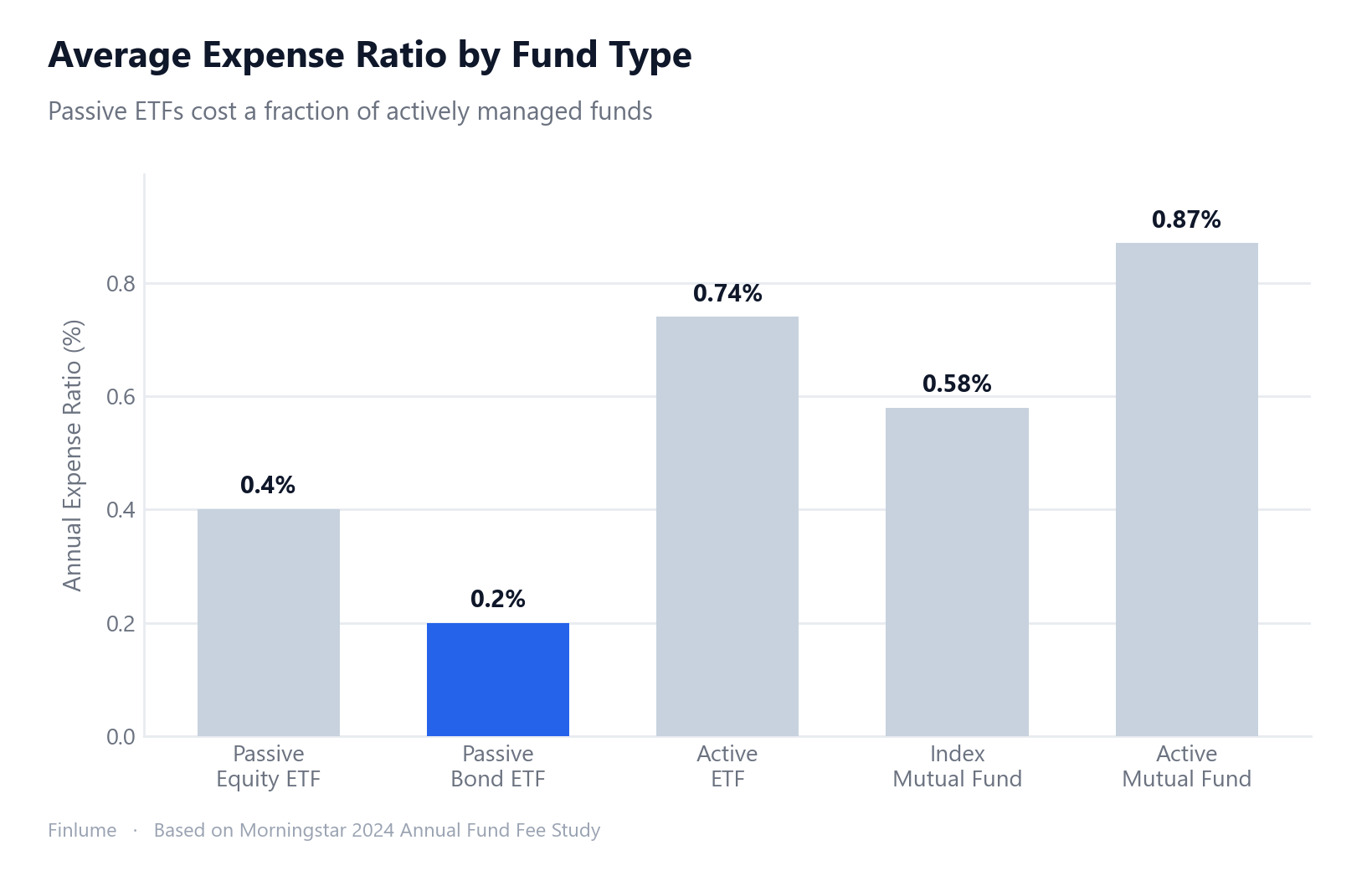

Costs, Tax Efficiency, and Risks

Costs: The annual fee charged by an ETF is called the expense ratio (or total expense ratio, TER). Here are the typical ranges:

- Passive index ETFs: approximately 0.03–0.50% per year

- Actively managed ETFs: approximately 0.5–1%+ per year

These numbers have trended down over the past two decades due to competition, and that’s good news for investors. A 0.05% fee versus a 1.0% fee might look trivial on an annual statement, but compound that difference over 20 or 30 years and it becomes a material drag on your final balance.

Tax efficiency: Covered above — the in-kind mechanism is the structural reason ETFs tend to generate fewer taxable distributions than mutual funds. Actual tax impact depends on your jurisdiction and account type.

Risks to keep in mind:

- Tracking error: The gap between what the ETF returns and what its benchmark index returns. Bond ETFs that use sampling (holding a representative subset rather than every bond in an index) can show higher tracking error than equity ETFs that hold all constituents.

- Bid-ask spread: A real but often overlooked cost, especially relevant in low-volume ETFs. Check daily trading volume before you buy.

- Market risk: ETFs are a delivery mechanism, not a shield. A broad market ETF will fall when the market falls. Diversification reduces single-stock risk; it doesn’t eliminate market-wide downturns. It’s worth understanding how diversification reduces risk — and where it quietly fails before you assume an ETF makes you bulletproof.

Three Things to Check Before Buying Your First ETF

Looking for “the best ETF” is the wrong framing. A more useful question: what separates a reasonable choice from a poor one?

① Check the underlying index. What exactly does this ETF own? Two ETFs with similar-sounding names can have very different compositions. Read the fund’s fact sheet, not just the marketing name.

② Check the expense ratio. If two ETFs track the same index, the one with the lower expense ratio will deliver better results over time, all else equal. This is one of the few genuinely predictable advantages in investing.

③ Check size and liquidity. A fund with very few assets under management or very low daily trading volume carries two risks: wide spreads (you pay more to get in and out) and potential closure (small ETFs do get shut down, forcing you to reinvest at an inconvenient time).

These three aren’t a formula for finding the perfect ETF. They’re a filter for eliminating obvious mistakes. Once you’ve run your candidates through the filter, the remaining choice depends on your goals and time horizon.

What One ETF Share Actually Buys: The Diversification Math

An ETF’s defining feature isn’t its fee — it’s that a single share spreads your money across the entire basket at once. It’s worth quantifying how much single-company risk that actually removes.

| What $1,000 buys | Approx. holdings | Largest single name (cap-weighted) | If that one company went to zero |

|---|---|---|---|

| One individual stock | 1 | 100% | −$1,000 (−100%) |

| Narrow sector / thematic ETF | ~25–40 | ~10–20% | −$100 to −$200 |

| S&P 500 ETF | ~500 | ~6–7% | ~−$60–70 (top) / ~−$1 (average holding) |

| Total US market ETF | ~3,500+ | ~5–6% | ~−$50–60 (top) / under −$1 (average holding) |

Holdings counts and weights are approximate and cap-weighted — broad indices are more top-heavy than the raw holding count suggests. Illustrative, not a specific fund’s figures.

The single-stock holder can be wiped out by one bankruptcy (Enron and Lehman shareholders lost nearly everything); the S&P 500 ETF holder loses a rounding error — under a dollar per $1,000 — from the identical event. Transferring that catastrophic single-name risk into a survivable rounding error is the entire point of the ETF wrapper.

Cap-weighting is the catch: “500 stocks” is not 500 equal bets — the largest handful carry outsized weight, so a broad ETF is diversified but not perfectly even. Even so, the worst-case single-name risk drops from −100% to a fraction of a percent, which is why a basket beats a bet on any one company.

Key Takeaways

- ETF = diversification of a fund + real-time tradability of a stock. Both in one instrument.

- NAV is the true value of the basket’s holdings. APs arbitrage any price gaps back toward NAV.

- In-kind creation and redemption keeps prices stable and creates structural tax efficiency.

- Passive ETF costs: roughly 0.03–0.50%/year. Active: roughly 0.5–1%+/year. Long-term, the difference compounds.

- Key risks: tracking error (larger in sampled bond ETFs), bid-ask spread (higher in illiquid funds), and market risk (diversification doesn’t prevent market-wide losses).

- Before buying: check the index, the expense ratio, and the fund’s size and liquidity.

- Fee drag is non-linear: a 0.82% annual TER gap costs roughly 21% of your 30-year ending value — a 1.55× shortfall on the starting amount (assuming 7% gross return).

Once you understand how ETFs are assembled, priced, and traded, they stop being mysterious. They’re one of the more transparent and cost-efficient tools available to individual investors — as long as you know what you’re actually buying. Which ETFs you hold, and in what proportion, ultimately flows from your asset allocation — that’s the decision that drives most of your long-run results.

Frequently Asked Questions

Q. What is the difference between an ETF and a stock?

A stock gives you ownership in one company. An ETF is a basket of dozens or hundreds of assets that you buy in a single transaction. Both trade on exchanges during market hours, but an ETF comes with built-in diversification — that’s the key difference.

Q. Can an ETF’s market price differ from its NAV?

Yes. During trading hours, supply and demand can push an ETF’s price slightly above or below its net asset value (NAV). Authorized Participants correct this gap through arbitrage, which is why most ETFs trade very close to NAV most of the time.

Q. How much does an ETF typically cost?

Passive index ETFs commonly charge around 0.03–0.50% per year. Actively managed ETFs typically run 0.5–1%+ annually. Over decades of compounding, even a seemingly small fee difference compounds into a significant drag on returns.

Q. What should I check before buying my first ETF?

Check three things: ① the underlying index (what exactly does this ETF own?), ② the expense ratio (lower is better for the same index), and ③ size and liquidity (very small ETFs can have wide spreads and closure risk). Think of these as filters that eliminate bad choices, not a formula for finding the perfect one.

Q. What is the difference between an ETF and a mutual fund?

Both are pooled funds holding a diversified basket, but an ETF trades on an exchange in real time during market hours, while a mutual fund is priced once per day at its closing NAV. Passive ETFs are generally lower-cost, and ETFs tend to be more tax-efficient thanks to their structure.

Q. How are ETFs created and redeemed?

Large institutions called Authorized Participants (APs) deliver the ETF’s underlying basket of securities to the issuer and receive large blocks of new ETF shares (Creation Units) in return — that’s creation. Redemption is the reverse: an AP returns ETF shares and receives the underlying securities. This mechanism keeps the ETF’s market price anchored near its NAV.

Q. Why are ETFs more tax-efficient than mutual funds?

Because redemptions happen in-kind — securities are swapped for ETF shares rather than sold for cash — ETFs generate fewer taxable events like realized capital gains. That said, tax treatment varies by country and account type, so it’s a structural tendency, not a guarantee.