7 Psychology-Backed Strategies to Stop Impulse Buying (Use Systems, Not Willpower)

We’ve all had that morning-after moment: you tap “Buy now,” and the next day you stare at the order and think, “Why did I get this?” I’ve spent years looking at spending data, and I still catch mystery charges on my own statement. So let me say it plainly up front — impulse buying isn’t a sign that you’re weak. It’s a sign that your brain is doing exactly what it was built to do.

1. Impulse Buying Is Brain Design, Not a Willpower Flaw

Behavioral economists talk about present bias: we feel a small reward right now far more intensely than a bigger payoff later. That “Buy now” button is aimed straight at that instinct.

The other key idea is the pain of paying. Spending money triggers a tiny psychological sting, and the bigger that sting, the more we hesitate. The trouble is that cards, autopay, and one-tap checkout numb it almost completely.

So the goal isn’t to squeeze out more willpower. It’s to build a system that brings back the sting and adds friction. All seven strategies below come from that single idea.

2. Strategy 1 — Cool the Impulse With a 24-Hour / 30-Day Wait Rule

Simple, and surprisingly powerful: wait 24 hours for small buys and 30 days for big ones, then check if you still want it. Once the emotional “hot state” cools, that must-have item often goes strangely flat.

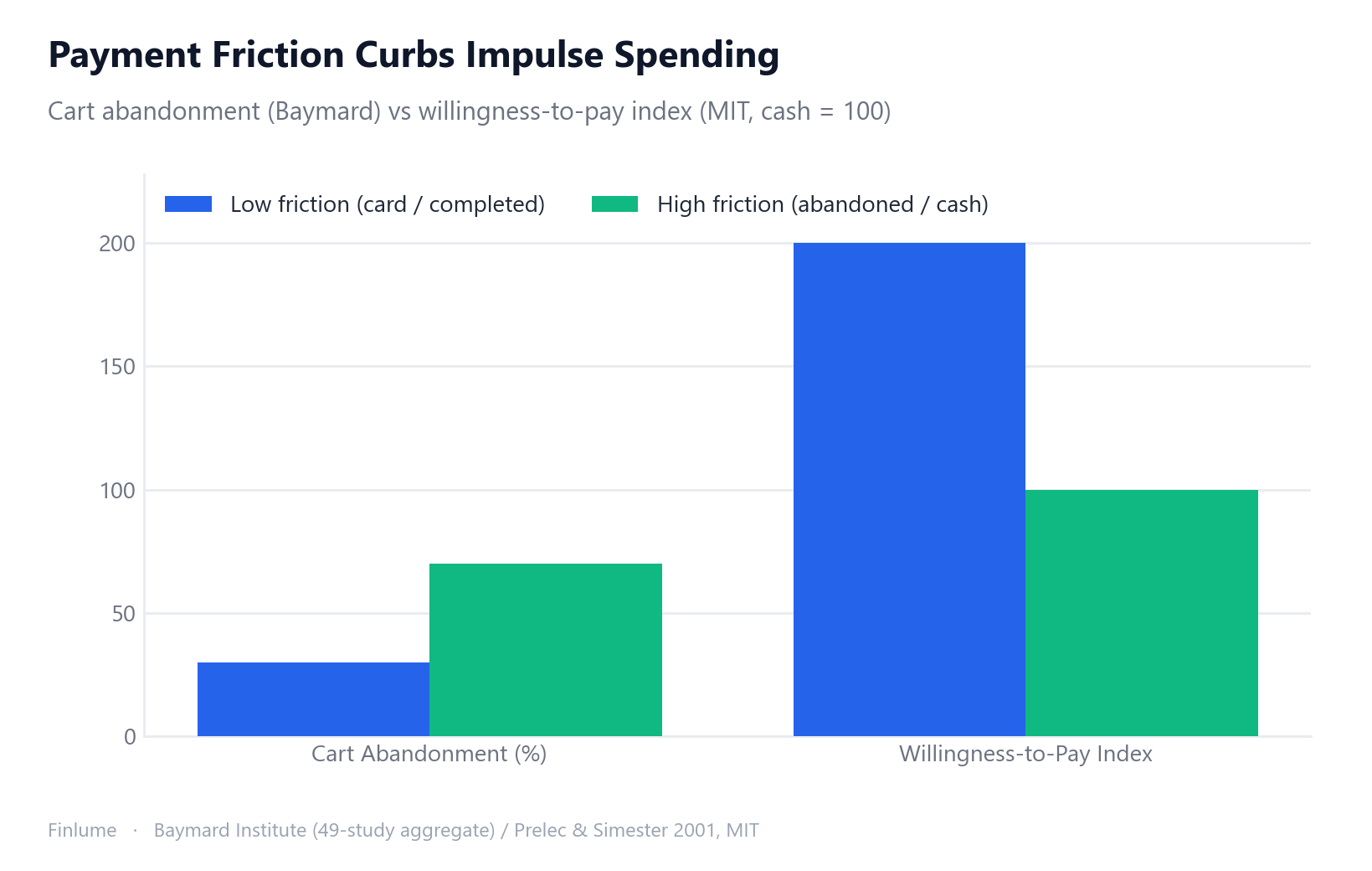

Here’s a telling clue. Baymard Institute, pooling 49 studies, found the average online cart abandonment rate is about 70%. That number is driven by a mix of things — shipping costs, account sign-ups, and so on — but one thing is clear: when people pause right before paying, a large share simply don’t buy.

In other words, a “wait” is just a way to engineer that natural pause on purpose. Load up the cart, sleep on it, and see how you feel tomorrow.

3. Strategies 2 & 3 — Add Friction to Paying

Strategy 2: Use cash or a debit card. A classic 2001 auction study by Prelec & Simester (MIT, Marketing Letters) found that for the same item, the maximum people would pay was significantly higher with a credit card than with cash — up to roughly double for things like sports tickets. Cards anesthetize the pain of paying.

(You’ll often see claims like “cards make you spend 64% more.” Honestly, the multiplier varies a lot by category, so I wouldn’t pin it to an exact figure. Just remember the direction: cash < card.)

Strategy 3: Delete saved cards and one-click checkout. Remove the stored card number and turn off one-tap, so you have to punch in 16 digits every time. That tiny bit of friction buys you the one decisive minute it takes for a hot state to cool.

4. Strategy 4 — Make the Opportunity Cost Visible

The 2009 study “Opportunity Cost Neglect” by Frederick and colleagues makes a sharp point: when we buy something, we don’t automatically think about what else that money could buy. But when the opportunity cost is spelled out, purchase intent drops noticeably.

So I’m a fan of converting a price into something concrete. “This $50 = three dinners out.” “This $300 = a month of groceries.” The moment an abstract number turns into a specific thing you’re giving up, your hand hesitates.

5. Strategy 5 — Remove the Temptation From Your Environment

One of the most reliable findings in behavioral design: removing temptation from your environment beats relying on willpower. On a tired, stressed evening, one marketing email turning into a purchase isn’t weakness — it’s predictable.

- Unsubscribe from store marketing emails

- Turn off push notifications on shopping apps — delete the app if you can

- Clean out bookmarks and wishlists

When temptation isn’t in front of you, there’s no fight to lose.

6. Strategies 6 & 7 — Pre-Set a Budget/List and Check Your Mood

Strategy 6: Decide your list and budget before you shop. Thaler’s mental accounting and the principle of precommitment both say the same thing: set what you’ll buy and a spending cap in advance, and unplanned spending shrinks. Just walking into a store holding a list makes a difference. The simplest way to set that cap is to split your paycheck with the 50/30/20 rule, and if you want to track every dollar so nothing slips away, zero-based budgeting is a natural fit.

Strategy 7: Check your emotional state. Self-control crumbles under fatigue, stress, and hunger. My personal rule is simple: “No buying when hungry, angry, or after midnight.” Almost everything I’ve bought in those three states came back as regret.

7. The Real Price Tag — What Your Impulse Habit Costs Over Time

Strategy 4 (opportunity cost) is powerful in the abstract, but here is what it looks like in numbers. The table below asks a simple question: if you redirected your monthly impulse spending into an investment returning 7% per year, how much would it grow?

All figures are in multiples of your monthly amount — multiply by your own currency to get a concrete number.

| Monthly impulse redirected | 5 years | 10 years | 20 years | 30 years |

|---|---|---|---|---|

| 50 × monthly unit | 3,580 | 8,654 | 26,046 | 60,999 |

| 100 × monthly unit | 7,159 | 17,308 | 52,093 | 121,997 |

| 200 × monthly unit | 14,319 | 34,617 | 104,185 | 243,994 |

Assumption: 7% annual return, compounded monthly (FV of annuity). For illustration only — actual returns vary.

The numbers get striking at the 20–30 year mark. Redirecting 100 units per month for 20 years turns a total contribution of 24,000 units into 52,093 units — a 117% gain purely from compounding (investment growth = 28,093 units on top of what you put in). At 30 years, the same habit produces nearly 3.4× what you actually deposited.

The point isn’t to make you anxious about every coffee. It’s to make the trade-off concrete: each line item on your impulse list isn’t just today’s price — it’s a multiplier that the market would have run for you.

8. The Takeaway — Systems Over Willpower

Impulse buying isn’t always bad. A small, planned treat inside your budget is the oil that keeps life running. It only becomes a problem when it slips out of control. So skip the self-blame and change the system instead.

| Strategy | Core principle | One-line action |

|---|---|---|

| 1. Wait rule | Cool the hot state | 24h for small, 30d for big |

| 2. Cash/debit | Revive the pain of paying | Cash over card |

| 3. Payment friction | Add steps | Delete saved cards & one-click |

| 4. Opportunity cost | Make the trade-off real | ”This money = what else?“ |

| 5. Block temptation | Remove the cue | Unsubscribe, kill notifications |

| 6. Budget & list | Precommit | Set items and a cap upfront |

| 7. Mood check | Protect self-control | No buying when tired, hungry, or up late |

| Key insight | Every impulse $ has a future cost | 100 units/month for 20 yr = 52,093 units @ 7% |

You don’t need all seven. Pick one and start today. The minute you fix the system instead of blaming your willpower, your statement starts getting a lot quieter. If you’re not sure where to park the money you stop spending, first settle on the savings rate that fits your situation, then give those dollars a clear destination with SMART financial goals.

Frequently Asked Questions

Q. What’s the single most effective way to stop impulse buying?

If you pick just one, use the wait rule: wait 24 hours for small buys and 30 days for big ones, then check if you still want it. Once the emotional hot state cools, many items lose their appeal. Simply pausing right before you pay is often enough to not buy at all.

Q. Do you really spend more when you pay with a credit card?

The direction is clear. In Prelec & Simester’s 2001 MIT auction study, for the same item the maximum people would pay was significantly higher with a credit card than with cash, and in some cases up to roughly double. Cards numb the pain of paying. The exact multiplier varies a lot by category, so it’s hard to pin down a precise figure.

Q. Does making the opportunity cost visible reduce impulse purchases?

Yes. Frederick and colleagues’ 2009 “Opportunity Cost Neglect” study found that we don’t automatically think about what else our money could buy, but when the opportunity cost is spelled out, purchase intent drops noticeably. Converting a price into something concrete, like “this $50 = three dinners out,” helps.

Q. Is impulse buying always a bad thing?

No. A small, planned treat inside your budget is the oil that keeps life running. It only becomes a problem when it slips out of control. Rather than blaming yourself, the key is to build a system that revives the pain of paying and adds friction.

This article is for informational purposes based on behavioral economics research and is not specific financial or investment advice. Spending habits vary by individual circumstances.